(April 30, 2021) NASCUS opens its human resources (HR) webinar series in May, setting the stage for even more events in June on issues related to marijuana and hemp those facing senior examiners from supervisory agencies.

The HR webinar series, which begins May 19, features Diane Pape Reed, president of CUDoctor, a full-service consultancy and training company. She is also co-founder of the annual CUNA Human Resources Compliance Certification School and was VP of Sales and Administration for a mid-sized Credit Union for 10+ years.

In the May 19 session, Reed will focus on building team trust and managing remote employees. In a May 26 session, she will highlight common remote management missteps and how managers can avoid them.

Both virtual sessions are one-hour long and begin at 2 p.m. ET.

In June, NASCUS plans two events: a three-day virtual school on marijuana and hemp issues, and its senior examiner forum.

The June 9-11 Marijuana and Hemp eSchool looks at recent regulatory updates, how businesses are evolving in the sector, what financial institutions should be considering in developing their own cannabis and hemp banking programs, and business payments (among other things).

The virtual e-school is led by Deirdra O’Gorman, founder and principal of DX Consulting. Since 2015, she has also served as CEO of The Fourth Corner Credit Union (4CCU), the first credit union chartered in more than 10 years in the state of Colorado.

Earlier in the month, on June 2, NASCUS holds its senior examiner forum (from 1:30-3:30 p.m. ET). The session focuses on confidential, but frank, dialogue on such issues as the new MERIT exam program, virtual examinations, cybersecurity, secondary capital and more.

For information on registration and complete agendas for all of the programs, see the links below.

LINKS:

HR Webinar series: Managing Remotely – Time to De-Stress and Establish Trust (May 19)

(April 30, 2021) Issues and policies being pursued by the state system were outlined this week by NASCUS President and CEO Lucy Ito during a presentation hosted by CU*Answers’ “The CUSO Challenge.”

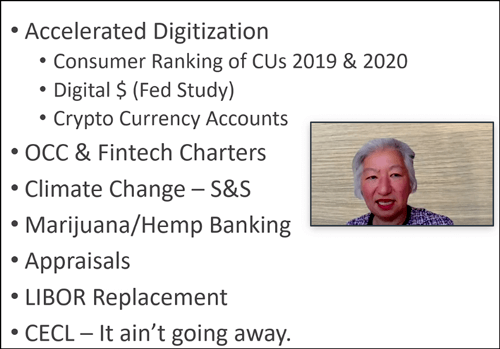

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

Ito also laid out NASCUS’ approach for “renovating” the Federal Credit Union Act, to bring the underlying federal line more in line with contemporary times, and to give the state system (which now represents more than half of the total assets of the entire credit union system) fair representation.

Among other things, Ito recommended separating the insurance function from the supervisory role of NCUA, a long-standing position of the association. NASCUS’ position is that the current structure of the National Credit Union Share Insurance Fund (NCUSIF) presents a potential conflict of interest within the agency unless those functions are internally separated. (NASCUS has also noted that any changes to the statutory structure of the NCUSIF should be evaluated and developed in conjunction with state regulators and credit union stakeholders, since state regulators have experience and expertise with statutory and operational construct of the bank deposit insurance fund that would help inform possible changes to the insurance fund.)

She also noted NASCUS’ support for expanding the NCUA Board from three to five members. In any event, NASCUS also supports reserving one seat on the board for a person with experience as a state credit union regulator.

Other renovations to the FCU Act mentioned by Ito included: updating field of membership, regulatory capital, member business lending and investments authorities, and considering changes to board compensation, annual meeting and member expulsion requirements.

(April 30, 2021) A two-page fact sheet that lays out what’s behind the demise of the London Interbank Offer Rate (LIBOR), a widely used rate used for such lending products as adjustable rate mortgages, has been published by the New York Fed’s Alternative Rate Reference Committee (ARRC). The fact sheet explains (among other things) LIBOR, the problems it poses, why it is being replaced at the start of next year, and the Fed’s favored replacement for the rate, the Secured Overnight Financing Rate (SOFR). A “part II” of the sheet, available separately (and linked to the first fact sheet) outlines how SOFR will work … Readings on inflation are likely to rise more in the coming weeks before moderating,Federal Reserve Chair Jerome H. (“Jay”) Powell said this week, adding that, ultimately, there will only be a “transitory” effect on inflation. Powell said the rise in inflation indicators will be partially due to supply bottlenecks from a rebound in spending as the economy continues to reopen. Those indicators likely will also be driven by emerging reports of a strengthening economy: Real GDP increased at a seasonally adjusted annual rate of 6.4% during the first quarter of 2021, the federal Bureau of Economic Analysis said this week. In the fourth quarter of last year, real GDP increased 4.3%.

