(Dec. 17, 2021) The “normal operating level” (NOL) of the NCUSIF – the level at which NCUA considers whether it needs to inject more reserves into the fund to cover looming losses, primarily through premiums – was set at 1.33% by the agency board Thursday. The decision was made after the agency dropped two of eight factors it uses to set the NOL as “no longer necessary” (the modeled potential decline in value of the NCUSIF’s claims on the corporate asset management estates; and to account for a potential projected equity ratio decline through the end of the following year without an economic downturn) … Robert (“Rob”) Schmidt is the new director of the Alaska Division of Banking and Securities; he succeeds James McConnell who left in October … The OCC finalized rescission of its 2020 rule implementing the Community Reinvestment Act (CRA), reverting agency rules to those adopted in 1995 and followed by its fellow federal banking regulators. The 2020 CRA rule was rescinded, the OCC said, to “facilitate the ongoing interagency work to modernize the CRA regulatory framework and promote consistency for all insured depository institutions.”

LINK:

Share Insurance Fund 2022 Normal Operating Level

(Nov. 19, 2021) Shared locations are service facilities for purposes of multiple common bond federal credit unions (FCUs) adding underserved areas to their membership bases, as are those with electronic facilities such as video teller machines, regardless of whether those credit unions have an ownership interest in either of the facilities, under a rule finalized Thursday by the NCUA Board.

However, automated teller machines (ATMs) continue to be excluded from the service facility definition for adding underserved areas, according to the new rule.

The final rule, approved unanimously by the three-member board, will take effect 30 days after publication in the Federal Register.

The rule was proposed nearly a year ago (in December 2020) to modify Part 701, Appendix B, of NCUA’s regulations to include any shared branch, shared ATM, or shared electronic facility in the definition of “service facility” for a multiple-common-bond FCU that participates in a shared branching network. “Reasonable proximity” to those shared facilities by an underserved group is a requirement under federal law for an FCU to add the group to its membership.

The proposal ran into opposition (largely from banking groups, evidenced by 680 form letters out of more than 700 total comment letters received) objecting to the definition of “service facility” to include ATMs. For the final rule, NCUA dropped ATMs from its shared service definition.

It also dropped in the final rule the requirement that FCUs seeking to add underserved groups must have an ownership interest in shared locations and electronic facilities.

The final rule does include, however, continues to mandate that a service facility must offer all three services: ability to take deposits (shares), approve loans and disburse loan proceeds

In other meeting proceedings, the NCUA Board:

- Heard an update on its new exam tools (including the (the Modern Examination and Risk Identification Tool, MERIT), noting that there are now 3,383 total MERIT system users, including 547-plus state supervisory authorities (SSAs).

- Issued a proposed 2022-2026 strategic plan for a 60-day comment period.

- Was told that the National Credit Union Share Insurance Fund (NCUSIF) is expected to reach an equity ratio of 1.28% by year’s end (if the ratio falls below 1.2% — or is projected to do so within six months – the NCUA Board is required to implement a restoration plan – including a premium – to bring the ratio above 1.2% within eight years).

LINKS:

Final Rule, Part 701, Shared Services Facilities

Board Briefing, NCUA’s Modernized Examination Tools

Board Briefing, Share Insurance Fund Quarterly Report.

(Sept. 24, 2021) In other action Thursday, the NCUA Board:

- Approved “midsession budget review” action that will use a $15 million 2021 budget surplus (realized through savings on curtailed travel during the coronavirus pandemic) to add seven new positions to the agency’s employment roster, among other things. Those positions will be added to the agency’s cybersecurity program (three new positions), the NCUA Board secretary (one position), and the agency’s office of ethics counsel (three positions), taking up $11 million of the surplus. The balance will be “reprogrammed,” with $2.4 million going to address cybersecurity support, employee relocations, and “human capital analytical support” (for analysis of compensation plans and diversity/equity/ inclusion programs and practices), and approximately $1.6 million to cover employee leave payouts.

