(Sept. 24, 2021) Earlier in the meeting, the NCUA Board voted – 2-1, with Harper the “no” vote – to act on three outstanding proposed rules over the span of the final three months of the year. Under the board’s vote, an expanded list of permissible activities and services of CUSOs would be considered for final action at the board’s Oct. 21 meeting

Action on two other outstanding proposals – on FOM shared service facility requirements, and mortgage servicing – were also scheduled for action at upcoming board meetings (Nov. 18 and Dec. 16, respectively). All three rules have been awaiting final action since this spring, following the close of their comment periods.

The CUSO proposal would allow the origination by a service organization of any type of loan that a federal credit union may originate, and grant the NCUA Board additional flexibility to approve permissible CUSO activities and services. In the comment request, the agency also sought comments on broadening federal credit unions’ authority to invest in CUSOs.

The proposal was issued by the NCUA Board Jan. 14, also on a vote of 2-1, with then-Board Member Harper dissenting (he became chairman later that month). Harper, making his objection, noted the NCUA’s lack of direct supervisory authority over CUSOs and indicated the proposal raised potential consumer protection concerns.

He essentially repeated those objections at Thursday’s meeting, calling the proposal the “wrong rule at the wrong time.” He asserted that the rule is not related to COVID-19 pandemic relief, and more likely to cause harm to small credit unions rather than help them. “It will grow an already unregulated space within the credit union system with little accountability to consumers and credit unions,” Harper said.

He also reiterated a call (which he has made before Congress) for NCUA to have oversight authority of CUSOs and other third-party vendors.

Regarding the FOM shared service facility requirements and mortgage servicing proposals, the NCUA chairman voiced continued opposition to both, but also aired some optimism about “a path forward” for each.

Under the FOM shared service facility requirements, any federal credit union shared branch, ATM, or electronic facility would meet the definition of “service facility” for membership requirements in multiple-common-bond FCU that participates in a shared branching network, thus expanding membership reach of federal credit unions. Under the mortgage servicing proposal, the agency’s investment regulation would be amended to permit FCUs to purchase mortgage servicing rights from other federally insured credit unions subject to certain conditions.

Those two proposals were issued for comment in December, on a vote of 2-1 for both with Harper dissenting on both.

Thursday’s action on the three proposals was advanced jointly by Vice Chairman Kyle Hauptman and Board Member Rodney Hood. They presented a joint memo to the board for approval that set the meeting dates, specifically meant to force action on the three outstanding proposals. “The items put forth by this Board Action Memorandum shall be brought before the Board as final rules in the timeframe set by this action. Nothing in this action should be construed to alter NCUA’s obligations under the Government in the Sunshine Act,” their memo stated.

LINK:

Board action memorandum: Action on NCUA Board Agenda Items for 2021

(April 30, 2021) Issues and policies being pursued by the state system were outlined this week by NASCUS President and CEO Lucy Ito during a presentation hosted by CU*Answers’ “The CUSO Challenge.”

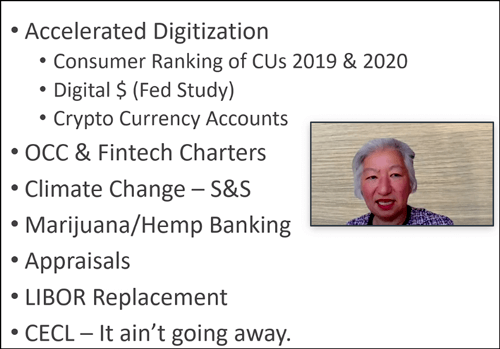

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

Ito also laid out NASCUS’ approach for “renovating” the Federal Credit Union Act, to bring the underlying federal line more in line with contemporary times, and to give the state system (which now represents more than half of the total assets of the entire credit union system) fair representation.

Among other things, Ito recommended separating the insurance function from the supervisory role of NCUA, a long-standing position of the association. NASCUS’ position is that the current structure of the National Credit Union Share Insurance Fund (NCUSIF) presents a potential conflict of interest within the agency unless those functions are internally separated. (NASCUS has also noted that any changes to the statutory structure of the NCUSIF should be evaluated and developed in conjunction with state regulators and credit union stakeholders, since state regulators have experience and expertise with statutory and operational construct of the bank deposit insurance fund that would help inform possible changes to the insurance fund.)

She also noted NASCUS’ support for expanding the NCUA Board from three to five members. In any event, NASCUS also supports reserving one seat on the board for a person with experience as a state credit union regulator.

Other renovations to the FCU Act mentioned by Ito included: updating field of membership, regulatory capital, member business lending and investments authorities, and considering changes to board compensation, annual meeting and member expulsion requirements.

FOR IMMEDIATE RELEASE

August 20, 2019

CONTACT: Shelton Roulhac, NASCUS Communications; [email protected]

IN WAKE OF APPEALS COURT DECISION UPHOLDING MOST OF NCUA’S FOM RULE, NASCUS’ ITO PRAISES NCUA’S DETERMINATION TO MAINTAIN AN EFFECTIVE FEDERAL CHARTER

Arlington, VA – In a victory for NCUA and the credit union system, the District of Columbia Circuit Court of Appeals upheld virtually all aspects of NCUA’s Field of Membership Rule, overturning the lower district court which had struck down two provisions of the rule.

NASCUS President and CEO Lucy Ito issued the following statement in response to the ruling:

“NASCUS congratulates NCUA on the field of membership ruling and commends the Agency’s efforts to maintain an effective federal charter. We have long held that a competitive federal charter is vital to preserving a robust dual charter system and today’s ruling certainly advances that goal.”

###

Information Contact:

Shelton Roulhac, Vice President, Communications, [email protected] (703) 528-5974

NASCUS is the national association that advocates for a strong and healthy state credit union system, and whose members include state regulatory agencies, credit unions, credit union leagues, and organizations that support the state credit union system.