Courtesy of Matt Egan, CNN

As leaders in Washington fail to make progress on a debt ceiling deal, Moody’s Analytics is warning of disastrous implications for American jobs if the United States defaults on its debt for an extended period.

Treasury Secretary Janet Yellen has forecast that the United States could run out of cash and extraordinary measures to pay its bills as soon as early June if Congress does not act.

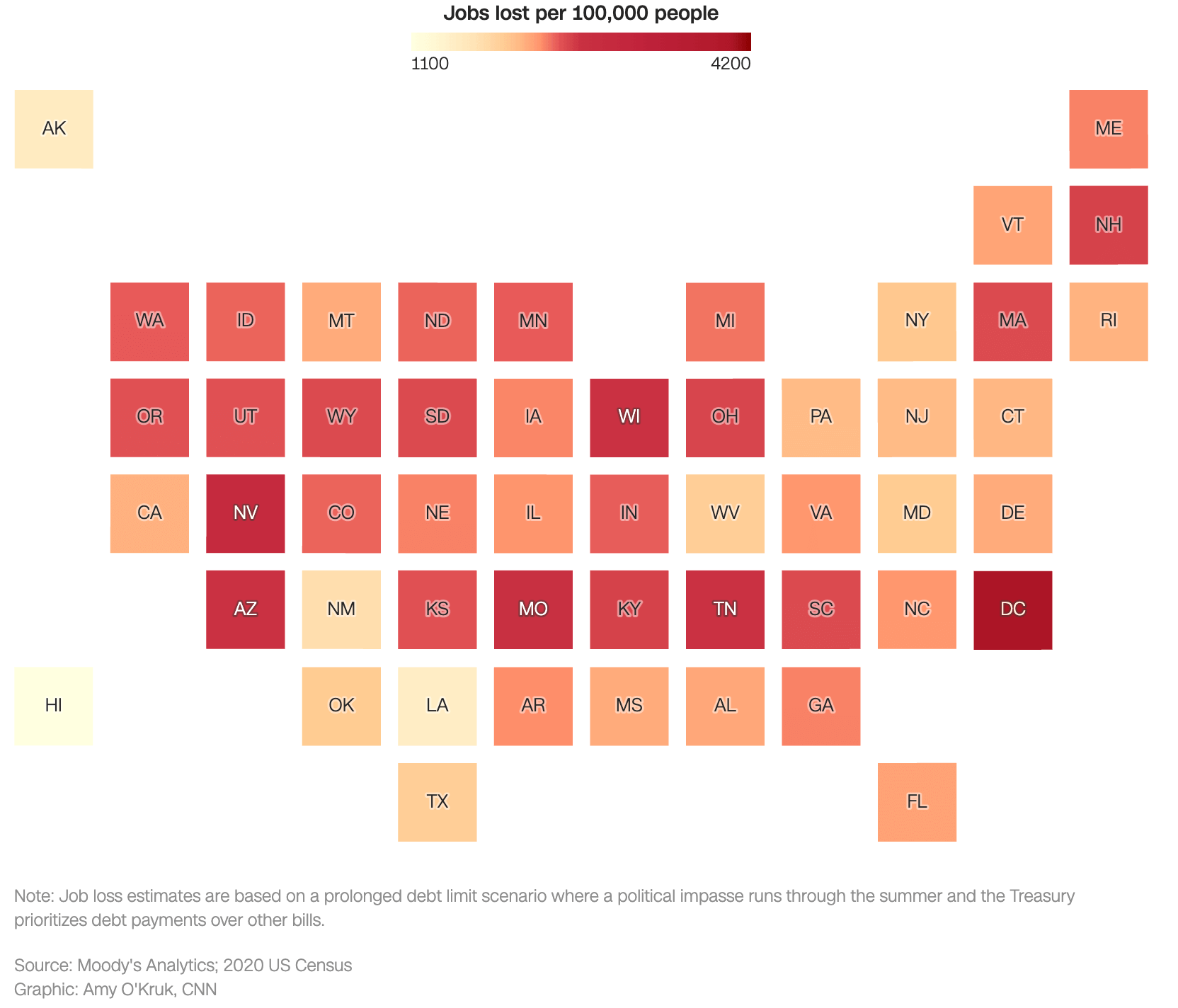

While most states would be “hit hard” by a debt limit breach, the economic pain would vary from state to state, according to projections released on Wednesday by Moody’s. It would disproportionately hurt states with large concentrations of federal workers or that have a number of jobs that rely on government funding. That includes Washington, DC, and states located near or that rely on federal institutions such as national labs or military bases such as Alaska, Hawaii and New Mexico.

A prolonged debt limit breach could cut thousands of jobs across the US

A prolonged debt limit breach could cut thousands of jobs across the US

Most state economies and DC will be hit hard if there’s a prolonged debt limit breach, particularly D.C. with its large government presence. Business- and tourist-travel-heavy states, such as Arizona and Nevada, will also be disproportionately impacted, according to Moody’s Analytics.

Soaring unemployment

The analysis spells out other widespread damage: The unemployment rate would spike to near-double digits in the District of Columbia (8.9%), California (8.7%) and Ohio (9.5%). Michigan’s unemployment rate would reach 10.8%, up from 4.1% today.

Other states that would feel significant impact are ones that rely on federal spending and aerospace, such as Virginia, Connecticut, Kansas and Washington. Moody’s said tourism-dependent states including Arizona, Florida and Nevada will eventually experience “sharp” job loss as well those that rely on auto manufacturing, like Michigan and South Carolina.

In the event of a prolonged breach of the debt ceiling, Moody’s estimates some large states would each lose hundreds of thousands of jobs. California could lose 841,600. Texas may lose 561,700. The report predicts Florida would lose 474,700 jobs, New York could shed 398,300, and Ohio, Pennsylvania and Georgia would each lose more than 200,000.

‘A real threat’

In its report, Moody’s assigns a 10% probability to a breach of the debt ceiling, up from 5% previously.

“What once seemed unimaginable now seems a real threat,” Moody’s Analytics chief economist Mark Zandi wrote in the report.

A breach is not the same thing as a default.

In an email to CNN, Zandi explained that a breach would occur if the Treasury Department fails to make a payment to any creditor on time – whether that be a Social Security recipient or the electric bill for a government building in Omaha.

A default would only occur if Treasury fails to make a debt payment on time, Zandi said.

In the report, Zandi wrote that if there is a breach, it would be “much more likely to be a short one than a prolonged one,” though even a “lengthy standoff no longer has a zero probability.”

The new warning from Moody’s comes a day after a meeting on Tuesday between President Joe Biden and Congressional leaders ended without any progress on a debt ceiling deal.

Zandi noted that although there are some emerging signs of concern in financial markets, for the most part investors “appear largely unruffled” by the estimated June 1 deadline.

“The longer it takes for financial markets to react,” Zandi wrote, “the greater the odds that lawmakers will not act in time, since market turmoil is probably what it will take to generate the political will lawmakers will need to come to terms.”