Join us October 24-27, 2022

This event is structured specifically for examiners to build the necessary skill sets and enhance their level of knowledge around a core area of topics. NASCUS is proud to present a collective group of experts ranging from compliance to market risk, national issues, and loan profitability.

Location: Hotel Indigo Traverse City

263 W. Grandview Pkwy

Traverse City, MI 49684

Cost to attend: $600 Examiner Members and $700 Non-Member Fee

Questions: Click here to contact Isaida Woo, Ed.D, Vice President, Education

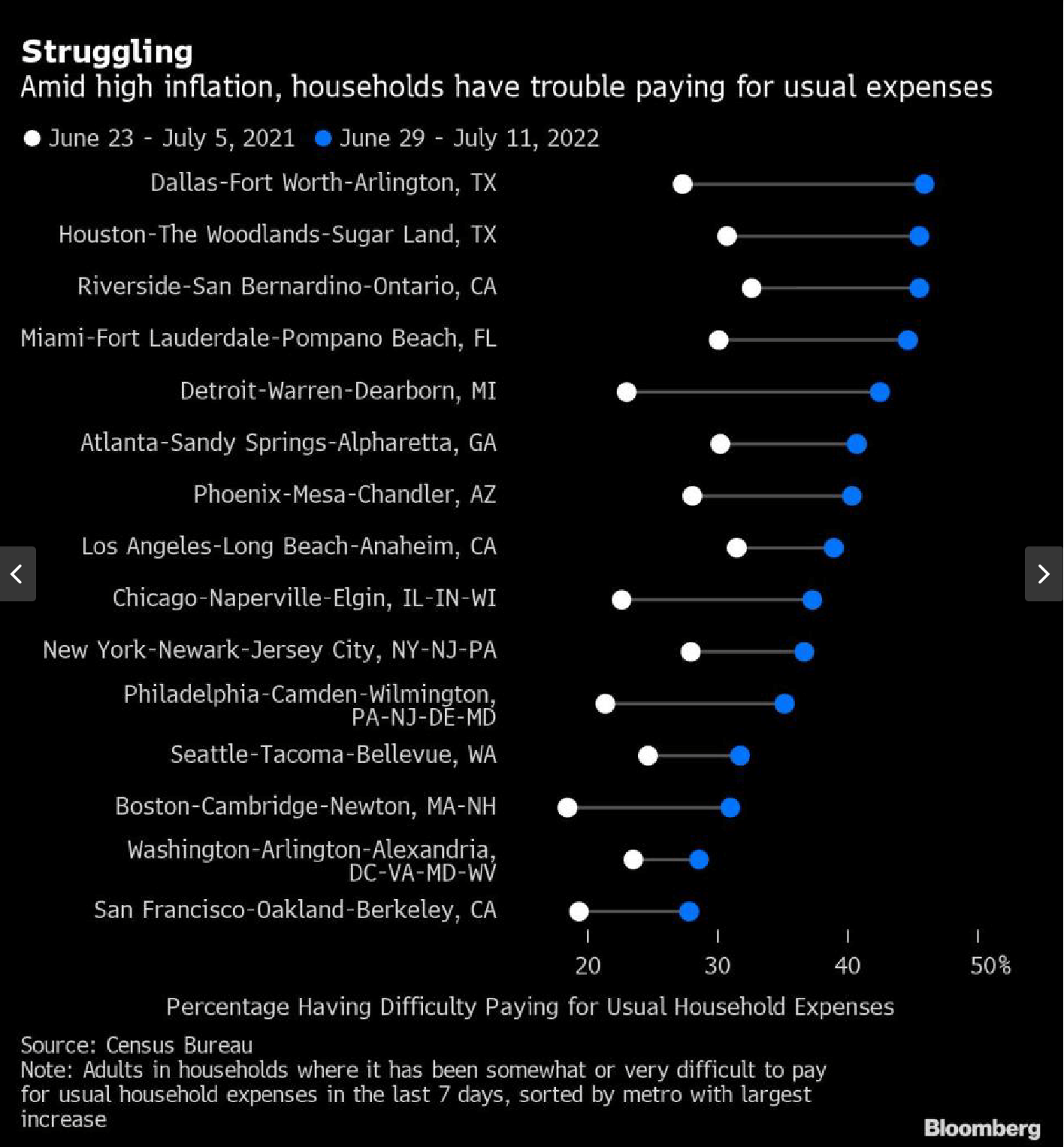

(Bloomberg) — The share of Americans who report having difficulties paying their bills has surpassed its 2020 pandemic peak in a US Census Bureau survey, underscoring the toll of soaring prices on budgets.

(Bloomberg) — The share of Americans who report having difficulties paying their bills has surpassed its 2020 pandemic peak in a US Census Bureau survey, underscoring the toll of soaring prices on budgets.

Four in ten adults said it has been somewhat or very difficult to cover usual household expenses in a poll conducted end of June and early July. That’s the highest since the Census started asking the question in August 2020. It implies that more than 90 million families are struggling, up from about 60 million a year ago.

When the Census first asked the question two years ago, a third of respondents reported difficulties in covering usual household bills. The share fell over the following year but started rising about a year ago after government pandemic relief ended and inflation took hold.

Millions of households with student loans are expected to face an additional monthly expense Sept. 1, when a Covid moratorium on servicing that debt ends.

The survey shows a sharp increase in financial stress in all of the country’s large metropolitan areas. In Dallas, for example, the share of respondents having difficulty paying bills jumped to about to 45.9% from 27.9% a year earlier. The share in Detroit rose by almost 20 percentage points.

A report last week from New York State Comptroller Thomas P. DiNapoli showed that one in eight residents were behind on paying their utility bills as of March. More than 1.2 million customers statewide owed $1.8 billion, with residents of New York City and Long Island accounting for 68% of the total.

The average amount owed by residents in the state doubled in two years, to $1,467 in March from $768 in March 2020.

“The pandemic’s effects continue to be felt in multiple aspects of life, including the elevated number of New Yorkers who continue to have trouble paying their utility bills,” DiNapoli said in the report.

Nationally, the latest Census survey shows that more than one third of households reduced or forwent expenses for basic household necessities, such as medicine or food, in order to pay an energy bill. More than one in five families kept their home at a temperature that felt unsafe or unhealthy for at least one month, and a similar share hasn’t been able to pay at least part of an energy bill.

Courtesy of Alex Tanzi, Yahoo Finance

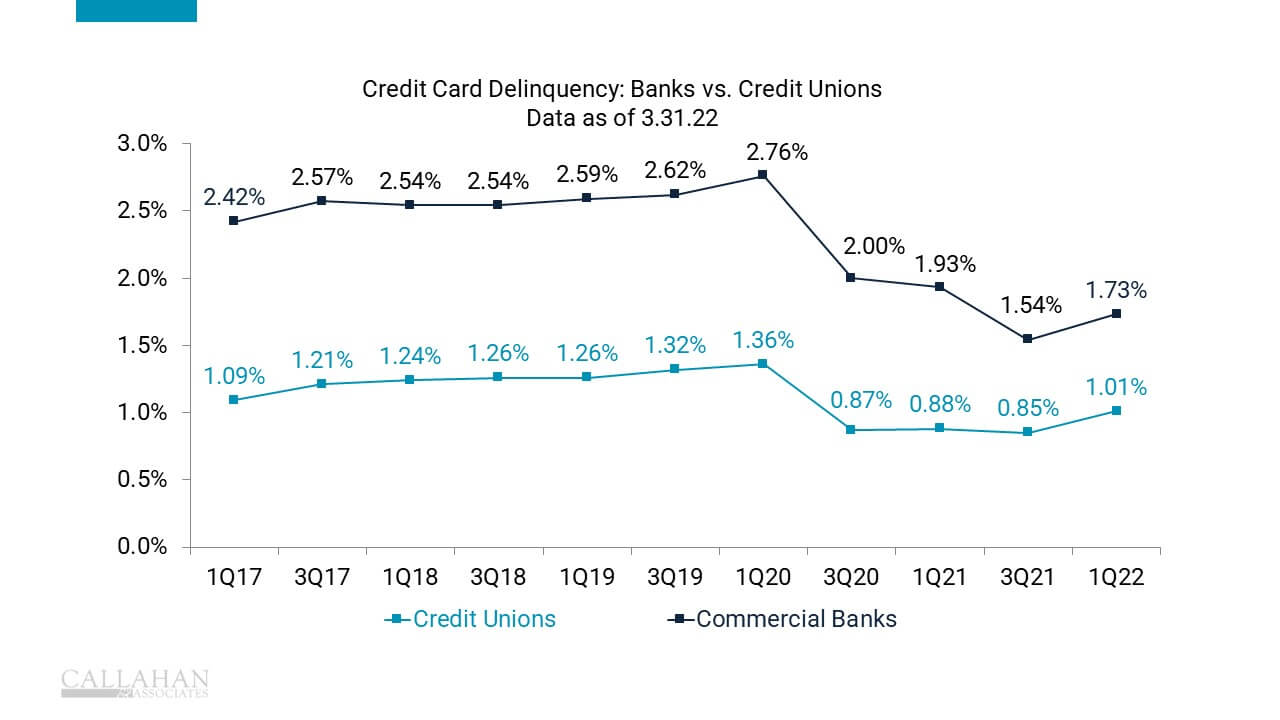

After a decline in consumer spending during the pandemic, the end of government relief programs has contributed to an increase in credit card usage – and a rise in delinquencies.

CREDIT CARD SPENDING, DELINQUENCIES RETURNING TO NORMAL FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.22

© CALLAHAN & ASSOCIATES| CREDITUNIONS.COM

- Credit card delinquencies at credit unions and commercial banks are back on the rise after unexpectedly improving during the pandemic, thanks to expanded unemployment benefits and stimulus checks from the federal government.

- At just 1.01%, credit card delinquency rates at credit unions at the end of the first quarter were nearly three quarters of a point below their for-profit counterparts, though for now credit unions are closer to reaching pre-pandemic delinquency levels than banks.

- Delinquency rates at banks and credit unions alike have been on the rise for the last four quarters following the end of government-backed pandemic-relief programs.

- The increase in delinquencies is largely a good thing. Credit card spending among credit union members fell $5.8 billion during the first year of the pandemic as lockdowns and social distancing led to a decline in consumer spending.

Courtesy of Sophie Monroe, CreditUnions.com

Cryptocurrency insider-trading case could have broad ramifications for industry.

Cryptocurrency insider-trading case could have broad ramifications for industry.

Federal authorities brought the first-ever cryptocurrency insider-trading case Thursday, accusing a former Coinbase Global Inc. COIN 5.43%▲ manager of tipping off his brother and a friend with confidential information, and signaling in a companion case an aggressive new push to police digital tokens.

Prosecutors in Manhattan filed wire-fraud charges against the three men, and, at the same time, the Securities and Exchange Commission brought a civil case against them in which it alleged that nine cryptocurrencies, including seven that are currently available on Coinbase, are unregistered securities.

The SEC’s classification of the digital tokens as unregistered securities could have wide-ranging effects on the cryptocurrency industry and expose Coinbase and other platforms to new legal liabilities and regulatory requirements.

An indictment unsealed in federal court in Manhattan alleged that Ishan Wahi, a former product manager at Coinbase, his brother Nikhil Wahi and his friend Sameer Ramani netted about $1.5 million in illegal profits.

The Wahi brothers were arrested Thursday morning in Seattle. Mr. Ramani remained at large, prosecutors said.

“Our message with these charges is clear: fraud is fraud is fraud, whether it occurs on the blockchain or on Wall Street,” said Damian Williams, the U.S. attorney for the Southern District of New York.

