(Aug. 20, 2021) Continuing and new leadership for the state system was also seated during the NASCUS Annual Meeting, held in conjunction with S3.

Serving as officers for 2021-22 for the NASCUS Regulator Board are:

- Chairman: Rose Conner (administrator, North Carolina Credit Union Division)

- Vice Chairman: Janet Powell (chief of regulation and supervision – credit unions, Oregon Dept. of Consumer and Business Services)

- Secretary/Treasurer: John Kohloff (commissioner, Texas Credit Union Department)

Joining the three as directors on the regulator board are:

- Katie Averill (superintendent, Iowa Department of Commerce, Division of Credit Unions)

- Yolanda Ford (deputy superintendent of banking for community and regional banks, New York State Department of Financial Services)

- Steve Pleger (senior deputy commissioner, Georgia Department of Banking and Finance)

- Charles Vice (commissioner, Kentucky Department of Financial Institutions)

- Mary Ellen O’Neill (director, financial institution division, Connecticut Department of Banking)

Members of the regulator board serve three-year terms (Kolhoff and Ford were elected to new terms this year). However, one member is appointed to serve a one-year term by the chairman; O’Neill holds that seat for 2021-22.

Meanwhile, the NASCUS Credit Union Advisory Council also selected its leadership for the upcoming year:

- Mike Williams, president and CEO, Colorado CU (Colo.), chairman;

- Mike Ryan, senior vice president and general counsel, BECU, (Wash.), vice chairman;

- Jeff Dahlstrom, president, Southeast Financial CU (Tenn.), secretary.

Joining the three as directors are:

- Rick Stipa, immediate past chair and CEO, Trumark Financial CU (Pa.)

- Amy Nelson, CEO, Point West CU (Oregon)

- Cathie Tierney, president/CEO, Community First CU (Wis.)

- Brian Wolfburg, president/CEO, Vystar CU (Fla.)

- Amy Sink, CEO, Interra CU (Ind.)

Like the regulator board members, directors of the CUAC serve three-year terms (Williams, Nelson and Tierney won new terms in elections this year). However, like the regulator board, one member is appointed by the chairman to serve a one-year term; Sink was appointed for the 2021-22 term to that seat.

LINK:

(Clockwise from upper left: NASCUS’ Lucy Ito joins NASCUS Executive Vice President and General Counsel Brian Knight, and NCUA Office of Examination and Insurance Director Myra Toeppe in a discussion of key issues)

(Aug. 20, 2021) The surging Delta variant of the coronavirus is putting a damper on NCUA’s plan to resume on-site operations, including exams, the agency’s top supervisor told the NASCUS S3 conference this week.

According to NCUA Office of Examination and Insurance Director Myra Toeppe, the continued phasing-in of on-site operations depends on the virus variant. She indicated a timetable still needs to be determined. However, the agency is ready (and willing) to go into a credit union whenever it sees a risk to the insurance fund, she said.

“We’ll go in where we need to go in if we see a risk to the insurance fund; we have been clear on that,” Toeppe said during a Tuesday session of the conference. (She was sitting in on the session in place of NCUA Board Chairman Todd Harper, who was unable to attend.) “We do have problem case officers that are doing things. Our regional offices, if we need to be on site, they will get with the (NCUA) executive director to determine from an insurance perspective if we need to go in. We’ve actually had to do some conservatorships during this time. Those are the exception, not the rule.”

But Toeppe emphasized that the agency would move with caution in any event. “People matter,” she said.

The agency’s top examiner also offered a strong defense for NCUA’s call for third-party vendor exam authority. “We do need it,” Toeppe, a former savings and loan regulator, said. “When I first came over to NCUA, I was stunned we didn’t have third-party vendor exam authority. I was used to always having it.” She said her former agency was never accused of abusing the authority, “and it was never a problem.”

Toeppe said NCUA sees reliance “more and more and more” by credit unions on the use of vendors and third parties to help them in a number of areas. She cited data processing and lending as examples.

