(Nov. 25, 2020) With changes coming to the membership of the NCUA Board, NASCUS believes now is a good time to consider some changes in how the NCUA Board is constructed – namely, requiring that at least one member of the board have state credit union regulator experience, and increasing the size of the NCUA Board from three to five members.

NASCUS and the state system have long advocated the changes.

“A board member who has served as a state credit union regulator would ensure that the state perspective is considered in the board’s deliberations, establish diversity of voices and better foster a robust dual charter system,” said NASCUS’ Ito. “State-chartered credit unions represent 50% of all credit union assets nationwide. The majority of state-chartered credit unions are federally insured. Without at least one board member with state credit union regulatory experience, NCUA is prone to a federal credit union bias as both the chartering body for federal credit unions and insurer of both federal and state credit unions.”

Increasing the size of the NCUA Board from three to five members would allow for better communications among the members without triggering formal meeting requirements (under the federal open meetings laws), and would raise the quality of debate, exchange of perspectives and transparency of operations, Ito said.

“Governance best practice recognizes that too few directors can pose the risks of less transparency and a concentration of power,” Ito said. “Indeed, NCUA credit union rules require federal credit unions to have at least five board members for these reasons.”

Making the changes won’t be as simple as flicking a switch, Ito noted: Congress will have to amend the Federal Credit Union Act to realize both. “However, the state system believes that, going forward, these changes will benefit the agency and the overall credit union system,” Ito said. “We pledge to work with any and all members of Congress to help them adopt these changes.”

(Nov. 25, 2020) Nominations for the NASCUS 2020 Pierre Jay Award – which recognizes the individuals, programs or organizations whose contributions have benefited the state credit union system in a significant way – are due Dec. 31,.

The award will be conferred during a virtual event in the first quarter of 2021.

Honoring those who have demonstrated outstanding service, leadership and commitment to NASCUS and the state system, the Pierre Jay Award was first conferred in 1997 and has been presented to an individual nearly annually since then. It honors the first Commissioner of Banks in Massachusetts, Pierre Jay. The 2019 winner was Mary Hughes, formerdirector, Idaho Department of Finance.

NASCUS members may nominate any person, program, or organization who or that has made a significant contribution to the state credit union system is eligible to be nominated. Nominees do not necessarily need to be affiliated with NASCUS. Examples of individuals, programs or organizations to be nominated include credit union organizations, volunteers (including committee members), staff members, or chief staff executives; and, state/federal organizations, state/federal lawmakers, state/federal regulators, or others.

LINK:

Pierre Jay Award: Details, nomination form

(Nov. 25, 2020) Physical risks posed to financial stability by climate change – even in the short term — include a sharp fall in asset prices and an increase in uncertainty, according to a new report issued this week by an international group of financial regulators.

However, the group said, another key risk to financial stability could be a disorderly transition to a low-carbon economy, brought about by an “abrupt change in (actual or expected)” public policy not anticipated by market participants, including that due to the increased materialization of physical risks, as well as technological developments.” The report — The Implications of Climate Change for Financial Stability – was released by the Financial Stability Board (FSB), a Basel, Switzerland-based organization made up of national authorities responsible for financial stability in 24 countries and jurisdictions, and others. FSB is chaired by Federal Reserve Board Vice Chair for Supervision Randal Quarles.

The report comes after the credit unions and banks in New York in October were advised by their state regulator to integrate financial risks from climate change into their governance, risk-management and business strategy frameworks, reportedly the first time a state supervisory agency for financial institutions has taken that approach.

The New York State Department of Financial Services said the guidance followed similar direction given to state-regulated insurers. October’s action, the agency indicated, would ensure that all of its regulated entities are managing climate risks. The letter was advisory only; it outlined no supervisory actions to be taken by the agency.

LINKS:

The Implications of Climate Change for Financial Stability

Letter from NY DFS: climate change and financial risks

(Nov. 25, 2020) NASCUS President and CEO Lucy Ito expressed the state system’s thanks to McWatters for his efforts as both a member and chairman of the NCUA Board for more than six years. “During his tenure, particularly as chairman of the board, Mark was receptive and responsive to the views and ideas of the state system,” Ito said. “For example, he was the first board member in 20 years to objectively assess the old, opaque overhead transfer rate (OTR) methodology and challenge the agency to do more than tweak it, which resulted in a complete overhaul of the methodology to be more fair, more equitable, and more transparent. In a number of other areas – notably risk-based capital and, especially, subordinated debt – Board Member McWatters carefully listened, concisely analyzed, and fairly evaluated the needs of the state system, as well as the entire credit union community. We thank him for his service, and wish him well going forward.”

(Nov. 25, 2020) The office of credit unions of the Michigan Department of Insurance and Financial Services has earned a five-year accreditation following an in-depth review and assessment by a panel of veteran credit union state supervisors, sponsored by the NASCUS.

