(Dec. 10, 2021) Every dollar transferred from the federal credit union savings insurance fund to fund NCUA expenses is one dollar not available to cover losses in the system and subsequently a dollar that may need to be replenished in the NCUSIF by the charging of a premium, NASCUS President and CEO Lucy Ito told the agency this week.

And that’s why it is so important for both state and federally chartered credit unions to understand and closely monitor how the agency moves money from the insurance fund and into its operating budget via the overhead transfer rate (OTR), Ito said.

Acknowledging that any discussion of the OTR is lackluster (she said, at worst, such dialog can leave stakeholders “bleary-eyed” or lull credit unions into a “deep, deep coma”), credit unions need to know and comprehend: every National Credit Union Share Insurance Fund (NCUSIF) dollar that NCUA uses to cover its expenses is one dollar less in the NCUSIF’s equity level. “This is the fundamental reason why both state and federal credit unions should take serious interest in the OTR,” she asserted.

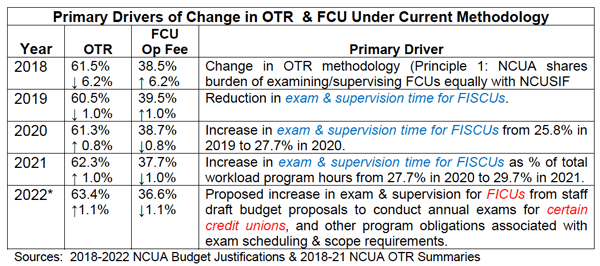

Ito made the comments this week during a public briefing and comment opportunity about the NCUA 2022 budget. The agency has proposed a 63.4% OTR for 2022, meaning that nearly two-thirds of the 2022 operating budget will be paid out of the share insurance fund (the remainder comes from federal credit union (FCU) operating fees). The operating spending plan – at $326 million — makes up 94.4% of the overall NCUA budget.

The 2022 OTR will be 110 basis points higher than the previous year’s and will be the third straight year that an increased transfer has been proposed by the agency (at 61.3% in 2020, 62.3% in 2021, and the proposed 63.4% for 2022).

Aside from taking funds from the insurance fund that could cover credit union losses, Ito said, there are two other reasons credit unions should monitor the OTR. First, NCUA’s use of NCUSIF dollars versus use of FCU operating fees to cover its expenses has the potential to imbalance the dual chartering system by disadvantaging the state system. “This is a threat to both state and federal credit unions,” she said, “because the dual charter framework is the credit union system’s most dynamic source of innovation and charter modernization.”

The third reason, she said, is the equity level of the insurance fund and the NCUA Board’s thought of raising the normal operating level (NOL) of the fund in anticipation of economic uncertainties related to the ongoing COVID-19 event. “Given the NCUA Board’s deliberations on changing the NOL to bolster NCUSIF equity, it behooves credit unions to monitor more than OTR as a mere formula used to transfer funds from the NCUSIF,” she said. “Credit unions should also be interested in what additional costs NCUA is now covering with NCUSIF dollars.”

Ito said her comments were made in the “pure spirit of state-federal regulator collaboration and in support of our shared objectives to foster a safe and sound and vibrant dual charter system that protects member-consumer best interests.”

In a nod to her impending retirement at year’s end, she thanked the board members for their “collegiality and commitment to forging a robust federal credit union system and a robust state credit union system” with state regulatory agencies during her seven-year run as NASCUS leader.

LINK:

President and CEO Lucy Ito Testifies on OTR During the 2022 NCUA Budget Briefing

(Dec. 10, 2021) Minimizing the risk of disruptive litigation and adverse economic impacts associated with the transition away from the LIBOR reference rate is the aim of legislation passed by the House Wednesday.

The Adjustable Interest Rate (LIBOR) Act of 2021 (H.R. 4616), passed on voice vote, was sponsored by Rep. Brad Sherman (D-Calif.). In addition to minimizing litigation and economic risks, supporters say the bill will encourage a fair transition for financial contracts that do not consider the permanent cessation of LIBOR by June 2023 in existing contracts, and have no workable fallbacks. LIBOR as a reference rate may no longer be used for new loans or other financial contracts after Dec. 31.

The bill states its intent is to establish a clear and uniform basis nationwide for replacing LIBOR in existing contracts whose terms do not provide for the use of a clearly defined or practicable replacement benchmark rate, without affecting the ability of parties to use any appropriate benchmark rate in new contracts.

The legislation, similar to a statute enacted earlier this year in New York, now heads to the Senate for consideration.

