9 ballot measures chart path for marijuana biz banking

Voter decisions next week on ballot measures in nine states about legalizing marijuana possession and use will likely set the stage for the next steps in how regulators and state-chartered financial institutions will deal with financial transactions involving marijuana businesses.

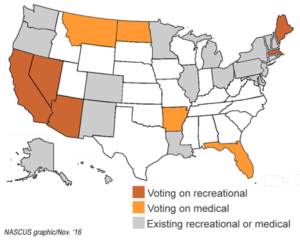

On Tuesday, voters in Arizona, California, Maine, Massachusetts and Nevada will vote on legalizing recreational use.At the same time, Arkansas, Florida, Montana and North Dakota will decide on legalizing medicinal use (the states proposing recreational use already have approved medicinal use). According to one estimate, the decisions in these states will affect a combined 82 million residents – or about one in four persons in the nation’s population (California alone makes up 47% of the populations of the deciding states).

On Tuesday, voters in Arizona, California, Maine, Massachusetts and Nevada will vote on legalizing recreational use.At the same time, Arkansas, Florida, Montana and North Dakota will decide on legalizing medicinal use (the states proposing recreational use already have approved medicinal use). According to one estimate, the decisions in these states will affect a combined 82 million residents – or about one in four persons in the nation’s population (California alone makes up 47% of the populations of the deciding states).

If all of these measures are approved by voters, more than half of the states (29, and the District of Columbia) would have legalized recreational or medicinal – or both – uses of marijuana for their jurisdictions. And that could lead to more pressure building on state credit unions and their regulators on how to handle financial transactions related to legalized marijuana – as well as pressure on the federal government to offer some clarification on doing so (which NASCUS is seeking). The substance remains classified as a Schedule 1 drug (the same as heroin), a rating that was reiterated by the federal Drug Enforcement Agency just this past August. That continues to hamper the ability of businesses serving the legal marijuana trade in their states from opening checking accounts, obtaining credit cards or wire transfer services, largely because financial institutions are reluctant to provide services out of fear of violating federal drug laws. As a result, many of the businesses resort to stashing cash in storage units, back offices and armored vans – which is quickly becoming a security issue.

NASCUS will be watching the results in order to gauge the impact on state regulators and credit unions. While the association supports federal legislation that clarifies the permissibility of financial institutions to provide financial services to state-authorized marijuana businesses (and acknowledging states’ rights issues), NASCUS takes no position on any of the ballot measures.

NCUA URGES DISMISSAL OF BANKERS’ LAWSUIT OVER MBL RULE

NCUA has urged a federal court to dismiss a banker group’s lawsuit challenging the new member business loan rule, arguing that the law’s cap on business lending does not extend to purchase of nonmember business loans or participation interests as the bankers had claimed. The lawsuit was brought in September by the Independent Community Bankers of America (ICBA), a national banking trade association, challenging the new MBL rule’s provision which allows federally insured credit unions to exclude purchased commercial loans or participations in such loans from the aggregate cap on MBLs (contained in section 1757(a) of the Federal Credit Union Act, which was enacted by the Credit Union Membership Access Act (CUMAA) of 1998). “Although ICBA may disagree with the NCUA’s judgments in this area, the agency’s interpretation is consistent with the plain text of Section 1757(a), and nothing in the statute or CUMAA’s legislative history provides any basis for displacing the agency’s interpretation,” NCUA stated in its motion for dismissal, which was filed Wednesday by the U.S. Justice Department on behalf of the agency.

The NCUA response makes four key points countering the bankers’ action. Those are: that the bankers’ group lacks standing because it alleges “no certainly impending injury in its complaint” traceable to the 2016 MBL rule; that the bankers’ claims are not ripe because the new MBL rule is not yet effective and has not been applied to specific transactions (the rule goes into effect in January); that the bankers fail to state a claim upon which relief can be granted, because NCUA has adopted a “permissible construction” of the FCU Act, and; that the action is “in substance” a challenge to the 2003 MBL rule and is thus “time-barred.” “Although the Complaint is styled as a challenge to the 2016 MBL Rule, Plaintiff’s allegations and requested relief all pertain to matters resolved in the 2003 rulemaking,” the NCUA response stated, referring to a rule adopted that year which excluded participation interests from the calculation of the aggregate MBL limit, but distinguished between member and nonmember participation interests. The NCUA response noted that, under precedent, “any challenge to the 2003 Final Rule was required to be filed no later than October 1, 2009—six years after the NCUA published that Rule. This action, filed nearly thirteen years after the Rule’s publication, is thus time-barred.”

LINK:

Memorandum in support of NCUA motion to dismiss ICBA MBL lawsuit

WASHINGTON JOINS SE REGIONAL INTERSTATE AGREEMENT

Washington has joined the Southeastern Regional Cooperative Interstate Agreements, which eases any procedural impediments for the state’s credit unions in branching into the eight other states. In addition to Washington, the Southeastern agreement includes Alabama, Florida, Georgia, Illinois, Mississippi, Missouri, North Carolina, and Tennessee). Washington was already a member of the Nationwide Cooperative Agreement for the Supervision of State Chartered Credit Unions, which includes (not including Washington) nine states (Idaho, Illinois, Indiana, Kentucky, Michigan, Ohio, Oregon, West Virginia and Wisconsin). Both agreements were developed by the engaged states with NASCUS. The Southeastern agreement (developed in 2009) is intended to promote fair and equitable commerce among state-chartered credit unions based upon reciprocity, subject to appropriate safety and soundness provisions, in order to best serve the consumers of the respective states that enter into the agreement.