- Considered a staff projection that, by year’s end, a “residual budget balance” (or surplus) of about $24.6 million will be left, which the agency said “can be used to offset future budget needs by the agency.”

- Heard a quarterly report on the National Credit Union Share Insurance Fund (NCUSIF), which noted an equity ratio for the fund, as of June 30, at 1.23% — three basis points above the minimum allowed by law before a “restoration plan” (including assessment of a premium) can be established by the board, but well below the fund’s current “normal operating level” (NOL) of 1.38%. Along those lines, Board Member Hood said he wants the board to consider resetting the NOL to 1.3% at either the October or November board meetings (staff project the equity ratio to rise to 1.28% at the end of December 2021).

Regarding the budget review, NASCUS’ Lucy Ito urged NCUA to apply any surplus in 2021 to offset the overhead transfer rate (OTR) for 2022. “Additionally, surplus in the share insurance fund’s admin budget, which largely represents savings in state examiner training, should either be reserved for future training needs or also used to offset the OTR even more,” Ito said.

LINKS:

Board Briefing, Share Insurance Fund Quarterly Report

Oregon Member Business Lending Rule

(Sept. 17, 2021) A proposed rule on subordinated debt will be on the agenda of the NCUA Board when it meets next week, according to an agenda published Thursday by the agency.

According to the agenda posted on its website, the NCUA Board will consider a rule on the subordinated debt under parts 702 (capital adequacy) and 703 (investment and deposit activities) under its regulations.

Late last year, the agency adopted a subordinated debt final rule on allowing well-capitalized, federally insured credit unions to count the debt instrument as capital for risk-based net worth purposes. Under the final rule ultimately published in January of this year, the rule is slated to take effect Jan. 1, 2022. That date is the same that new risk-based capital rules for credit unions are to take effect.

The rule also grandfathered any secondary capital issued before the rule’s effective date of Jan. 1, and preserves that capital’s regulatory capital treatment for 20 years after the effective date. The “grandfathered secondary capital” generally, the agency said, remains subject to requirements in the agency’s current secondary capital rule.

Also on the agenda for the board’s meeting next week is:

- A quarterly report on the National Credit Union Share Insurance Fund;

- A review of the business loan rule for Oregon credit unions (to determine if the state rule covers all the provisions in the NCUA rule and is no less restrictive, thus exempting credit unions in the state from compliance);

- A 2021 mid-session budget review;

- And an item merely listed as “NCUA Board Agenda.” No other information is given.

The board meeting is scheduled to get underway at 10 a.m. ET, and will be streamed live via the Internet.

LINK:

NCUA Board Agenda for the Sept. 23, 2021 Meeting

(May 21, 2021) The development that, at least for now, a premium won’t be necessary to be paid by federally insured credit unions to the NCUSIF is good news for all credit unions, NASCUS President and CEO Lucy Ito said Thursday. However, she cautioned, vigilance is crucial. “Certainly there is more ahead to play out for the economy – but there is no crystal ball on the outcome for any of us. The credit union system, in any event, will have to watch all indicators carefully to determine which way things are going, and even consider some alternative approaches if necessary. Board Member Rodney Hood asked several insightful questions about the insurance fund’s investment powers and strategies – which may spark a conversation about an alternative approach for staving off premiums in the future. In any event: the state system will be part of any conversations about the fund’s finances, and the impact on the state system.”

(May 21, 2021) Giving his agency examination and enforcement authority over third-party vendors, and making key changes to the structure of the federal savings insurance fund for credit unions, were the top legislative requests made to a House committee by NCUA’s Todd Harper this week.

The NCUA Board chairman told the House Financial Services Committee – which held an oversight hearing of all of the federal credit union and banking regulators — that his agency needs the third-party exam authority because, increasingly, activities that are “fundamental” to credit unions are being outsourced to entities outside of the agency’s regulatory oversight. Those activities include, he said, loan origination, lending services, Bank Secrecy Act/anti-money laundering compliance (BSA/AML), financial management and technological services including information security and mobile and online banking.