LINK:

H.R. 4616, The Adjustable Interest Rate (LIBOR) Act of 2021

(Dec. 10, 2021) Creditors must select by April 1 replacement indices for existing LIBOR-linked consumer loans, which include closed- and open-end credit provisions that require a link to an index comparable to the soon-to-be-defunct rate, according to a final rule issued this week by the CFPB.

LIBOR (the London Interbank Offered Rate) is scheduled to be discontinued after Dec. 31; no new contracts or loans may be agreed to using LIBOR after that date. After June 2023, LIBOR may no longer be used for any existing financial contracts.

CFPB said its final rule includes closed-end credit provisions that require creditors to choose an index comparable to LIBOR when changing the index of a variable rate loan, or consider it a refinancing for purposes of its Regulation Z (which implements the Truth in Lending Act (TILA)).

The bureau said that, to help creditors determine a comparable index for closed-end loans, the rule identifies certain spread-adjusted indices based on the Secured Overnight Financing Rate (SOFR), a LIBOR alternative developed by the Federal Reserve-sponsored Alternative Reference Rates Committee (ARRC). The indices are intended for consumer products as examples to illustrate a reference rate that would be comparable to replace 1-month, 3-month, or 6-month tenors of USD LIBOR, according to CFPB.

Another closed-end credit provision of the final rule, the bureau said, includes a “non-exhaustive” list of factors for creditors to help determine whether a replacement index meets the Regulation Z “comparable” standard regarding a particular LIBOR index. The rule also updates post-consummation disclosure sample forms for certain adjustable-rate mortgage loan products replacing LIBOR references with a SOFR index, CFPB said.

Open-end loans, CFPB said, would be covered by the rule under LIBOR-specific provisions to permit creditors or card issuers for home equity lines of credit (HELOCs) and credit card accounts to replace the LIBOR index and adjust the margin used to set a variable rate on or after April 1, 2022, if certain conditions are met.

The conditions, CFPB said, include that the creditor or card issuer generally must choose a replacement index which has historical fluctuations that are substantially similar to those of the LIBOR index and ensure that the new interest rate or APR is substantially similar.

Another “non-exhaustive list” of factors to consider is provided to creditors and card issuers when they are determining whether a replacement index meets the Reg Z “historical fluctuations are substantially similar” standard regarding a particular LIBOR index, and identifies certain SOFR-based spread-adjusted indices recommended by the ARRC for consumer products and the prime rate as examples of indices that meet this standard, the bureau said.

“The rule also finalizes change-in-terms notice requirements proposed by the Bureau for disclosing margin reductions for HELOCs and credit card accounts when LIBOR is replaced,” CFPB said. To help consumers understand how creditors will determine rate changes in the variable rates for their loans, the disclosure requirements will be effective April 1, 2022, and have a mandatory compliance date of Oct. 1, 2022.

The rule also amends Regulation Z to address how the requirement to reevaluate rate increases on credit card accounts applies to the transition from using a LIBOR index to a replacement index.

The bureau noted it did not include a SOFR-based spread-adjustment replacement index for one-year USD LIBOR, saying it was “reserve judgment.”

“Once the Bureau knows which SOFR-based spread-adjusted index the ARRC will recommend for replacing the 1-year USD LIBOR index for consumer products, the Bureau will consider whether that index meets the comparability and ‘historical fluctuations are substantially similar’ standards and, if so, whether to codify such determinations in a supplemental final rule,” CFPB stated.

The agency also released an updated set of frequently asked questions (FAQs) to help creditors address other LIBOR transition topics, regulatory questions, and general implementation considerations.

LINKS:

Final rule: Facilitating the LIBOR Transition (Regulation Z).

(Dec. 10, 2021) A proposed rule designed to “protect the U.S. financial system from illicit use” by addressing who must report corporate beneficial ownership information – including what and when – was unveiled this week by FinCEN.

According to the agency, collecting the information and providing access to law enforcement, financial institutions, and other authorized users will “diminish the ability of malign actors to hide, move, and enjoy the proceeds of illicit activities.”

The proposal implements the beneficial ownership information reporting provisions of the Corporate Transparency Act (CTA). FinCEN said it is taking aggressive aim at “those who would exploit anonymous shell corporations, front companies, and other loopholes to launder the proceeds of crimes, such as corruption, drug and arms trafficking, or terrorist financing.”