LINK:

Southeastern Regional Cooperative Interstate Agreement

PAPIEZ TAKES THE REINS IN WASHINGTON (SUCCEEDING JARVIS)

Gloria Papiez is the acting director of the Washington Department of Financial Institutions, assuming the post Tuesday following the retirement of long-time director Scott Jarvis. Formerly deputy director for nearly 11 years, she joined DFI in 2000 and previously worked as assistant director of administration at the Washington State Utilities and Transportation Commission, and assistant director of audit at the Washington State Auditor’s Office. She also served as a board member on the Financial Managers Advisory Council, is a member of the Washington Society of Certified Public Accountants, and currently serves on the governor’s Results Washington Goal Council for efficient, effective and accountable government. In a release, Washington Gov. Jay Inslee (D) called her “a dedicated public servant with a tremendous amount of state financial regulation experience.”

COMPENDIUM DETAILS RULES AFFECTING FISCUS UNDER NCUA

How many times have you asked yourself “why aren’t all of the NCUA rules affecting federally insured, state-chartered credit unions in one place, so I can easily find what’s what?” That question has now been answered, with the publication by NASCUS (in conjunction with BECU of Tukwila, Wash.) of the Part 741 Compendium: Quick Reference to State Rules Under NCUA, now available on the NASCUS website (members only). The Compendium is separated into five parts:

- Subpart A – Regulations That Apply to Both Federal Credit Unions and Federally Insured State-Chartered Credit Unions and That Are Not Codified Elsewhere in NCUA’s Regulations

- Subpart B — Regulations Codified Elsewhere in NCUA’s Regulations as Applying to Federal Credit Unions That Also Apply to Federally Insured State-Chartered Credit Unions

- Appendix A to Part 741—Examples of Partial-Year NCUSIF Assessment and Distribution Calculations Under §741.4;

- Appendix B to Part 741—Guidance for an Interest Rate Risk Policy and an Effective Program

- Appendix C to Part 741—Interpretive Ruling and Policy Statement on Loan Workouts, Nonaccrual Policy, and Regulatory Reporting of Troubled Debt Restructured Loans

According to NASCUS President and CEO Lucy Ito, the compendium offers an integrated roadmap to Part 741. “For years we have heard from both state regulators and credit union practitioners of the need for an easy-access guide to the state rules under NCUA – and this publication serves that request.” Ito noted that the Compendium will be updated on a regular basis, to reflect changes in regulation.

LINK:

CONFERENCE OFFERS WEALTH OF INFO ON BSA/AML

Detecting terrorist financing, the state of cannabis, effective anti-money laundering model risk governance, elder abuse, lessons from internal controls, BSA and the payments system, controls on beneficial ownership — plus dialogue with regulators from FinCEN, NCUA, OFAC and more — are all topics highlighted at this year’s NASCUS/CUNA BSA Conference in just two weeks in San Antonio. The Nov. 13-16 session at the Grand Hyatt San Antonio features more than 20 hours of educational sessions, plus four hours of pre- and post-conference sessions (on profiling human trafficking and building BSA/AML risk assessment, respectively). Participants also receive access (for three months after the conference) to pre‐recorded, online video sessions covering BSA compliance issues in mergers, money services businesses (MSBs), cyber security, and BSA resources. Additionally, those attending the conference earn 20 credits towards their Certified Anti-Money Laundering Specialist (CAMS) designations. See the link for more information.

LINK:

NASCUS/CUNA 2016 BSA Conference (Nov. 13-16, San Antonio)

… AND MARK YOUR 2017 CALENDARS FOR SUMMIT, CYBERSECURITY AND MORE

Mark your calendars for upcoming premiere events from NASCUS in 2017, now in the planning stages: NASCUS State System Summit, Aug. 30-Sept. 1 (San Diego); NASCUS/CUNA Cybersecurity Symposium, June 5-6 (San Diego); State Regulator National Meeting, March 20-21 (for regulators only; Washington, D.C./National Harbor); NASCUS/CUNA BSA Conference, Nov. 12-15 (Las Vegas). See you in 2017!

LINK:

NASCUS education calendar, 2016-17

BRIEFLY: On the road with NASCUS; CFPB guidance about service providers

NASCUS is on the road again this week, with EVP and General Counsel Brian Knight attending the Northwest Credit Union Association’s Attorney’s Conference (for CU attorneys in Washington and Oregon), presenting on state issues, particularly those related to cybersecurity and the regulatory response … NASCUS has posted a summary of the CFPB’s compliance bulletin and policy guidance (2016-02) on “service providers,” which makes it clear that the bureau “expects supervised banks and nonbanks to oversee their business relationships with service providers in a manner that ensures compliance with Federal consumer financial law.” See the link for more details.

LINK:

NASCUS Summary: CFPB Compliance Bulletin and Policy Guidance 2016-02; Service Providers

Information Contact:

Patrick Keefe, NASCUS Communications, [email protected] or (703) 528-5974

For more information about NASCUS's news and/or public relations, please contact our Marketing and Communications Department.