Those third parties also include credit union service organizations (CUSOs), he said. And, he added, while there are many advantages to credit unions and members in using the service providers, “the concentration of credit union services within CUSOs and third-party vendors presents safety and soundness and compliance risk for the credit union industry.”

As examples, he pointed to the top five credit union core processor vendors which, he said, provide services to approximately 87% of total credit union system assets, and the top five CUSOs, which provide services to nearly 96% of total credit union system assets. “A failure of even one of these vendors represents a significant potential risk to the Share Insurance Fund and the potential for losses from these organizations are not hypothetical,” he asserted. “Between 2008 and 2015, CUSOs contributed to more than $300 million in losses to the Share Insurance Fund alone,” he added, referring to the National Credit Union Share Insurance Fund (NCUSIF).

Harper noted that now NCUA may only examine CUSOs and third-party vendors with their permission. He asserted that continued transfer of operations to third parties (and CUSOs) “diminishes the ability of NCUA to accurately assess all the risks present in the credit union system and determine if current CUSO or third-party vendor risk-mitigation strategies are adequate.“

NASCUS supports the agency obtaining the power over technology service providers (TSPs) that provide services to federally insured credit unions — provided that any such authority requires NCUA to rely on state examinations of such service providers where such authority exists at the state level. Further, NASCUS supports efforts to strengthen state regulatory exam and supervision of third parties providing services to state-chartered credit unions.

Regarding the insurance fund, Harper made three legislative requests to the committee:

- Increase the fund’s capacity by removing the 1.50% statutory ceiling on its capitalization;

- Remove the limitation on assessing premiums when the equity ratio exceeds 1.30% of equity in the fund to insured shares, giving the NCUA Board discretion on the assessment of premiums;

- Institute a risk-based premium system.

“These recommended changes, if enacted, would allow the NCUA Board to build, over time, enough retained earnings capacity in the Share Insurance Fund to effectively manage a significant insurance loss without impairing credit unions’ contributed capital deposits in the Share Insurance Fund,” he said. “Moreover, these changes would generally bring the NCUA’s statutory authority over the Share Insurance Fund more in line with the statutory authority over the operations of the (FDIC’s) Deposit Insurance Fund.”

LINK:

(May 21, 2021) In a related move Thursday, the NCUA Board voted unanimously to seek public comments on its policy that guides the determination of the insurance fund’s Normal Operating Level (NOL).

Now, the NOL (the target equity ratio set for the insurance fund by the NCUA Board) is set at 1.38%. Under the law, the board may set the NOL at anywhere between 1.2% to 1.5%. If the equity level is greater than the NOL, the NCUA Board may vote to make a distribution back to credit unions of the equity in the fund above the NOL (as it did two years ago).

According to NCUA staff, a re-evaluation of the NOL policy is prompted by two events: the current economic landscape (along with the impact of current forbearance programs ending, and likely evictions rising – both perhaps leading to loan underperformance), and pending events related to the corporate asset management estates and end of the NCUA Guaranteed Notes (NGN) Program. Staff noted that the NOL will no longer have to take into consideration the NGNs after June, since the last of the notes will have been, by then, liquidated.

The agency said it is looking for looking for comments on a variety of subjects regarding the NOL policy, including:

- Should a moderate or severe recession be the basis for evaluating the insurance fund’s performance?

- Should a five- year period — or a longer or shorter period – be used for modeling the fund’s performance?

- How should the agency use the modeled potential decline in value of the fund’s claims on the corporate asset management estates going forward until the estates are fully resolved?

- Should the projected equity ratio decline continue to be incorporated into the NOL analysis through the end of the following year without an economic downturn (or should this period be longer or shorter, or not factored into the analysis at all)?

A 60-day comment period was set for public input.

