Mark your calendar for the latest episode of the NASCUS 101 series, coming up Oct. 14 (at 2 p.m. ET). This popular session covers, in just 30 minutes, NASCUS legislative and regulatory (L&R) resources, educational offerings and webinars, member engagement, as well as news and data.

Additionally, the program shows members how to volunteer for a committee or working group, personalize member communications and sign up for regulatory and security alerts – as well as how to connect with other members to exchange ideas and collaborate.

Also highlighted during the session: NASCUS’ latest product, Campus 365 (powered by BAI), which helps members hone their compliance and professional skills training, and more. The bi-monthly series — free and open to all NASCUS members — illustrates how collaboration among all 45 regulatory agency members, committees, credit unions, leagues, corporates, trade associations, and CUSOs can support the credit union system. NASCUS 101 is also scheduled for Dec. 9. There is no cost, but registration is required (see the link below).

LINK:

NASCUS 101, Oct 14; registration, more info

(Sept. 10, 2021) More than 100 low-income credit unions (LICUs) were awarded grants totaling $1.5 million to expand their outreach to underserved communities and improve digital services and security, the federal credit union regulator said last week.

The grants awarded to the 105 credit unions, NCUA said, were offered through the agency’s Community Development Revolving Loan Fund (CDRLF).

According to NCUA, the grants ranged from $1,500 to $50,000 to credit unions in 35 states and the District of Columbia. The agency said 16 credit unions were first-time grant recipients, and 33 were minority depository institutions. Awards were made in two categories: Underserved outreach (for 22 grants totaling $1,006,190), and digital services and cyber security (for 83 grants totaling $529,517).

The agency said it received 280 grant applications seeking more than $4.6 million.

LINK:

NCUA Awards Grants to Assist Low-Income Credit Unions

(Sept. 10, 2021) Helping regulators and the public better understand the business lending market is the stated aim of a new rule unveiled Sept. 1 by CFPB, according to its acting director.

The proposed rule would require lenders to disclose information about their lending to small businesses. According to the bureau, lenders would be required to report the amount and type of small business credit applied for and extended, demographic information about small business credit applicants, and key elements of the price of the credit offered.

That information would allow it to learn, the agency said, how small enterprises fare when trying to access financing, and what barriers are holding them back from further prosperity.

CFPB noted the rule was mandated by the legislation which created the bureau, the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank).

In comments to the press Sept. 1, CFPB Acting Director Dave Uejio said the bureau and the public don’t know enough about whether small businesses have fair access to the capital they need to generate new jobs and grow the economy.

“As we saw all too recently in the original design and implementation of the Paycheck Protection Program (PPP, established to help businesses keep paying their workers during the coronavirus crisis), we need to know much more about the credit needs of small businesses if we are to support them adequately in times of crisis and day-to-day,” Uejio said. “Our rule, if finalized, will shed much-needed light on the credit needs of small businesses, and it will help unleash the true potential of our nation’s entrepreneurs.”

Under the proposal – issued with a 90-day comment period, with no extension anticipated, the agency stated – lenders would be required to collect and report data about credit applications from small businesses, including women-owned and minority-owned small businesses. The bureau said the proposed reporting requirements would apply to a wide range of credit products, including term loans, lines of credit, credit cards, and merchant cash advances.

The agency said it would publish “application-level” data collected under the rule, but would modify or withhold data from public disclosure “based on an assessment of the risks to privacy interests and the benefits of publication.”

LINK:

CFPB Proposes Rule to Shine New Light on Small Businesses’ Access to Credit

Remarks of Acting Director Dave Uejio at the Press Call on the Small Business Lending Proposed Rule

(Sept. 10, 2021) Banks have more time to comment on proposed guidance to help them manage third-party risk, with a new deadline of Oct. 18, the federal banking agencies said this week. The agencies said the extension for the comment period – originally set to end Sept. 17 – was adopted to allow more time for individuals to analyze issues and prepare their comments. The proposed joint guidance was issued July 13; it is based on 2013 guidance from the Office of the Comptroller of the Currency (OCC). The latest guidance also covers arrangements between banks and financial technology (fintech) firms. NCUA did not join in proposing the guidance … An information and communications technology (ICT) supply chain risk management fact sheet has been posted on the NASCUS website, to help the state system raise awareness of risks to supply chains and help reinforce an overall national culture of security. The fact sheet was developed by the federal Cybersecurity and Infrastructure Security Agency (CISA) develop strategies for mitigating and addressing supply chain risks

LINKS:

Agencies Extend Comment Period on Proposed Risk Management Guidance for Third-Party Relationships

ICT Supply Chain Risk Management Fact Sheet

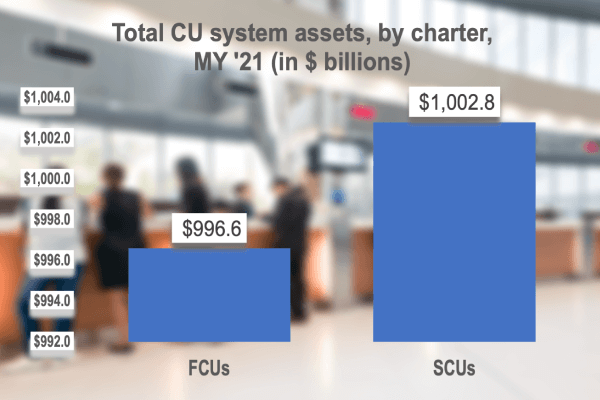

State credit unions now hold more than $1 trillion in assets, representing more than half of all assets held across the credit union system, the latest figures from NCUA show.

State credit unions now hold more than $1 trillion in assets, representing more than half of all assets held across the credit union system, the latest figures from NCUA show.

Mid-year 2021 numbers released this week by the agency (and numbers compiled by NASCUS for privately insured credit unions from American Share Insurance (ASI)) show that the state system holds $1.003 trillion in combined assets (both federally insured, state chartered CUs (FISCUs) and privately insured credit unions (PICUs)). Federal credit unions hold just under the trillion-dollar mark, at $997 billion.

That brings the combined total of assets for all credit unions to just under $2 trillion ($1.99 trillion). As of mid-year, SCUs held 50.2% of total assets, with FCUs at 49.8%.

The numbers also show state credit unions expanded their asset totals slightly faster than federals during the first half of the year, at a rate of 7.35% (compared to 7.02% for FCUs). In memberships, however, the FCUs added more at a faster rate, adding 1.8 million (up 2.77% from year-end). SCUs added just under 1.1 million members (for a 1.79% growth rate). Total memberships at credit unions are now more than 127 million, according to the compiled statistics.

“The trillion-asset mark is a milestone for the state credit union system,” NASCUS President and CEO Lucy Ito said. “It was only in the last decade that the credit union system as a whole reached $1 trillion in assets. This latest achievement is an indication of how consumers have turned to the credit union system – and particularly state credit unions – during these latest days of economic challenges, and a search by savers and borrowers for security and service.”

The NCUA mid-year numbers also show that credit unions saw their net income rise by more than 77% in the first half of 2021, compared to year-end 2020, expanding to $21.3 billion over the six-month period.

Yet, even though credit unions saw growth in assets, memberships and net income, the overall net worth ratio for the credit union industry in the first half of the year actually declined, the NCUA numbers show. At mid-year, the credit union net worth ratio (which is the primary indicator of credit union safety and soundness) fell to 10.17%, down 150 basis points from year-end (when it stood at 10.32%).

However, the net interest margin at credit unions (which is gauged by comparing the net interest income a credit union earns on loans to the interest it pays savers, a key indicator of profitability) remained steady during the first half of the year, at 2.57% of average assets (the same as at the end of the first quarter). That’s the first quarter in the last five that the ratio has not declined. However, the ratio for the second quarter is also tied for the lowest point it has been in the last five years (comparing second quarter figures only).

LINK:

Credit Unions’ Net Income, Insured Shares and Deposits Rise in Second Quarter

(Sept. 10, 2021) Payment provisions in a 2017 rule on payday loans were upheld by a federal court in Texas this week, essentially turning back a challenge to the four-year-old regulation.

The ruling means compliance with the rule will become mandatory in mid-2022.

In a statement, CFPB) Acting Director Dave Uejio said the decision issued in the U.S. District Court for the Western District of Texas reaffirms the agency’s ability to protect borrowers from unfair and abusive payment practices by payday lenders and others covered by the rule.

“Today’s ruling will provide relief to all those who could face these practices,” Uejio said. “The CFPB expects lenders to follow the requirements of the payment provisions, consistent with the court’s order.”

Under the ruling, the mandatory compliance date will be June 13, 2022.

Uejio asserted that the provisions of the rule would prohibit lenders from continuing to attempt to withdraw payment from borrowers’ accounts after two attempts have failed. He said that would protect borrowers from being subject to multiple fees for returned payments or insufficient funds and reduce the risk that consumers’ accounts will be closed.

LINK:

(Sept. 10, 2021) NCUA’s request for information (RFI) on digital assets and related technologies is the latest summary posted on the association’s website; comments are due Sept. 27.

Like all NASCUS summaries, it is available to members only.

In July, the NCUA issued the RFI, with a particular eye on current and potential uses for credit unions and the risks associated with them. NCUA said the effort is to engage the credit union system and other stakeholders in learning how emerging distributed ledger technology (DLT) and decentralized finance (DeFi) applications are viewed and used. In particular, the agency said, it wants feedback on the role NCUA can play in “safeguarding the financial system and consumers in the context of these emerging technologies.”

The agency described DeFi as the broad category of applications adopting peer-to-peer networks to create digital assets like cryptocurrency and crypto-assets, clearing and settlement systems, identity management systems, and record retention systems. DLT (which includes blockchains) consists of a shared electronic database where copies of the same information are stored on a distributed network of computers.

LINK: