(May 7, 2021) State regulators must have access to the same “beneficial ownership” information that federal agencies will have under legislation adopted last year, and made available through a database, NASCUS wrote in a comment to FinCEN submitted this week.

In response to an advance notice of proposed rulemaking (ANPR) issued early last month, NASCUS wrote that to “maintain a seamless and effective oversight of the BSA/AML, FinCEN must include state regulators in the implementation of the Corporate Transparency Act (CTA) to the same extent as federal agencies.”

The CTA, adopted as part of last year’s National Defense Authorization Act (NDAA), allows that the beneficial ownership information submitted to FinCEN may be disclosed to financial institutions (including credit unions) in their compliance with BSA/AML customer due diligence (CDD) requirements. “Beneficial owners” are those individual natural persons who ultimately own or control the reporting companies.

The state system said it supports strengthening the Bank Secrecy Act/anti-money laundering (BSA/AML) framework, and will work with FinCEN as the beneficial ownership database is developed and the CTA implemented. However, NASCUS urged FinCEN to develop a database that reduces information and collection verification burden on credit unions.

“Credit unions and other financial institutions already bear a substantial BSA/AML regulatory burden to safeguard the financial system and work diligently to fulfill their responsibilities,” NASCUS wrote. “Designing the Beneficial Ownership Database in a manner that eases related customer due diligence requirements would allow financial institutions to re-allocate resources to monitoring and other BSA/AML obligations resulting in a more secure financial system.”

LINK:

Comment: Beneficial Ownership Information Reporting Requirements

(May 7, 2021) Possible, additional reporting requirements for state credit unions because of a proposed new rule on credit union service organizations (CUSOs) is a key concern outlined by the state system in its comment letter submitted to NCUA late last week on the proposal.

Overall, the proposal would expand the list of permissible activities for a federal credit union (FCU) CUSO and reserve authority for the NCUA Board to approve additional activities without the traditional notice and comment. Typically, NASCUS wrote, the association does not weigh in on proposals that affect, directly at least, only federal credit unions. However, because this proposal could influence state credit unions considering collaborating with FCU investors in the formation and ownership of a CUSO, the association was prompted to comment.

In some states, NASCUS pointed out, CUSOs owned by state credit unions already hold expanded lending power. The association noted, however, that the NCUA proposal could end up requiring additional reporting requirements that don’t today exist for SCUs. “NASCUS opposes extension of any additional reporting requirements to SCU CUSOs resulting from an expansion of FCU powers,” the association wrote.

NASCUS reminded the agency that SCU CUSOs may now provide many products and services authorized under state law free of restrictions in place for FCU CUSOs – and, in some cases, states already have the authority NCUA is proposing now for FCU CUSOs.

“To date, NCUA, the (National Credit Union) share insurance fund, and the credit union system have been able to manage any risk presented by SCU CUSOs within the existing reporting framework pursuant to existing Part 741.12” of NCUA regulations, NASCUS wrote. The association wrote that nothing in the proposal identifies a pressing need to include SCU CUSOs in any new reporting requirements and “we expect that should NCUA seek to include ALL CUSOs in any reporting requirements the agency would consult with the state regulators and subject proposed SCU CUSO reporting requirements to notice and comment.”

In other comments, NASCUS recommended that the agency:

- allow a limited amount of FCU investment in an SCU CUSO without triggering agency limitations on the state CUSO;

- continue to evaluate prudent changes that enhance a credit union’s ability to serve members and meaningfully engage in the marketplace, after asserting that “collaborating with a CUSO should not be a necessity in order for a credit union to remain vibrant and healthy.”

- permit FCUs to invest with banks, which would be consistent with the state system’s view of the need for greater flexibility for credit union investment.

- continue to work with NASCUS and state regulators to leverage state supervisory oversight of CUSOs and third-party service providers as needed to address any supervisory uncertainty NCUA may have related to any SCU CUSO or other third-party entity.