LINK:

Request for Comment, Share Insurance Fund Normal Operating Level Policy

(May 21, 2021) There is likely no insurance premium in the immediate future for federally insured credit unions, as the estimated equity level for the federal credit union insurance fund will be slightly above the level that would trigger the process for assessing a premium, the NCUA Board was told Thursday.

During its regular monthly meeting for May, the board heard a staff report on the National Credit Union Share Insurance Fund (NCUSIF), which showed that the fund’s equity level at the end of June would stand at 1.22%. According to the Federal Credit Union Act, the board must establish a restoration plan (which would likely include a premium) for the insurance fund if the board determines the equity level will fall below 1.2% within the next six months. So far, the board has not yet made that determination.

The law only requires a premium if the equity level drops below 1.2%. Since the fund hasn’t dropped that low (at least, not yet), no premium is likely. (The board may charge a premium, under the law, if the equity ratio falls below 1.3%, but that is not a requirement.)

The likelihood of a premium could, however, change going forward. NCUA Board Chairman Todd Harper suggested that the full extent of the financial impact of the coronavirus crisis is not yet known. As forbearance programs instituted in the face of the crisis expire, Harper said, “some credit unions will likely see their performance begin to deteriorate. It is also possible that there may be no failures and losses to the fund. We just do not know.”

He added that the agency “must make sure that the share insurance fund is strong enough to weather any stresses, including failures or losses, we know may be coming.”

Vice Chairman Kyle Hauptman took a more sanguine view. “We are aware that in the next year or so, the equity ratio may well right itself without NCUA doing anything more,” Hauptman said. “I want to make that clear: we know that could happen.” But Hauptman also made it clear that no one can predict the future.

LINK:

Board Briefing, Share Insurance Fund Quarterly Report

(May 14, 2021) Whether share insurance applies to a credit union share certificate purchased by a limited liability corporation (LLC) depends in part on who owns the funds and whether the LLC is engaged in an “independent activity” other than one solely related to increasing share insurance coverage, NCUA wrote in an April 23 legal opinion letter, but only made public this week.

The letter, addressing “Proposed Capital Markets Funding Program for Credit Unions” and signed by NCUA General Counsel Frank Kressman, summarizes a scenario in which several LLCs purchase share certificates worth a maximum of $250,000, the “standard maximum share insurance amount” (SMSIA) permitted by NCUA’s share insurance regulations, at federally insured credit unions (FICUs) where they are members or are eligible to be members. The letter states that each LLC would be the actual owner of the share certificates they purchase and would not be holding them in any sort of agent, nominee, or custodian capacity.

The NCUA general counsel wrote that share insurance coverage is provided “only to the actual owner of the funds in an account and requires the true owner of the funds to either be a member of the FICU or otherwise eligible to maintain an insured account at the FICU.”

Additionally, he wrote that the accounts held by a corporation, partnership, or unincorporated association “engaged in any activity other than one directed solely at increasing insurance coverage (that is, an ‘independent activity’) will be insured up to the SMSIA in the aggregate.”

Emphasizing the requirement for ownership of funds, the letter adds that share insurance coverage “is always dependent upon compliance with all applicable requirements of Part 745, including the recordkeeping requirements in § 745.2(c)” of the agency’s rules.

The opinion was sent to Stuart Morrissy of Hogan Lovells US LLP in Washington, D.C.

LINK:

NCUA legal opinion – Proposed Capital Markets Funding Program for Credit Unions

(May 14, 2021) A final rule on investments in derivatives by credit unions, and two items that could have a significant impact on a savings insurance premium for credit unions, are all on the agenda for the NCUA Board when it meets on Thursday.

The final rule on derivatives follows up on a proposal from the agency issued in October, which was designed to make current regulations less prescriptive and more principles-based. The proposal would also expand federal credit unions’ (FCUs) authority to purchase and use derivatives as part of their interest-rate risk (IRR) management.