The CTA was part of the Anti-Money Laundering Act of 2020, FinCEN said. It established beneficial ownership information reporting requirements for certain types of corporations, limited liability companies, and other similar entities created in or registered to do business in the United States. The proposed rule implements these reporting requirements, the agency noted.

Comments are due in 60 days after the proposal’s publication in the Federal Register.

LINK:

(Dec. 10, 2021) A new candidate for a permanent appointment as comptroller of the currency will have to be found by the Biden Administration after the most-recent nominee, Saule T. Omarova, bowed out of consideration.

In a letter, Omarova said she appreciated President Joe Biden’s (D) nomination of her to lead the Office of the Comptroller of the Currency (OCC), but wrote that “at this point in the process, however, it is no longer tenable for me to continue as a Presidential nominee.”

Omarova, a Cornell University law professor and veteran of the Treasury Department under President George W. Bush (R ), had proven to be a controversial nominee to lead the federal bank regulator. Industry opposition was intense (based on some of her past writings that included suggesting the Federal Reserve consider offering some banking services), and her nomination ran into particular trouble during a hearing last month before the Senate Banking Committee, where she faced intense questioning from Republican senators, described as rude and condescending by some.

Biden accepted the withdrawal but took notice of the opposition Omarova faced. “Unfortunately, from the very beginning of her nomination, Saule was subjected to inappropriate personal attacks that were far beyond the pale,” Biden said in a statement.

For the time being (and until a new nominee is found), the OCC will continue to be led by Acting Comptroller Michael Hsu, who this week named a new chief of staff (Lauren Oppenheimer).

LINK:

(Dec. 10, 2021) The 2022 budget, and three final rules — on mortgage servicing rights, subordinated debt and the complex credit union leverage ratio — are among the items the NCUA Board will consider at its meeting next week.

In November, the board released publicly its proposed budget for the new year, which called for a 1.2% increase from the previous year’s. However, the components of the spending plan show significant changes from the previous year. For example, the agency’s capital budget (which funds such things as purchases of new equipment) is down 30.7% from the previous year (for a total of $13.1 million). The administrative budget for the National Credit Union Share Insurance Fund (NCUSIF) is down by 21.7% (to $6.2 million) from the previous year.

But the agency’s operating budget – which is funded mostly by funds from the National Credit Union Share Insurance Fund (NCUSIF) via the overhead transfer rate (OTR) of a proposed 63.4%, and accounts for 94.4% of the agency’s overall budget – is up 3.6%, according to the NCUA proposed budget for a total of $326 million. It includes 46 new full-time equivalent (FTE) staff positions for 2022 (including 32 regional and specialist credit union examiners). Employee pay and benefits makes up 79% of the operating budget.

(As noted in the item on NASCUS’ comments made during the NCUA budget briefing, the association has pointed out this year’s proposed OTR is the third straight year NCUA has raised the transfer rate.)

The mortgage servicing rights proposal, if finalized, would amend the agency’s investment regulation to permit federal credit unions to purchase mortgage servicing rights from other federally insured credit unions, subject to certain conditions. Describing the proposed rule as “half baked” when it was proposed and released for comment a year ago (and voting against it), NCUA Board Chairman Todd Harper said he could find a way to support a final rule if changes were made.

Also on Thursday’s agenda:

- Share Insurance Fund 2022 Normal Operating Level.

- Final Rule Complex Credit Union Leverage Ratio (parts 702 and 703)

- Subordinated Debt Final Rule (parts 702 and 741).

The NCUA Board meeting is scheduled to broadcast live via the Internet, and to get underway at 10 a.m. ET on Thursday.

LINK:

NCUA Board meeting agenda, Dec. 16

(Dec. 10, 2021) State-chartered credit unions maintained their hold on a slight majority of all credit union assets over the third quarter 2021, with about 50.2% of the total, according to numbers released this week by NCUA and compiled by NASCUS.

The latest numbers make the fourth quarter in a row (since the fourth quarter of 2020) that state credit unions have held the most assets. The results are derived from NCUA third-quarter call reports (for federally insured credit unions) and American Share Insurance, Inc., for privately insured CUs (compiled by NASCUS).

Additionally, state and federal credit unions crossed a new threshold in the third quarter: both exceeded $1 trillion in assets for the first time, for a total of $2.04 trillion combined ($1.02 trillion for states, which includes both federally insured and privately insured), and $1.01 trillion for FCUs.

NASCUS President and CEO Lucy Ito said the third quarter results demonstrate the resilience of state credit unions, their members’ trust in their service and viability, and careful and reasonable supervision by state authorities. “The financial impact of the pandemic caused many members to save their money, particularly that provided by the government to maintain economic activity,” Ito said. “They turned to their credit unions as the repository of their funds, because they knew it was a safe, sound, convenient and responsible shelter for them.”

Overall, assets at both state and federal credit unions have grown by about 9% since the end of last year, reflecting the influx of savings by members.

Meanwhile, memberships at credit unions exceeded 130 million for the first time, with 48.1% held by SCUs and 51.9% by FCUs.

The number of credit unions fell again by the end of the third quarter (continuing a long-term trend driven by consolidation of the industry), with 5,096 total (38.7% SCUs and 61.3% FCUs).

Financially, credit unions posted a solid performance in the third quarter, according to the NCUA numbers for federally insured credit unions (both SCUs and FCUs). That is:

- An aggregate net worth ratio (net worth as a percentage of total assets) of 10.23% at the end of the third quarter, up from 10.16% at the end of the previous quarter. Compared to a year earlier (third-quarter 2020) when the ratio was 10.44%, the ratio had declined. However, it bottomed out in the first quarter of the year at 10.02% and has been climbing, quarter by quarter, since then.

- Return on average assets – a broad indicator of credit union profitability overall– was 112 basis points in the third quarter, NCUA said, the same as posted in the second quarter, but up from 65 basis points in the same period a year earlier. The median credit union return on assets in third-quarter 2021, NCUA noted, was 56 bp, up from 42 bp a year earlier

- Net interest margin was $50 billion, or 2.59% of average assets – up from $48.1 billion, but down as a percentage of average assets, which was 2.87%.

LINK:

Credit Unions See Continued Share and Deposit Growth in Third Quarter

(Dec. 10, 2021) The latest version of the National Defense Authorization Act (NDAA) – must-pass, annual legislation that includes funding for the military, among other things — does not include the SAFE Banking Act, which would allow credit unions to serve legal cannabis-related businesses in states that have legalized cannabis. The House has previously passed an NDAA version that included the SAFE bill; however, that provision ran into trouble gaining support by Senate leaders. NASCUS has strongly supported adoption of the bill … NASCUS sent to credit union and associate members their 2022 membership dues invoices this week. NASCUS primary points of contacts should look for an email from Shellee Mitchell, Program Specialist. If you do not receive your invoice by next week, please let Shellee know at [email protected] NASCUS appreciates the ongoing support from our membership, and we look forward working with you in 2022.

(Dec. 10, 2021) Real estate buyers using cash to purchase residential or commercial properties would be subject to new reporting requirements aimed at spoiling money laundering schemes under a new proposal being explored by the Treasury’s financial crimes unit announced this week.

According to the Financial Crimes Enforcement Network (FinCEN), its advance notice of proposed rulemaking (ANPR) seeks responses on what approach it should take toward residential and commercial real estate transactions to address the “vulnerability of the U.S. real estate market to money laundering and other illicit activity.”

“Given the relative stability of the real estate sector as store of value, the opacity of the real estate market, and gaps in industry regulation, the U.S. real estate market continues to be used as a vehicle for money laundering and can involve businesses and professions that facilitate (even if unwittingly) acquisitions of real estate in the money laundering process,” FinCEN said in a release.

The agency asserted that real estate transactions involving loans or other financing by banks, credit unions and other regulated financial institutions, which are subject to federal anti-money laundering rules, are less susceptible to money laundering because those institutions are required to report suspicious activity to the agency.

By contrast, the agency stated, when real estate is purchased without such financing, it can be “nearly impossible to trace the beneficial owners behind shell companies that are often used to purchase the real estate. As a result, corrupt officials and criminals engaging in illicit activity can exploit the U.S. real estate sector to launder their ill-gotten wealth.”

According to the agency, the ANPR would assist FinCEN in preparing a proposed rule that would enhance the transparency of the domestic real estate market on a nationwide basis and protect the U.S. real estate market from exploitation by criminals and corrupt officials.

FinCEN noted that it has not imposed general recordkeeping and reporting requirements authorized under the Bank Secrecy Act (BSA) on persons involved in all-cash real estate transactions. However, it added that it has imposed specific transaction reporting requirements on title insurance companies in the form of Geographic Targeting Orders (GTOs). The ANPR, the agency said, seeks comment on the approach FinCEN should take with respect to both the residential and commercial real estate sectors.

Comments are being sought on the proposal for 60 days after publication in the Federal Register.

LINK: