Agency Accepting Comments and Budget Briefing Presentation Requests

Agency Accepting Comments and Budget Briefing Presentation Requests

Sept. 29, 2022 — The National Credit Union Administration’s staff draft budget for 2023–2024 is now available on the agency’s website for review and comment. The staff draft budget has also been submitted for publication in the Federal Register, and the comment period is open until October 28, 2022.

The proposed combined 2023 staff draft budget is $367.0 million, or 8.1 percent higher than the 2022 budget. The proposed operating budget is $350.8 million, which is 9.6 percent higher than in 2022. The proposed 2023 capital budget is $11.2 million, or 14.1 percent lower than in 2022. The proposed Share Insurance Fund administrative budget is $4.9 million, or 21.5 percent lower than in 2022. The proposed budget summary and detailed budget justifications can be found on the Budget and Supplementary Materials page on NCUA.gov.

The agency will hold a public budget briefing at its Central Office on Wednesday, October 19, 2022, beginning at 10 a.m. Eastern. The meeting will be livestreamed on NCUA.gov.

To Comment on the Proposed Budget:

- Submit comments on Docket # NCUA-2022-0145 at the Federal eRulemaking Portal by October 28, 2022.

- Comments should provide specific, actionable recommendations.

To Request an In-Person Presentation at the October 19 Budget Briefing:

- Email your request to [email protected] by October 12, 2022.

- Include the presenter’s name, title, affiliation, mailing address, email address, and telephone number.

- The Board Secretary will notify approved presenters and give them their allotted presentation times.

For those approved to present at the budget briefing, written statements and presentations must be sent to [email protected] by 5 p.m. Eastern on October 14, 2022. In addition to delivering remarks at the budget briefing, registered presenters will have the opportunity to pose questions about the budget to NCUA staff.

The Board will consider a final budget at an open meeting later this year.

Sept. 22, 2022 — As various government agencies and reports use slight inflationary easing to show the economy isn’t in such bad shape, there’s an unescapable chill in the air, and it’s not just winter. It’s the cold reality that living is less affordable than ever.

Sept. 22, 2022 — As various government agencies and reports use slight inflationary easing to show the economy isn’t in such bad shape, there’s an unescapable chill in the air, and it’s not just winter. It’s the cold reality that living is less affordable than ever.

To track these trends, PYMNTS has partnered with LendingClub on the “New Reality Check: the Paycheck-to-Paycheck Report,” an ongoing series tracking how Americans at various income levels and in different demographics are affording — if just barely — the cost of living.

In a conversation with PYMNTS’ Karen Webster, LendingClub CEO Scott Sanborn pushed past recent marginal improvements to Labor Department inflation numbers, pointing to the fact that credit card balances are growing, delinquencies are rising and we don’t have the full picture.

What remains unspoken, he said, “is the way they report delinquencies is on their entire outstanding percentage of delinquent loans on their outstanding portfolio. The thing about credit cards is I think the average age of the balance is between five and seven years. You have this massive amount of balance that’s old, that’s very stable.”

While personal loan delinquencies are not apples to apples as a credit card comparison, he said that “if you look by vintage, the quarterly [credit] delinquencies are fanning like crazy, and none of them are talking about it.”

Portfolio delinquencies may look okay, but that’s a function of time and new balances which haven’t had time to hit issuers yet.

“Just compare the first six months of credit cards issued in Q2 of this year versus the first six months in any of the last 5 to 10 years,” he said. “They look remarkably worse, but nobody’s talking about it.”

See also: NEW DATA: US Consumers Face Emergency Expenses 3.5x Larger Than Fed Estimates

Webster marveled at the fact that the Apple Card is being offered to subprime borrowers with scores as low as 620 to 660 given that backdrop. Sanborn sees that as an unavoidable buy-on terms trap that manufacturers/retailers like Apple are now stuck in.

He said, “As a retailer, the idea that somebody walks into the Apple Store and says, ‘I’d like to buy a new iPad,’ and you say, ‘No, I’m sorry, you can’t have one,’ that’s the business of extending credit. It’s super painful for people who aren’t in the business of credit.”

To keep that machine making sales and not declining brand loyalists, Apple and others are demanding and committing to approval rate minimums from their finance partners — in Apple’s case, Goldman Sachs — some of which end up in that delinquency pile.

‘A Fundamental Misunderstanding’

On the larger issue of perceptions around paycheck-to-paycheck living in America, the most recent New Reality Check study found that 59% of U.S. consumers lived paycheck to paycheck in July, down from 61% in June. However, on the 12-month view, it trended up from 54% in July 2021.

These consumers exist on a continuum of living check to check, from comfortably handling monthly expenses to struggling to meet rising costs, with more now falling behind. Asked why paycheck-to-paycheck consumers are often written off as “poor” or irresponsible, Sanborn sees decades of pile-on effects that erased hard-won benefits like pensions as the real culprit.

“There’s just a fundamental misunderstanding,” he said. “There’s room for interpretation on what does it mean to live paycheck to paycheck? And if what you think of living paycheck to paycheck is you use your paycheck to cover only 100% discretionary items and then you’re out, that is a definition. But the reality is, who’s to determine what’s discretionary?”

Learn more: How Did $1,400 Become the ‘New’ Average Emergency Expense?

Running down the list — transportation, dining, contributing to 401k and HAS plans — he said these could be considered “discretionary” as much as date night, underscoring the confusion.

Here again, Sanborn invoked perception versus reality. Noting that “$370 billion worth of deposits left the system — that’s a record, that is people tapping into their savings,” he said it’s also clear in retail sales trade-downs and rents that are now up 15% year over year.

“Back to this point of being poor and living paycheck to paycheck are not the same thing,” he continued. “Yes, the inflation over the last year has been acute, but over the longer arc of the last 20 years, cost of housing, cost of healthcare, cost of education are all going up exponentially, and over that entire 20-plus-year period, wages have only recently in the last two years started to move.”

Paycheck-to-Paycheck Living Hits Crisis Levels

His underlying point is that perceptions of paycheck-to-paycheck consumers are hopelessly outdated and misaligned with the financial realities of 2022, and even prior years.

Illustrating his point, he said, “If you are able to have a credit card that has a balance, you’re credit worthy. Equating it to whether it’s a lower income [individual] or lower credit quality is not accurate. The data does not support that. Why else would 54% of Americans have credit card debt that they do not pay off? If they had the capacity to pay it off, they would.”

In a move to give struggling consumers options, LendingClub acquired Radius Bancorp in 2021, adding savings accounts to its portfolio in a bid to help consumers boost their financial health.

Sanborn said, “We’re helping them legitimately find savings by offering one of the highest rates possible on the savings account in the country. That’s the commercial aspect. But the human aspect, the broader the policy aspect is we’re all talking about the climate crisis and that’s real. This is also a crisis, and it’s also real, and it is also happening. We have this massive bubble of people heading toward retirement that are not going to be able to afford retirement.”

Conceding that there’s no silver bullet solution, Sanborn believes housing, healthcare and retirement are three major areas deserving public-private action with urgency.

![]() Filene is hitting the road to bring the latest research where it matters most, your backyard!

Filene is hitting the road to bring the latest research where it matters most, your backyard!

| REGISTER | EVENT DETAILS |

We all know there is more value in gathering in three-dimensions, but with overbooked flights and long travel days, it’s hard to make the time. Filene is taking the hassle of flight delays and long layovers off the table by bringing our research on the road in our new series of Filene Roadshows!

Join us on Tuesday, September 27 for this exclusive opportunity to engage directly with Filene Fellow, Dr. Jeffrey Robinson from our Center for Innovation and Incubation. We are packing in a full afternoon of brain food that will leave you ready to turn innovative ideas into action back at your organization.

This event is free to attend but seats are limited.

Location: Affinity Federal Credit Union

73 Mountainview Blvd

Basking Ridge, NJ 07920

Chairwoman of the House Committee on Financial Services, delivered the following statement at a Subcommittee on National Security, International Development, and Monetary Policy hearing entitled, “Under the Radar: Alternative Payment Systems and the National Security Impacts of Their Growth.”

Thank you very much, Chairman Himes, for convening this hearing on the current and future national security challenges related to the growth of alternative payment systems. These systems can drive inclusion and offer convenience, but because they are generally outside of the western financial system, they also offer opportunities for sanctions evasion and other financial crime.

Further, they rival U.S. dollar-led trade and payments systems, potentially undermining the strength of the dollar and our ability to leverage tools like economic and trade sanctions. So, I look forward to hearing from today’s witnesses on what Congress needs to consider regarding this growing concern.

Research by Boston Fed economist finds borrowers and lenders incentivized to take more risk

Research by Boston Fed economist finds borrowers and lenders incentivized to take more risk

September 15, 2022 — In 2010, researcher Mattia Landoni obtained access to data on thousands of short-term loans known as “repos” that were issued in the three years before the 2007-2008 financial crisis. But like many of his colleagues, Landoni assumed that data on repos would be boring since they were generally thought of as safe. He did not take a closer look at it until 2014, at the urging of fellow researcher Jun Kyung Auh.

He quickly realized he was wrong: Repos were not boring. In fact, the lack of transparency into how they are made or how lenders manage risk has implications that could impact the economy’s fragility, said Landoni, now a senior financial economist at the Federal Reserve Bank of Boston.

“We need to understand what we are seeing here, or we could be just as blindsided by the next financial crisis as we were in 2007,” said Landoni, who works in the Bank’s Supervision, Regulation & Credit department.

Landoni and Auh teamed up on a paper that examines risk-taking associated with repos, “Loan Terms and Collateral: Evidence from the Bilateral Repo Market,” which is forthcoming in The Journal of Finance. The researchers find that repo loans against low-quality collateral are riskier than those against high-quality collateral. But they also find that there are incentives for both lenders and borrowers to continue engaging in these riskier loans.

The researchers said lenders appear to take more risk and receive more compensation when collateral quality is lower, and loans against low-quality collateral are cheaper for borrowers.

Quality, transparency of securities used as collateral varies widely

“Repo” is short for “repurchase agreement,” a short-term, collateral-backed loan. A “bilateral” repo is between two parties. The firm acting as the borrower agrees to sell securities – such as stocks and bonds – to another firm, and then repurchase those same securities at a higher price. The securities act as collateral, meaning the buyer keeps them if the seller breaks the agreement.

But the quality of the collateral varies widely. The researchers observed two main types of securities used as collateral: mortgage-backed securities and collateralized debt obligations.

Landoni said mortgage-backed securities have some degree of transparency because they are backed by real estate loans.

“You can list each mortgage by zip code, so you know exactly what is going into that (security),” he said.

Collateralized debt obligations are backed by a pool of loans and assets, and are, in theory, no more or less risky than mortgage-backed securities. But the researchers found that they are less transparent and more complex, making it harder to assess their value. And, Landoni said, “They were of lower quality, on average.”

Paper: Loans against lower-quality collateral are riskier, but attractive

For their paper, Landoni and Auh created a dataset of more than 13,000 “uncleared” repo loans – meaning they were made directly between two parties. The loans were made between a large hedge fund and major financial institutions from 2004-2007.

The length of the loans spanned one day to six months, and their principal amounts ranged from about $30,000 to more than $700 million, with a median of about $10.5 million.

The researchers analyzed the data and studied the prices of securities being used as collateral. They also created a model to determine what was causing patterns they observed in the dataset.

They found that, despite their higher margins, repo loans against lower-quality collateral were riskier than loans against higher-quality collateral. But both lenders and borrowers had incentives to engage in these riskier loans.

Why? The researchers said it relates to lender optimism and a behavior called “reaching for yield:” Lenders offer a relatively cheaper loan to a borrower with lower-quality collateral in exchange for the chance to take more risk and potentially earn more money.

Since borrowers can get cheaper loans using low-quality collateral, they have an incentive to continue buying it. And that gives the firms that produce securities used as low-quality collateral an incentive to keep creating them.

The researchers said it is critical to continue learning more about this market as the risks lenders take there could have significant impacts on the overall economy.

Landoni said efforts are ongoing to gather more information about the bilateral repo market. He added that he hopes the study helps inform a pilot program in the U.S. Treasury’s Office of Financial Research that is focused on establishing data collection and disclosure protocols.

Courtesy of Amanda Blanco, Federal Reserve Bank of Boston

Sept. 22, 2022 — NCUA held it’s first in-person board meeting since the start of the COVID-19 pandemic. The board thanked the NCUA staff for all of their efforts.

The Board unanimously approved two items:

- A notice of proposed rulemaking, NCUA Part 701, Appendix A, Federal Credit Union Bylaws, Member Expulsion

- A notice of proposed rulemaking, NCUA Part 702, Subordinated Debt

Proposed Rule, NCUA Part 701, Appendix A, Federal Credit union Bylaws, Member Expulsion

- On March 15, 2022, Congress enacted the Credit Union Governance Modernization Act of 2022. Under the statute, NCUA has 18 months following the date of enactment to develop a policy by which a federal credit union (FCU) may be expelled for cause by a two-thirds vote of a quorum of the FCU’s board of directors. The proposed rule would amend the standard FCU bylaws to adopt such a policy. The 18-month period to adopt a final rule enacting a policy on member expulsion ends September 15, 2023.

- NCUA Chairman Todd M. Harper Statement on the Member Expulsion Proposed Rule

Proposed Rule, Part 702, Subordinated Debt

- The proposal would make two changes to the Subordinated Debt rule (Current Rule) related to the maturity of Subordinated Debt Notes and Grandfathered Secondary Capital. Specifically, this proposal would replace the maximum maturity of Notes with a requirement that any credit union seeking to issue Notes with maturities longer than 20 years demonstrate how such instruments would continue to be considered “debt.”

- This proposed rule would also extend the Regulatory Capital treatment of grandfathered secondary capital to the later of 30 years from the date of issuance or January 1, 2052.

- The proposed rule would also make four minor modifications to the Current Rule to make it more user-friendly and flexible. Specifically, the proposal would:

- amend the definition of “Qualified Counsel” to clarify that such person(s) is not required to be licensed to practice law in every jurisdiction that may relate to an issuance.

- amend two sections of the Current Rule to remove the “statement of cash flow” from the Pro Forma Financial Statements requirement and replace it with a requirement for “cash flow projections.”

- revise the section of the Current Rule on filing requirements and inspection of documents.

- the proposal would remove a parenthetical reference related to grandfathered secondary capital that no longer counts as Regulatory Capital.

- Read: NCUA Chairman Todd M. Harper’s Statement on Amendments to the Subordinated Debt Rule

Each proposal will have a 60-day comment period upon publication in the Federal Register.

June 30, 2022: NCUSIF briefing

Read all Board Member statements from this meeting.

- The Board was briefed on the June 30, 2022 – NCUSIF

- The Equity Ratio – as of June 30, 2022, the Equity Ratio remained the same from December 2021 at 1.26%.

- The NCUA projects the NCUSIF equity ratio to reach 1.30 percent for period ending December 31, 2022.

Each board member stressed that while the fund is stable with an increase in the ratio projected, the board must proceed carefully when making any decisions about the share insurance fund due to inflation and increased operating costs. They also stressed the importance of monitoring and managing liquidity issues in the industry due to the significant increase in interest rates.

The board also discussed the expiration of CARES Act relief and the need for Central Liquidity Facility agent membership. The board stressed they will continue to work with Congress.

Ongoing growth in home and auto lending means the industry is gradually shedding the high liquidity levels brought on by pandemic relief programs.

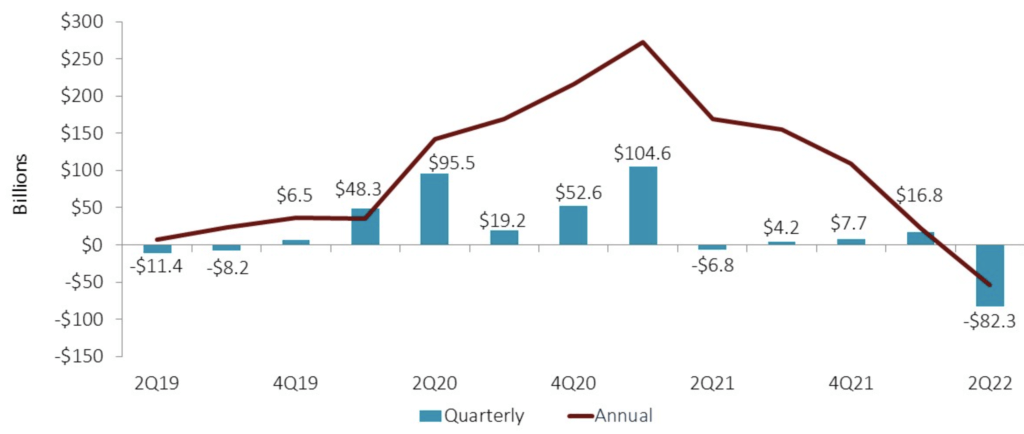

Courtesy of CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

Take Aways

- The federal government took a variety of steps to provide economic relief during the first year of the pandemic, including distributing trillions of dollars directly to consumers. As a result, credit union shares grew at record rates – well outpacing loan growth – leading to sizeable increases in liquidity. However, with the pandemic now mostly in the rearview mirror, credit unions are beginning to unwind the liquidity built up during the crisis. Credit unions reported 6.6% quarterly growth in outstanding loan balances as of 2Q22, well outpacing share growth over the same period, leading to liquidity outflows of $82.3 billion since March. This is a large change from 1Q22, when liquidity moderately increased by $16.8 billion.