The accreditation for the credit union office of the Michigan DIFS resulted from a robust process that includes disciplined self-evaluation, peer review and ongoing monitoring. The process is administered by the NASCUS Performance Standards Committee (PSC) and measures a state regulatory agency’s ability and resources to effectively carry out its regulatory and supervisory programs.

To earn accreditation, a credit union state supervisory agency must demonstrate that it meets accreditation standards in agency administration and finance, personnel and training, examination, supervision and legislative powers.

“Accreditation is credible evidence of an agency’s capabilities, which also benefits credit unions in the state as well,” said NASCUS President and CEO Lucy Ito. “It provides recognition of the professionalism of a state agency’s regulators, supervisors and staff, and may also deliver the impetus and support for legislation that modifies and/or modernizes state law.

She said the achievement also benefits state-chartered credit unions, as it illustrates how a state regulatory agency has met the highest levels of regulatory proficiency,” she added.

More than 85% of state-chartered credit union assets are supervised by NASCUS’ 28 accredited state agencies. The NASCUS Accreditation Program was adopted in 1989 to administer and assure the quality standards of states’ credit union examination and supervision. Modeled on the university accreditation concept, the program applies national standards of performance to a state’s credit union regulatory program.

LINK:

NASCUS Accreditation Program

(Nov. 25, 2020) A proposal to modernize NCUA rules on derivatives, particularly to make it more “principles based” has been summarized by NASCUS and posted on the association’s website. The summary is available to members only.

The proposal, according to NCUA on Oct. 16 when the board approved its release for a 60-day comment period, is designed to provide more flexibility for federal credit unions to manage their interest rate risk (IRR) through the use of derivatives, while retaining key safety and soundness components.

The agency also said on proposal that the changes would “streamline” the rule and give credit unions more authority to purchase and use derivatives for managing interest-rate risk. The proposal also, NCUA said, reorganizes rule content related to loan pipeline management into one section, which it said would aid in readability and clarity.

NASCUS CEO Ito emphasized at the time the rule was proposed that state credit union derivative authority properly rests with state supervisors, and that they have the experience to apply that power. She noted that state supervisory authorities have extensive experience with derivatives and interest rate swaps both in state-chartered credit unions and community banks, and can play a role as the final rule is developed applying their experiences and lessons to the rule-making.

She also described NCUA’s move to streamline its derivative regulation as “pro-active in anticipation of increased interest rate risk given current low-rate environment and likely long-term rate increases.”

LINK:

Summary: NCUA Proposed Rule (FCUs Only); Derivatives Part 703 (members only)

(Nov. 25, 2020) Model privacy forms from the CFPB that many credit unions and banks use to disclose their information-sharing practices to their members and customers should be updated, according to a report issued this week by the Governmental Accountability Office (GAO).

The report, requested by Senate Banking Committee Chairman Mike Crapo (R-Idaho), said the current model form provided under the Gramm-Leach-Bliley Act (GLBA) for required disclosures gives consumers only a limited understanding of institutions’ information sharing. The GAO specifically recommended that the CFPB update the model privacy form and consider including more information about third-party sharing.

Noting that the GLBA-related model privacy form, providing a safe harbor under the law, was created more than 10 years ago, the report states it thus provides a limited view of what information is collected and with whom it is shared. GAO said consumer and privacy groups interviewed by the GAO cited similar limitations.

The proliferation of data-sharing since the form’s creation in 2009 “suggests a reassessment of the form is warranted,” the report adds.

The bureau, in response to the report, said it would consider doing updating the form, adding that it would require a joint rulemaking with other agencies.

LINK:

CONSUMER PRIVACY: Better Disclosures Needed on Information Sharing by Banks and Credit Unions (GAO-21-36)

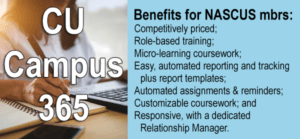

(Nov. 25, 2020) Have you met CU Campus 365 yet? Why not introduce yourself over the Thanksgiving holiday! CU Campus 365 is a new benefit for NASCUS credit union members in alliance with BAI, the industry leader in compliance training, with a history of more than 95 years in the financial services industry.

With the adverse effects of a global pandemic, credit unions need affordable, efficient, and comprehensive solutions for compliance training and professional skills learning. CU Campus 365 provides the solutions, with the latest in courseware and the BAI Learning Manager, a learning management system (LMS) specifically designed to meet the demands of the financial services industry. With it, credit unions have the tools they need to minimize compliance risk and increase employee development.

With the adverse effects of a global pandemic, credit unions need affordable, efficient, and comprehensive solutions for compliance training and professional skills learning. CU Campus 365 provides the solutions, with the latest in courseware and the BAI Learning Manager, a learning management system (LMS) specifically designed to meet the demands of the financial services industry. With it, credit unions have the tools they need to minimize compliance risk and increase employee development.

NASCUS’ credit union members recently received an invitation to learn more about CU Campus 365’s powerful training solutions. Click on the link below to learn more – or visit nascus.org!

LINK:

Welcome to CU Campus 365!