The agency executive asserted that use of third-party vendors can become a source of risk to the share insurance fund. “And that’s always my focus,” she said. “We want to be sure we aren’t exposing the insurance fund to undue risk. And that’s really where it comes from; it’s a risk perspective for NCUA.”

She added that if the agency secures the authority (which will take an act of Congress to do so), NCUA would use it cautiously. She disputed some reports that the agency would be “ramping up” such as by hiring 500 additional examiners. “I think we’d use (the authority) prudently, where needed, just exactly like the state supervisors have done,” she said. “Where it’s needed, when it’s needed when we see a risk– just like the state supervisors, they’ve used it prudently. The banking regulators use it prudently. I don’t think there would be any difference.

She said that using the authority, when needed, is necessary to avoid a regulatory blind spot. “From (the perspective of) managing the share insurance fund, that makes us very nervous. That’s one thing that keeps me up at night,” she said.

In other comments, Toeppe said:

- Cybersecurity is a persistent threat; the one risk that just doesn’t go away. “We have ebbs and flows of other risks, but cybersecurity just keeps coming,” she said. “It just doesn’t stop, it’s in everything. It’s the constant ‘come at you’ thing. It’s high level, persistent.”

- NCUA is not discouraging mergers among credit unions (as opposed to banking regulators with banks, under an executive order from President Joe Biden). “We don’t tell (credit unions) no you can’t merge, but we want to make sure they are doing the right thing.”

- She has no problem with credit unions buying banks, as long as the transaction is done well and the credit union has done its homework. “Everyone thinks we rubber stamp them,” she said, adding the agency does not. She said the transaction must make sense, and that the agency has be sure of the risk that the insurance fund is taking on with the transaction.

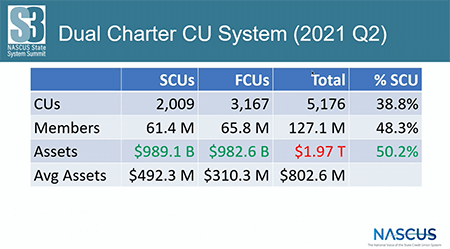

(Aug. 20, 2021) State credit unions are growing their assets and members, spurred to some extent by the financial impact of the COVID-19 pandemic, NASCUS President and CEO Lucy Ito told the opening session of the NASCUS 2021 State System Summit (S3) Tuesday.

Ito’s remarks were among the first at the S3 conference, which assembled a diverse group of more than 115 attendees throughout the country, including state regulators, credit unions, industry partners, and the media. The annual event serves as the state system’s annual conference, and offers a unique opportunity to bring together credit union regulators and practitioners for open dialogue and mutual exchange.

Ito indicated that state credit union asset growth of 21.3% from the end of the first quarter 2020 to end of first quarter 2021 (to $989.1 billion) was astronomical but not surprising, given the influx of savings most financial institutions experienced related to the financial impact of the coronavirus crisis. However, she did say that the membership growth of 3.67% for the period (to 61.4 million) – and decline in the number of state credit unions by just more than 2% (to 1,009) — was typical for the state system.

She noted that the consolidation of credit unions over the last three years, however, has slowed slightly. At year-end 2018, she said, the number of state credit unions dropped by 3.6%; the rate slowed to 2.3% in 2019. Last year, the number dropped at an even slower rate of 2.2%. “Possibly into 2021, consolidation could be slowed a bit in that credit unions may not be pursuing mergers given the other things that they are dealing with,” she said.

Notably, Ito reported, the state system at the end of the first quarter held slightly more than half (50.2%) of all assets in the whole credit union system; memberships were just under the halfway mark, she said, at 48.3%. Overall, two out of every five credit unions (38.8%) are state credit unions. However, state credit unions on average are larger than their federal brethren, at $492.3 million in assets, compared to $310.3 million for FCUs, she pointed out.