- As economic activity expands, this liquidity is being converted from cash into impactful loans. Overall, the dollar value of loans rose by $86.6 billion in the second quarter, increasing total loans by 6.6%. This expansion was driven by credit union members taking out loans for first mortgages (up $26.8 billion this quarter, or 5.36%) and used cars (up $18.4 billion this quarter, or 6.72%). Both growth rates are five-year highs. The loan-to-share ratio has increased from 70.22% in March to 74.73% at the half-year mark.

- Not only is this loan growth helping members purchase homes and cars, it also translates to an impact on earnings for credit unions. As cash balances are converted into loans, credit unions increase earnings off the higher yield. Net interest margin is beginning to tick up, rising 10 basis points from the end of March to 2.67%.

- Rising interest rates make it unclear whether this record loan demand will continue. However, the effects of the economic reopening and federal relief funds on the demand for auto and home financing has certainly led to a repurposing of credit union liquidity.

Federal Reserve’s Michael Barr highlights priorities in initial public remarks

Sept. 7, 2022—The Federal Reserve’s new regulatory chief said Wednesday that the central bank is considering how to more-closely scrutinize bank mergers and may beef up the way it requires certain banks to plan for their own demise.

Sept. 7, 2022—The Federal Reserve’s new regulatory chief said Wednesday that the central bank is considering how to more-closely scrutinize bank mergers and may beef up the way it requires certain banks to plan for their own demise.

Read Barr’s entire remarks here “Making the Financial System Safer and Fairer”

The remarks from Fed Vice Chairman Michael Barr, his first in public since taking office July 19, suggest a more aggressive approach to overseeing Wall Street than his Republican predecessor Randal Quarles.

Mr. Barr said he aims to evaluate how the Fed reviews proposed bank tie-ups and to assess “where we can do better,” speaking at an event hosted by the Brookings Institution, a Washington think tank.

The remarks are consistent with those from others made by the Biden administration and its top regulators, who are seeking to address concerns that the steady growth of the nation’s largest regional banks has introduced new risks to the financial system. While these firms might lack the vast trading floors and international operations of megabanks such as JPMorgan Chase & Co. and Bank of America Corp., the biggest regionals’ balance sheets are now approaching the size of some of so-called systemically important banks.

The push to revamp the way regulators assess the mergers of large banks is in its early stages but could make bank tie-ups more difficult.

“These risks may be difficult to assess, but this consideration is critical to assess how we are performing merger analysis and where we can do better,” Mr. Barr said Wednesday.

The remarks were being closely watched by banks and officials to get a sense of Mr. Barr’s priorities.

He spoke about so-called living wills, or plans for banks to wind themselves down in a crisis without a government bailout. Mr. Barr said regulators need to continue to analyze whether firms are taking “all appropriate steps to limit the costs to society of their potential failure.” He also warned about the so-called resolvability of some larger regional banks that have grown in size and in importance to the financial system.

Mr. Barr’s remarks didn’t go into detail on whether he plans to alter bank capital and liquidity levels through changes to the central bank’s rulebook or its annual “stress tests,” which aim to determine how large lenders would react to drastic market and economic shock.

Still, he suggested he was looking at ways to beef up stress tests, the value of which some critics say has eroded over time, becoming less stressful for banks. “The stress tests need to continue to evolve,” Mr. Barr said. “They’re supposed to be stressful. They’re supposed to be tough. And I want to make sure that they are that way.”

He said he would have more to say about certain bank-capital requirements in the fall. Mr. Barr has previously said he wants to get a broad view of requirements before pushing for adjustments to rules piece by piece.

Industry groups, such as the Bank Policy Institute and the Financial Services Forum, had no immediate comment on Mr. Barr’s remarks.

Mr. Barr’s supervision role is the government’s most influential bank overseer, responsible for developing a vision for the regulation of big banks and other financial firms. That includes developing policy recommendations for the Fed board and for overseeing its regulatory staff, which supervises some of the largest U.S. financial firms, including JPMorgan, Bank of America and Citigroup Inc.

Mr. Quarles, who previously held the Fed supervision post, focused on simplifying financial regulations enacted after the 2008-09 financial crisis. Supporters say those moves clarified or better calibrated the central bank’s rules. Some Democrats say they significantly softened the impact of the Wall Street rulebook. Mr. Quarles left the Fed in December.