NASCUS, in its comment letter on the proposal filed with the agency in late December, said the state system supports the proposal, but made two recommendations to make the rule more flexible for the needs of state credit unions. First, NASCUS said the agency should eliminate redundant supervisory notice requirements where applicable. NCUA, the association wrote, should provide an exemption from its notice requirement for FISCUs in states where pre-approval or pre-notification is required to be given to the state regulator.

Second, NASCUS wrote that the agency should incorporate exempt derivatives transactions directly into part 741.219 of its rules – the section that covers FISCUs and investment requirements. Specifically, NASCUS “strongly recommended” that — to facilitate FISCU compliance – the agency should incorporate the excluded transactions under the proposal (under part 703.14 of NCUA rules, which only apply to FCUs) directly into a new subpart (d) of section 741.219. Restating the excluded transactions directly in the relevant FISCU rule, NASCUS wrote, “is a better organizational framework that more clearly communicates to FISCUs the required compliance obligations.”

NASCUS also acknowledged in its letter that a key part of the proposal is continued recognition by NCUA of the primacy of state law in determining investment authority for FISCUs.

Regarding the insurance fund and the future of a premium, the NCUA Board will also consider at next week’s meeting:

- Issuing a comment request on the National Credit Union Share Insurance Fund’s (NCUSIF) “normal operating level” (NOL), which is the reserve level at which the board has determined the fund can adequately cover any losses presented to the fund. The NOL plays a key role in determining whether a premium will be charged to credit unions to bolster the fund’s reserves. The subject of a premium has been the focus recently of considerable discussion. However, NCUA Board Chairman Todd Harper has repeatedly said the question is increasingly not if, but when, a premium will be charged. Separately (but related): In September, the FDIC Board adopted a restoration plan for the agency’s Deposit Insurance Fund (DIF) which — much like the NCUSIF — had been diluted by the massive influx of savings as a result of the financial impact of the coronavirus crisis. The FDIC plan would restore the fund’s reserve ratio to at least 1.35% of reserves to total insured funds within eight years, as required under federal law — but would require no “extraordinary measures” – such as increasing assessment rates. Instead, the agency said last fall that it would, over the next eight years: monitor deposit balance trends, potential losses, and other factors that affect the reserve ratio; maintain the current schedule of assessment rates for insured banks and other institutions; and provide updates to its loss and income projections at least semiannually.

- A quarterly report on the NCUSIF, which should include details on the latest equity level of the fund, which also has an impact on a future premium. Lately, the equity level (the amount of total reserves in the fund relative to total savings insured) has been dropping as insured savings have been growing, spurred by member deposits of federal stimulus payments and other savings. Federal law requires that if the NCUSIF equity ratio drops below 1.2%, the board must adopt a “restoration plan” to bring the equity ratio back up to the fund NOL – including a premium. The insurance fund closed 2020 with an equity level of 1.26%, well below the current NOL of 1.38% (but an improvement from earlier in the year when the equity level stood at just 1.22%).

The board meeting gets underway at 10 a.m. ET; audio of the meeting will be live-streamed via the Internet.

LINK:

NCUA Board meeting agenda, May 20

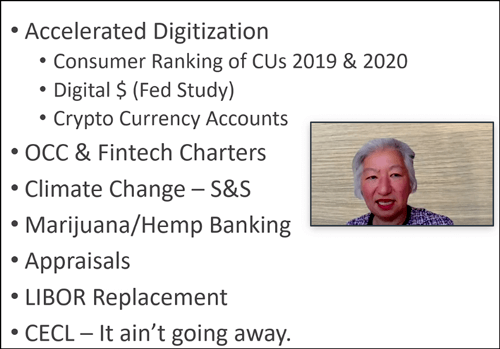

(April 30, 2021) Issues and policies being pursued by the state system were outlined this week by NASCUS President and CEO Lucy Ito during a presentation hosted by CU*Answers’ “The CUSO Challenge.”