On conversions of charters, Ito said over the last 13 years (as of the end of the second quarter of each year), more credit unions (103) with more assets (about $60 billion) have converted from federal to state. She noted, however, that since 2016 when NCUA approved modernization of its field of membership rules for FCUs, that more credit unions have been converting from state to federal (50 conversions to federal charter, versus 40 to states). Those totals include the first two quarters of this year.

However, states continued to gain more assets in the conversions over that time period: $26.4 billion compared to $17 billion for conversions to federal. But that trend may be about to change. So far in 2021, she pointed out, there have been seven conversions, with four of those from state to federal and accounting for $2.4 billion in assets. The three federal to state conversions, she noted, totaled only $328.5 million in assets. “It makes me wonder if this is a turning point in conversions,” she said.

“At this time we have a state and federal system that is basically 50-50,” Ito said. “As we look to the future, factors that will affect future trends (of the share of the market) include continued mergers depending on the size of those and whether or not they change charters; conversions; interstate operations as state borders become less important in people’s lives; and field of membership flexibility.”

She said that, historically, when federal credit unions have converted to states, it is because of the field of membership flexibility that is available in some states, especially the ability to mix and match geographic community fields of membership with associations or with select employee groups.

In other comments, Ito asserted that charter competitiveness within the states will be a key to future growth and success. She noted that parity between credit union charters within states – and even parity between charters of other states (for at least five states: Connecticut, Idaho, Texas, Utah and Washington) or other financial institutions – will play an increasingly large role for states.

“Competitiveness is key; credit unions do need to be able to keep up and compete,” Ito said. “Certainly, as all of us experienced both in our professional and personal lives during the pandemic, just the digitization of our lives accelerated and certainly the pressures on credit unions and other depositories has grown much more intense.”

(Aug. 20, 2021) A proposal by NCUA to create the new “complex credit union leverage ratio (CCULR)” framework — the credit union equivalent of the community bank leverage ratio (CBLR) — is out for public comment until Oct. 15, according to a notice published in the Federal Register this week. Issued for comment during the July 22 NCUA Board meeting, the proposed rule would make a simplified measure of capital adequacy available to federally insured credit unions defined as “complex” – meaning those with more than $500 million in assets … The spread of the Delta variant of the coronavirus and stagnant vaccination rates pose “downside risks” to the economic outlook, according to members of the Fed’s rate-setting Federal Open Market Committee, as expressed in the minutes of the meeting from July 27-28. The minutes were released this week. Committee members also noted economic uncertainty remains high and that supply disruptions and labor shortages might last for longer than anticipated … NCUA is scheduling a Sept. 8 webinar on its modernized examination tools. The session, which gets underway at 2 p.m. ET and runs for an hour, will focus on the new modern examination platforms and systems, including the agency’s Modern Examination & Risk Identification Tool, (MERIT), as well as associated programs: the Data Exchange Application (DEXA), NCUA Connect, and the Admin Portal. The agency said registration is now open.

LINKS:

Capital Adequacy: The Complex Credit Union Leverage Ratio; Risk-Based Capital

Minutes of the Federal Open Market Committee, July 27-28, 2021

Register Now for NCUA’s Modernized Examination Tools Webinar on Sept. 8

(Aug. 20, 2021) Reorganizing its rules to lessen confusion over application of anti-money laundering rules, and working with state regulators to implement those rules, are among the recommendations made by NASCUS in its letter to NCUA concerning the latest annual review of the agency’s regulations.

In February, NCUA asked for comments on its annual review of agency rules, which covers one-third of the regulations (the review is conducted over a three-year period to ensure all agency rules are reviewed at least once every three years). Among the rules being reviewed in 2021: Security program, report of suspected crimes, suspicious transactions, catastrophic acts and Bank Secrecy Act compliance (Part 748 of the agency’s rules), among other things.

The state system offered comments in several areas, including BSA/AML compliance, reporting of suspicious transactions, and organization of NCUA rules (particularly those affecting state credit unions).