LINK:

Comment: Proposed Rule, Credit Union Service Organizations (CUSOs) – RIN 3133–AE95

(May 7, 2021) A new federal credit union chartered late last month in Kendall Park, N.J., to serve a local Islamic community will offer its members non-interest-bearing consumer loans, among other services, NCUA said this week. Maun FCU will be an Islamic-faith-based, no-interest credit union whose not-for-profit, cooperative business model will fill a need for affordable, federally insured financial services among members of its community, the agency said in a release. The new credit union will serve employees and members of the New Brunswick Islamic Center in New Brunswick, N.J., and employees and members of the Islamic Society of Central Jersey in Monmouth Junction, N.J. … the Federal Reserve this week called for comments on proposed guidelines it would use to evaluate requests for accounts and payment services at Federal Reserve Banks presented by “novel types” of banking institutions attempting to leverage new and emerging technologies and techniques. Generally, principles outlined in the guidelines would require the requesting entity to be eligible to receive Fed services, and cannot present “undue risk” to the Fed system or the financial system at large.

LINKS:

NCUA Charters Maun Federal Credit Union

Proposed Guidelines for Evaluating Account and Services Requests (PDF)

(May 7, 2021) Apartment landlords were put on notice this week by the CFPB that federal protections are in place to keep tenants from being evicted, at least for the short term, due to the financial impact of the coronavirus crisis.

However, the ruling of a federal court later in the week has placed the future of those protections in doubt without congressional action.

Monday, the bureau announced it – in concert with the Federal Trade Commission (FTC) — had sent letters to companies that the agencies said collectively own more than 2 million apartment units nationwide. “The letters remind these landlords of federal protections in place to keep tenants in their homes and stop the spread of COVID-19,” according to a release from CFPB. “The Centers for Disease Control and Prevention (CDC) has extended until June 30 a temporary moratorium on evictions for non-payment of rent, and the CFPB has issued an interim final rule, which takes effect today, establishing new notice requirements under the Fair Debt Collection Practices Act (FDCPA).”

According to the agencies, the letters ask landlords to examine their practices to ensure they comply with the CDC moratorium and the FTC Act and “remediate any harm to consumers stemming from any such law violations.” The letters also, they said, encourage landlords to notify FDCPA-covered debt collectors working on their behalf, which may include attorneys, of the CDC moratorium, applicable state or local moratoria, and those parties’ obligations under the FTC Act and FDCPA, including the CFPB’s interim final rule.

However, on Wednesday, a federal judge in Washington, D.C., said the CDC acted outside of its authority in extending the temporary eviction moratorium. Ruling in favor of a group of property managers and real estate trade associations, U.S. District Judge Dabney Friedrich vacated the CDC order.

“It is the role of the political branches, and not the courts, to assess the merits of policy measures designed to combat the spread of disease, even during a global pandemic,” the order states. “The question for the Court is a narrow one: Does the Public Health Service Act grant the CDC the legal authority to impose a nationwide eviction moratorium? It does not.”

The status of CFPB’s new rule is now unclear. The Justice Department, however, has indicated it will appeal the judge’s ruling and may ask for a stay in the meantime.

(May 7, 2021) James “Tim” Merritt, assistant administrator of the North Carolina Credit Union Division, has announced his retirement, effective a week from today (May 14) … Meanwhile, in credit union state association leadership developments, Rich Schaeffer has become the new president and CEO of the West Virginia Credit Union League, succeeding long-time CEO Ken Watts, who has retired … In Michigan, Patty Corkery has been appointed president and CEO of the state’s league, succeeding veteran CEO Dave Adams, who resigned (but who remains at the helm of the association’s CUSO, CU Solutions Group).

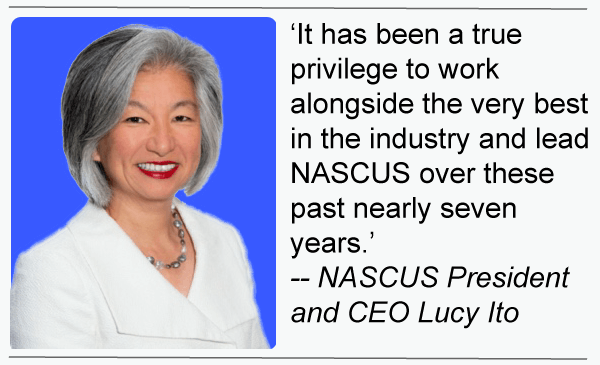

(May 7, 2021) Lucy Ito, NASCUS President and CEO since 2014, will retire from the position at year’s end, she announced this week. The association is conducting a search for a new leader, to take office before Ito departs to allow for a smooth transition.

“Working with both state regulators and credit unions over my entire career has been tremendously fulfilling,” Ito said. “It has been a true privilege to work alongside the very best in the industry and lead NASCUS over these past nearly seven years.”

Ito thanked the NASCUS Regulator Board and the Credit Union Advisory Council for their support and guidance during her tenure at NASCUS, which began in November 2014. “The Regulator Board and Council have worked in true collaboration with myself and the staff; I am grateful for their leadership and friendship.”

But she also noted there is much to do before year’s end. “This transition of leadership at NASCUS will in no way interrupt or dampen our advocacy or our commitment on behalf of the state system,“ she said. “A number of proposed new rules and actions from NCUA, other federal agencies and other entities are in the works that will effect state credit unions. NASCUS will continue to be the voice of the state system throughout the year as these efforts proceed. We also will continue to pursue our own initiatives and events – including the 2021 State System Summit, our annual conference for the state credit union system this summer.”

The NASCUS leader joined the association after serving as executive vice president and chief operations officer at the California and Nevada Credit Unions Leagues. Prior to that, she served as a vice president of the World Council of Credit Unions (WOCCU) working on credit union development issues worldwide.

She currently serves on the International Credit Union Regulators’ Network (ICURN) Board of Directors and Steering Committee, the State Issues Committee of the American Association of Credit Union Leagues (AACUL), and the NCUA-SSA Joint Supervisory Working Group. She also participates in the African-American Credit Union Coalition’s (AACUL) Cross Cultural Exchange Program, a newly launched national pilot initiative.

NASCUS leadership has named a search committee to select a new leader for the association; D. Hilton and Associates, an executive recruiting firm with long ties to the credit union system, has been retained to identify suitable candidates.

(May 7, 2021) Tom Fite, director of the Indiana Department of Financial Institutions, is now chairman of the State Liaison Committee (SLC) of the FFIEC, the group said this week. He will serve a one-year term as SLC chairman from May 1 to April 30, 2022.

Fite was also reappointed to a two-year membership term on the SLC, which he first joined in 2017. Director of the Indiana regulator’s office since January 2016, Fite served before that as deputy director of the department’s depository division and, for 15 years prior to that, served in field examination and regional supervision.

In a statement FFIEC Chairman, and NCUA Board Chairman, Todd Harper congratulated Fite as a fellow Hoosier. “ Tom’s examination and supervision acumen, along with his state regulatory experience and working knowledge of the SLC, make him an ideal choice for Chairman,” Harper said. “I look forward to working with him on the important work of the Council.”

The five-member SLC, in addition to Fite, also includes:

- Steve Pleger, State of Georgia, Department of Banking and Finance senior deputy commissioner, designated by NASCUS; he is a current NASCUS Board member and a former chairman of the Regulator Board;

- Kevin Allard, Ohio Division of Financial Institutions superintendent, designated by the American Council of State Savings Supervisors (ACSSS);

- Melanie Hall, Montana Division of Banking and Financial Institutions commissioner, confirmed by the council; and

- Susannah Marshall, Arkansas State Bank Department commissioner, designated by the Conference of State Bank Supervisors (CSBS.

LINK:

Fite Elected as State Liaison Committee Chairman, Reappointed to FFIEC State Liaison Committee

(May 7, 2021) During her tenure as NASCUS president and CEO, Lucy Ito has been the leader for the state system on a number of issues and initiatives, including:

- Advocating for policies that foster balance and equity between state and federal credit unions, particularly NCUA’s overhead transfer rate (OTR) methodology.

- Creating an environment for state regulators and credit unions to work together to reach common sense solutions.

- Establishing a forum of collaboration for state regulators through events, such as the National Meeting for State Regulators, launched in 2016 and held each spring

- Constructing idea-sharing platforms such as The Exchange—a dialogue for state regulators and CEOs of large stand and federal credit unions (those with $10 billion or more in assets) to anticipate future challenges facing the entire credit union system.

- Partnering with NCUA, including re-committing, for the first time in more than a decade, to the Document of Cooperation between NASCUS and the agency, signed in 2019.

- Rebuilding credit union system involvement in the National Institute for State Credit Union Examination (NISCUE), NASCUS’ education foundation, and expanding scholarship opportunities for state examiners.

- Launching a cohesive and collaborative, member-focused engagement strategy and building nationwide trust in the NASCUS brand.