At the event, Mr. Barr also addressed monetary policy. He said inflation was too high and that the Fed was committed to bringing it down. Acknowledging that the Fed’s rate increases risk a further slowdown to the economy—and even some pain—he said it is far worse to let “inflation continue to be too high.”

He didn’t specify how high the Fed’s benchmark interest rate should rise.

Mr. Barr was the last of President Biden’s slate of five appointees to the central bank. Fed Chairman Jerome Powell and three other appointments were confirmed in recent months.

Formerly a dean of public policy at the University of Michigan, Mr. Barr also served in the Treasury Department during the Clinton and Obama administrations, including as a top lieutenant to then-Treasury Secretary Timothy Geithner. Mr. Barr played a role as an architect of the 2010 Dodd-Frank financial overhaul, including the law’s creation of the Consumer Financial Protection Bureau.

Courtesy Andrew Ackerman, Wall Street Journal

Cyber Criminals Increasingly Exploit Vulnerabilities in Decentralized Finance Platforms to Obtain Cryptocurrency, Causing Investors to Lose Money

SUMMARY

The FBI is warning investors cybercriminals are increasingly exploiting vulnerabilities in decentralized finance (DeFi) platforms to steal cryptocurrency, causing investors to lose money. The FBI has observed cybercriminals exploiting vulnerabilities in the smart contracts governing DeFi platforms to steal investors’ cryptocurrency. The FBI encourages investors who suspect cybercriminals have stolen their DeFi investments to contact the FBI via the Internet Crime Complaint Center or their local FBI field office.

THREAT

Cybercriminals are increasingly exploiting vulnerabilities in the smart contracts governing DeFi platforms to steal cryptocurrency, causing investors to lose money. A smart contract is a self-executing contract with the terms of the agreement between the buyer and seller written directly into lines of code that exist across a distributed, decentralized blockchain network. Cybercriminals seek to take advantage of investors’ increased interest in cryptocurrencies, as well as the complexity of cross-chain functionality and open source nature of DeFi platforms.

Between January and March 2022, cybercriminals stole $1.3 billion in cryptocurrencies, almost 97 percent of which was stolen from DeFi platforms, according to the US blockchain analysis firm Chainalysis. This is an increase from 72 percent in 2021 and 30 percent in 2020, respectively. Separately, the FBI has observed cybercriminals defraud DeFi platforms by:

- Initiating a flash loan that triggered an exploit in the DeFi platform’s smart contracts, causing investors and the project’s developers to lose approximately $3 million in cryptocurrency as a result of the theft.

- Exploiting a signature verification vulnerability in the DeFi platform’s token bridge and withdraw all of the platform’s investments, resulting in approximately $320 million in losses.

- Manipulating cryptocurrency price pairs by exploiting a series of vulnerabilities, including the DeFi platform’s use of a single price oracle,(a) and then conducting leveraged trades that bypassed slippage checks (b) and benefited from price calculation errors to steal approximately $35 million in cryptocurrencies.

RECOMMENDATIONS

Investment involves risk. Investors should make their own investment decisions based on their financial objectives and financial resources and, if in any doubt, should seek advice from a licensed financial adviser. In addition, the FBI recommends investors take the following precautions:

- Research DeFi platforms, protocols, and smart contracts before investing and be aware of the specific risks involved in DeFi investments.

- Ensure the DeFi investment platform has conducted one or more code audits performed by independent auditors. A code audit typically involves a thorough review and analysis of the platform’s underlying code to identify vulnerabilities or weaknesses in the code that could negatively impact the platform’s performance.

- Be alert to DeFi investment pools with extremely limited timeframes to join and rapid deployment of smart contracts, especially without the recommended code audit.

- Be aware of the potential risk posed by crowdsourced solutions to vulnerability identification and patching. Open source code repositories allow unfettered access to all individuals, to include those with nefarious intentions.

The FBI recommends DeFi platforms take the following precautions:

- Institute real time analytics, monitoring, and rigorous testing of code in order to more quickly identify vulnerabilities and respond to indicators of suspicious activity.

- Develop and implement an incident response plan that includes alerting investors when smart contract exploitation, vulnerabilities, or other suspicious activity is detected.

a Price oracles are tools that query, retrieve, and verify price information about a given asset used by the DeFi platform’s smart contracts.

b Slippage refers to price difference between when a transaction is submitted and when the transaction is confirmed (validated) on the blockchain. Slippage checks are designed to minimize or eliminate slippage.