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

Ito also laid out NASCUS’ approach for “renovating” the Federal Credit Union Act, to bring the underlying federal line more in line with contemporary times, and to give the state system (which now represents more than half of the total assets of the entire credit union system) fair representation.

Among other things, Ito recommended separating the insurance function from the supervisory role of NCUA, a long-standing position of the association. NASCUS’ position is that the current structure of the National Credit Union Share Insurance Fund (NCUSIF) presents a potential conflict of interest within the agency unless those functions are internally separated. (NASCUS has also noted that any changes to the statutory structure of the NCUSIF should be evaluated and developed in conjunction with state regulators and credit union stakeholders, since state regulators have experience and expertise with statutory and operational construct of the bank deposit insurance fund that would help inform possible changes to the insurance fund.)

She also noted NASCUS’ support for expanding the NCUA Board from three to five members. In any event, NASCUS also supports reserving one seat on the board for a person with experience as a state credit union regulator.

Other renovations to the FCU Act mentioned by Ito included: updating field of membership, regulatory capital, member business lending and investments authorities, and considering changes to board compensation, annual meeting and member expulsion requirements.

(March 19, 2021) Nine areas that will affect the resource needs of NCUA– including monitoring the equity ratio of the savings insurance fund, enhancing the examination program and building the supervision workforce — in the coming year and likely beyond, are listed in the agency’s 2020 annual report released this week.

The nine areas, the agency said, “will continue to shape the environment facing credit unions and will determine the resource needs of the NCUA.” Those areas are:

- Monitoring the National Credit Union Share Insurance Fund’s (NCUSIF’s) equity ratio

- Enhancing the agency’s examination program

- Building the NCUA workforce to supervise an evolving credit union environment

- Declining membership in small credit unions

- Growing threats to cybersecurity

- Adapting to technology-driven changes to the financial landscape

- Factoring the near-term economic outlook

- Managing interest rate risk and liquidity risk

- Continuing consolidation

Regarding the insurance fund, the agency said that an incident such as a significant credit union failure that drops the equity ratio below 1.0% “would result in a direct expense to credit unions through the impairment of the 1.0% capital deposit they contribute to the fund, which credit unions have recorded as an asset on their balance sheets.”

“Additionally, if the equity ratio falls below 1.20%, or is expected to within six months, the Federal Credit Union Act requires the NCUA Board to assess a premium on federally insured credit unions to restore the fund to at least 1.20% or adopt a fund restoration plan,” the report reminds. It notes that the fund, as of Dec. 31, 2020, was at 1.26% of equity to shares insured — 12 points below the “normal operating level” of the fund of 1.38%.

As for enhancing the exam program, the report states that in 2021 the agency will finalize deployment of the new MERIT system and transition new exams from AIRES to the new method. “This transition includes the agency’s primary examination platform as well as many business processes targeted to take advantage of MERIT’s configurable platform,” the report states. It also indicates that the agency will continue to develop its Enterprise Data Program, intended to “enhance how agency governs and reports its data.”

On building its workforce, the agency said it increasingly needs cybersecurity specialists and experts in areas including capital markets, commercial lending, consumer financial protection and payments systems. “The agency also has a large percentage of employees who have reached, or will soon reach, retirement age, including many in senior levels of management,” the report states. “Finding appropriate successors who can lead the agency and employees who have the requisite skills and expertise is essential to ensuring that the NCUA can continue to achieve its mission effectively.”

The report notes that, this year, it will use a new learning management system to “better enable access to on-demand training for all employees,” and will develop and execute training to support implementation of the new MERIT exam system and its multi-year leadership development strategy.

Also in the report, the agency states:

- Among its supervisory priorities in the wake the coronavirus crisis, it will work with state regulators and credit unions to identify operational challenges emerging from the impact of the pandemic;

- It will continue in 2021 working with six state regulators in piloting an alternating-year examination program for federally insured, state-chartered credit unions (FISCUs). After the pilot ends, the agency said, it and the states will assess how – and whether – the results can improve the exam program, particularly by improving coordination.