Regarding anti-money laundering rules, NASCUS noted that Treasury’s Financial Crimes Enforcement Network (FinCEN) is proceeding with a “no-action letter” program for BSA/AML rules over which that agency has enforcement authority. The program will not affect NCUA rules, NASCUS noted. To mitigate confusion, NASCUS recommended that NCUA rules be reorganized to co-locate or otherwise more clearly identify BSA/AML “FinCEN” rules and NCUA specific rules.

NASCUS also urged NCUA to revisit the monthly requirement that credit union boards be informed of suspicious activity reports (SARs) required under BSA/AML. While that may work for federal credit unions (which are required to meet monthly), NASCUS noted, it does not work for state credit unions where boards are only required to meet quarterly. “In other covered industries, including banking, best practice for reporting to the entity’s board is quarterly, or synchronized to regularly scheduled board meetings,” NASCUS wrote. “NCUA should clarify its expectations for how reporting is handled and make clear that for credit unions with less-than-monthly board meeting, reporting SAR filings at the next available board meeting, or quarterly, would satisfy the regulatory requirement.”

In other comments, NASCUS:

- Reiterated the importance of NCUA working with state regulators to develop regulations to implement the Anti-Money Laundering/Countering the Financing of Terrorism (AML/CFT) National Priorities (National Priorities) as published by the Treasury Department on June 30. NASCUS recommended the agency create a working group with state regulators to develop pending regulations.

- Recommended the agency reinstate the policy of publishing a summary and response to stakeholder comments. “There is real value for stakeholders in understanding NCUA’s response to recommended changes and in gaining insight into the agency’s rational for resisting making various recommended changes,” NASCUS wrote.

- Repeated its call that NCUA reorganize its rules to consolidate and co-locate all National Credit Union Share Insurance Fund (NCUSIF) rules for federally insured credit unions (FISCUs) in one section (or series of consecutive sections), which NASCUS asserted would “provide significant regulatory relief to credit unions without increasing risk to the NCUSIF.”

- Proposed the agency develop a regular review of guidance as a companion to the annual regulatory review. “While not carrying the force of regulation or statute, supervisory guidance provides stakeholders crucial insight into how NCUA interprets compliance with regulation, and as such is just as critical to be regularly evaluated.,” NASCUS wrote.

- Observed that agency rules could be made more consistent by ensuring regulatory provisions containing mandatory elements of compliance contain mandatory language rather than permissive language. “Requirements should also be stated in the active tense such as ‘a credit union shall design its information security program’ rather than passive construction such as a ‘credit union information security program should be designed,’” NASCUS stated.

LINK:

NASCUS comment letter: 2021 NCUA regulatory review

(Aug. 20, 2021) Producing new and updating existing resources that will strengthen the state charter is the aim of new program introduced by NASCUS this week in conjunction with the S3 conference. The association also announced three credit union system organizations have generously contributed to help deliver the program to the state system beginning in 2022.

According to NASCUS’ Lucy Ito, the NASCUS Dual Charter Resource Initiative (DCRI) will support such initiatives as statute modernization in individual states, researching and producing detailed comparisons between the federal and state charters, and producing a curated legislative digest that focuses on select state credit union legislation for strengthening state credit union codes.

The three organizations that have initially pledged to contribute to support the DCRI are CUNA Mutual Group ($150,000), American Share Insurance ($100,000, and PSCU ($20,000). Their contributions total $270,000.

Ito said all three of the initial DCRI partners recognize that a robust dual charter system for the future will assure the continued dynamism of the U.S. credit union system.

The NASCUS leader unveiled the program, and announced the contributions made by the three initial supporters, during the NASCUS president’s report delivered during the association’s annual meeting Tuesday.

“State charter advances benefit the entire credit union system, from state and federal regulators to state and federally chartered credit unions and their members,” Ito said. “It is essential to the system’s vibrancy that we work hand in hand to address the challenges ahead.”