LINK:

Background on USD LIBOR

(April 30, 2021) The proposed delayed compliance dates for two debt collection rules from CFPB issued under the Fair Debt Collection Practices Act (FDCPA) has been summarized by NASCUS and is now posted on the association’s website.

This latest summary, like all of those developed and published by NASCUS, is available to members only.

Under the proposal, the two debt collection rules (which had been slated to take effect Nov. 30) will now have a delayed compliance deadline of Jan. 29, 2022. The bureau, when it issued the proposal, said the delay is intended to give those affected more implementation time amid the ongoing challenges of the COVID-19 pandemic.

Late last year, the bureau issued two final (in October and December) under the FDCPA. The October final rule focused on the use of communications related to debt collection and clarified prohibitions on harassment and abuse, false or misleading representations, and unfair practices by debt collectors when collecting consumer debt. The December rule clarified disclosures debt collectors must provide to consumers at the beginning of collection communications. It also prohibited debt collectors from making threats to sue, or from suing, consumers on time-barred debt; and requires debt collectors to take specific steps to disclose the existence of a debt to consumers before reporting information about the debt to a consumer reporting agency.

But the bureau, earlier this month, determined that the COVID-19 pandemic had caused “widespread societal disruption, with effects extending into 2021.” In light of that disruption, the agency said, providing additional time for review – and implementation – of the new rules “may be warranted.”

The rules adopted last year permit debt collectors to choose to comply with the rules’ requirements and prohibitions ahead of their effective date. However, the CFPB noted, in proposing the delay, said that the FDCPA and other applicable law would continue to govern debt collectors’ conduct, with safe harbors and presumptions implemented only as of the rules’ effective date.

Comments are due May 19.

(April 30, 2021) More complaints – particularly about credit or consumer reporting — were received in 2019 and 2020, on a per capita basis, from consumers living in predominantly minority counties than from consumers in predominantly white, non-Hispanic counties, the CFPB said this week in its April 2021 Complaint Bulletin.

Additionally, the bureau said, those consumers living in counties with the highest minority percentages submitted complaints at more than four times the rate compared to counties with the lowest percentage of minority populations.

Credit or consumer reporting appears to cause significantly more issues for consumers in predominantly minority counties, the bureau said, and added that consumers living in predominantly minority counties submitted more complaints on a per capita basis in nearly every one of the 11 product categories about which the agency accepts complaints.

The agency also gave some insights to future reporting: it said it will soon expand its demographic collection to include household size and income. That will include, CFPB said, enhancing the agency complaint form to give consumers the option to provide household size and household income when submitting a complaint.

Any additional information the bureau may need to help better understand the experiences of diverse communities that submit complaints will also be explored in the future, CFPB said.

LINK:

CFPB April 2021 Complaint Bulletin

(April 30, 2021) Compliance with a final rule on “qualified mortgages” (QM) is delayed to Oct. 1, 2022, the CFPB said this week, asserting that the pause would allow lenders more time to offer the loans based on homeowners’ debt-to-income (DTI) ratios, and not only on certain pricing thresholds.

The delay, which changes the mandatory compliance date from July 1 of this year to the Oct. 1 date of next year, is part of a final rule the CFPB is calling the “April 2021 Amendments to the ATR/QM Rule.” ATR stands for “ability to repay.”

In a release, the bureau said the action was taken to “help ensure access to responsible, affordable mortgage credit, and preserve flexibility for consumers affected by the COVID-19 pandemic and its economic effects.”

“As the mortgage market navigates an uncertain and challenging time, extending the date by which lenders must comply with the CFPB’s new General QM definition will help provide options and flexibility for both lenders and borrowers,” CFPB Acting Director Dave Uejio said in a statement.

The bureau also asserted that delaying the QM compliance date by more than a year would give lenders more time to use the Government-Sponsored Enterprise (GSE) Patch, which has also been extended to Oct. 1 of next year – or until the date that the applicable GSE exits conservatorship, whichever comes first. The agency said the GSE patch provides QM status to loans that are eligible for sale to GSE mortgage companies Fannie Mae or Freddie Mac. “The availability of the GSE Patch after July 1, 2021 may be limited by recent revisions to the Preferred Stock Purchase Agreements entered into by the Department of the Treasury and the Federal Housing Finance Agency,” the bureau noted.

According to an executive summary of its final rule issued Tuesday, the CFPB said that while the April 2021 final rule extends the general QM final rule’s mandatory compliance date, the effective date of the QM rule remains March 1, 2021.

The summary notes that for mortgage applications on the effective date (or after) – but before the new mandatory compliance date of Oct. 1, 2022 – lenders have the option of complying with either the revised, price-based general QM loan definition or the original, total monthly DTI-based general QM loan definition.

Only the revised, price-based general QM loan definition is available for applications received on or after the Oct. 1, 2022 mandatory compliance date, the summary states.