(Nov. 25, 2020) An “S” component (for market sensitivity) in the CAMEL examination rating system remains on the radar for NCUA in 2021, especially now that the agency’s information systems are being updated through the Enterprise Solutions Management (ESM) program.

According to a semiannual report to Congress by the agency’s Office of Inspector General (OIG) made public recently (reporting on agency activities from April 1 to Sept. 30), the addition of this component – S, which will turn the CAMEL rating system into CAMELS – will require revision to the liquidity component (L) to only include liquidity content and criteria, not interest-rate risk.

“(NCUA) Management indicated that adopting the ‘S’ (Market Sensitivity) for the CAMEL rating system involves public notice and comment, NCUA Board approval, and cohering regulation, examination procedures, and system changes,” the report states. “As part of the Enterprise Solutions Modernization program, NCUA is updating the examination platform to incorporate the ability to assign and capture the ‘S’ component as an optional part of the CAMEL rating. Management indicated they expect to have this system change in place in 2021.”

The report also states that agency management noted that the system change will provide the agency the flexibility to adopt the “S” rating if the Board so chooses, and to capture the “S” rating for federally insured state-chartered credit unions in the states where the state regulators adopted the “S” rating.”

NASCUS, which supports including the component in the agency’s rating system, has determined that at least 24 states have already adopted it in their rating system. NASCUS’ Ito said the state system also commends NCUA Chairman Hood for his consistent interest in state agency supervisory practices in adopting the “S” rating for credit unions. “The ‘S’ rating is more relevant than ever since credit unions will face growing interest rate risk as the Federal Reserve eventually allows rates to rise in concert with economic recovery that takes place in the coming years,” she said.

LINK:

NCUA Semiannual Report to Congress (April 1–September 30, 2020)

(Nov. 25, 2020) Change is coming to the NCUA Board in the next 10 days or so, following change that already occurred late last week with the resignation of one of the board members. Here’s a quick rundown of what happened late last week, what’s scheduled to happen next week, and a look at what may be ahead for leadership of the agency.

- Last week, Senate Majority Leader Mitch McConnell (R-Ky.) announced (via the Senate’s executive calendar, which lists when executive branch nominees will begin to be considered by the Senate) that the nomination of Kyle S. Hauptman to be a member of the NCUA Board would be considered as early as Monday of next week (Nov. 30). Hauptman was nominated by outgoing President Donald Trump (R ) last summer to take the seat of J. Mark McWatters, whose term expired in August 2019; McWatters has been serving in a holdover capacity until his successor (Hauptman) was confirmed by the Senate. McWatters is a former chairman of the NCUA Board (succeeded by current Chairman Rodney Hood last year), who was named to that position by Trump.

- On Thursday, during the regular monthly meeting of the NCUA Board, both Board Members McWatters and Todd Harper expressed some dissatisfaction with the proposed NCUA budget for 2021, which is scheduled to be the subject of a Dec. 2 briefing by the agency (and which NASCUS has requested to provide comments for). McWatters also announced that he would not support the 2021 staff budget as drafted “as long as I’m on this board.” The NCUA Board is scheduled to consider the 2021 budget at its next monthly meeting, set for Dec. 17.

- Late Friday, McWatters released a copy of a letter he said he had sent to Trump that day informing the president that he was submitting his resignation. “As the Senate is scheduled to confirm my successor in the next few days, I hereby resign my position as of today,” McWatters wrote.

- Monday, Hood publicly released a statement noting McWatters’ resignation, observing that “his years on the NCUA Board are a credit to his decades-long career in law and policymaking. I wish Mark all the best in his future endeavors.” (NCUA Board Member Todd Harper – who also voiced concerns about the budget – released a statement on social media reading (in part) “Mark leaves the Board with a commendable record of achievement, and I wish him well in his future endeavors.”)

The end result of all of this: When the NCUA Board meets Dec. 17 to consider the 2021 budget – including the overhead transfer rate (OTR) for the NCUSIF portion of the agency spending plan – there could be one new face on the board, and perhaps two votes in favor of the agency’s budget for next year.

Looking ahead, with the transition of President-elect Joseph R. Biden (D) now officially underway in advance of the Jan. 20 transfer of power from Trump, there is likely to be more change. The new president will be in a position to designate a new chairman of the NCUA Board (that position is not confirmed by the Senate if the individual has already been confirmed as a board member). As the only Democrat-appointee on the board, Harper is in line to become the next NCUA Board chairman if the president decides to take action.

The most recent example of the president tapping a member of his own party to be chairman: McWatters was named acting chairman of the agency board by Trump on Jan. 26, 2017 – six days after taking the oath of office as president. McWatters replaced Rick Metsger who remained on the board (ultimately to be succeeded by Hood). The “acting” part of McWatters’ title was removed by Trump in June of that year.

Harper’s term on the board ends in April; however, he may serve on the board until a successor is confirmed by the Senate. Hood’s term ends in August 2023; Hauptman, if confirmed, would inherit a term that runs to August 2025.