More specifically, Ito said, through the DCRI, NASCUS and contributing partners will, on behalf of a stronger state charter, pursue progressive legislation and regulation, build relationships to foster charter innovation, guard against unnecessary federal pre-emption and expand awareness of options available to state-chartered credit unions.

She said the DCRI will begin development during the coming months and will move into the market early next year. Initiative sponsors will engage with the initiative through a series of financial contributions and program participation, she added.

LINK:

NASCUS Launches Dual Charter Resource Initiative

(Aug. 20, 2021) Also featured at this year’s S3 conference:

- Discussion of the employment challenges and opportunities before credit unions resulting from the coronavirus crisis by nationally recognized employment and human relations speaker (and president of the firm CUDoctor) Diane Reed.

- A review of the economic landscape as the country struggles to emerge from the financial impact of the pandemic by Thomas Siems, senior economist and director of research for CSBS.

- Insights into mortgage lending trends and strategic planning by Tracy Ashfield of Ashfield & Associates, a mortgage lending consulting firm for credit unions.

- Dialog about the problems with the appraiser credentialing system, as well as inequality in real estate appraisals and the impact on borrowers and sellers by NCUA Deputy Director, Office of Examination and Insurance Tim Segerson, and NASCUS General Counsel and Executive Vice President Brian Knight.

“This year’s Summit offered a program aimed at providing insights to key challenges and opportunities to the state system, maximizing attendee engagement, generating creative problem solving, and supporting nationwide interaction to bolster and grow the state system for years to come,” said NASCUS’ Lucy Ito.

(Aug. 20, 2021) Summaries of three recent issuances from NCUA – on capitalizing loans, the rollout of the new examination tool, and on mortgage servicing rules – were published by NASCUS this week.

All three are available to members only. The summaries cover issuances – two letters to credit unions and one regulatory alert – issued by the agency over the last three weeks or so.

Early this month, the agency issued letter to credit unions (LTCU) 21-CU-07, which outlined limits on capitalization of loans to members. In particular, the letter pointed out, the financing of fees and commissions continue to be prohibited for federally insured credit unions, despite adoption of the new rule earlier this year allowing capitalization of loan interest. In the letter, the agency said that maintaining the prohibition on capitalization of fees “is an important consumer protection feature of the rule for member borrowers.”

In June, the agency’s board voted unanimously to lift the prohibition of capitalization of interest in connection with loan workouts and modifications; the rule took effect July 30. The change was made, NCUA said, to give borrowers additional access to loan workouts, perhaps caused by the economic disruption caused by the coronavirus crisis.

The second letter (LTCU 21-CU-08) summarized listed the new applications (and their implementation) the agency is employing for assisting in exams and communicating to credit unions. The letter, issued just last week, noted that the agency would begin transitioning to its new Modern Examination and Risk Identification Tool (MERIT) exam tool and other applications meant to modernize and streamline the agency’s operations. The other tools include the Data Exchange Application (DEXA), the Administrative Portal, and the Consumer Access Process and Reporting Information System (CAPRIS) for federal credit unions.

The letter also offers insights about who at credit unions can use the new tools, and how the tools integrate with state supervisory authority (SSA) examination and supervision programs.

The third item summarized by NASCUS and published this week is of a regulatory alert (21-RA-08), which urges review of CFPB mortgage servicing rules. According to the alert, credit unions are urged to review the June 30 rule temporarily amending certain mortgage servicing requirements under the bureau’s Regulation X to assist borrowers affected by the COVID-19 emergency. The alert noted that the CFPB rule — which takes effect Aug. 31 — only applies to servicers that service mortgages secured by a borrower’s principal residence and does not apply to small servicers.

LINKS:

NASCUS summary: LTCU 21-CU-07, Capitalization of Unpaid Interest (members only)

NASCUS summary: LTCU 21-CU-08, Implementation of Modernized Systems (members only)

NASCUS summary: 21-RA-07 Equal Credit Opportunity Act (Regulation B) (members only)