Lawyers for Ishan Wahi said the charges were meritless. “Ishan Wahi is innocent of all wrongdoing and intends to defend himself vigorously against these charges and in the SEC action,” said lawyers Andrew St. Laurent and Marc Axelbaum.

Priya Chaudhry, a lawyer for Nikhil Wahi, said prosecutors were trying to criminalize innocent behavior “because they are looking for a scapegoat because so many people have lost money in cryptocurrency recently.”

A lawyer for Mr. Ramani couldn’t be identified.

Coinbase said in a statement on its blog that it had conducted an investigation on the three men and had provided information about the individuals to the Justice Department. The platform also said it fired Ishan Wahi.

“Coinbase takes this type of illicit behavior super seriously,” said Paul Grewal, the company’s chief legal officer. “We have zero tolerance for it.”

Mr. Grewal said Coinbase invests heavily in systems and policies to prevent employees from taking advantage of confidential information, such as asset-listing plans.

Ishan Wahi, who worked on Coinbase’s asset-listing team, had advance knowledge of the timing and public announcements of assets the exchange planned to list, prosecutors alleged. He was one of a small number of employees who belonged to a private messaging channel used to discuss launch dates and timelines, according to the indictment.

Starting in June 2021, the three defendants used the confidential information to make trades in advance of at least 14 public-listing announcements by Coinbase, the indictment alleged. The men concealed the trades through a web of crypto accounts and anonymous digital wallets, prosecutors alleged.

Some of the trades drew public scrutiny. In April, a Twitter account well known in the crypto community flagged the purchase of hundreds of thousands of tokens about 24 hours before they were named in a public-listing announcement, prosecutors alleged. Later in the month, Coinbase said it was investigating whether someone inside the company had leaked confidential company information.

On May 11, the exchange’s security-operations director emailed Ishan Wahi, telling him to attend an in-person meeting, prosecutors said. The day before the meeting, Mr. Wahi bought a one-way flight to India scheduled to depart the next day, according to prosecutors. They said that before the flight departed, Mr. Wahi called and texted his brother and Mr. Ramani about Coinbase’s investigation.

Law-enforcement agents stopped Mr. Wahi and prevented him from leaving the country, according to prosecutors.

The case is the latest signal that federal prosecutors in Manhattan are making an enforcement push on alleged insider-trading schemes of digital assets. Prosecutors last month charged a former employee of an NFT marketplace with using inside information to profit on NFTs, or nonfungible tokens.

The SEC charges are likely to turn up the pressure on Coinbase, which had previously disclosed it was under investigation by the agency. SEC Chair Gary Gensler has said he plans to pursue enforcement actions against crypto-trading platforms that facilitate trading in unregistered securities.

Thursday’s civil complaint marked the first time the SEC under Mr. Gensler has formally identified cryptocurrencies it believes to be securities that are offered on a major trading platform. It raises the possibility that Coinbase could face penalties for violating federal laws that require securities exchanges to register with the SEC.

Coinbase disputed the SEC’s assessment and criticized the agency’s decision to get involved in the case.

Mr. Grewal, Coinbase’s chief legal officer, said the firm has no plans to remove the cryptocurrencies from its trading platform.

“We have reviewed these assets carefully in advance of our listing,” he said, though he declined to share the firm’s legal analysis.

For each of the cryptocurrencies it alleged to be securities, the SEC applied a legal test developed by the Supreme Court in the 1940s. The commission said the tokens were all offered and sold to investors by issuers hoping to raise money. The issuers and promoters of the offerings touted the potential profits that investors might earn from the assets based on the efforts of others, the SEC said in its complaint.

“Those realities affirm that a number of the crypto assets at issue were securities, and, as alleged, the defendants engaged in typical insider trading,” SEC enforcement chief Gurbir Grewal said.

Courtesy of Corinne Ramey, James Fanelli, and Paul Kiernan, Wall Street Journal

Budget Briefing

Budget Briefing

The NCUA board was briefed on the budget and current operating budget surplus. The surplus is primarily from lower staffing levels and vacancy rates resulting in decreased pay and benefits and continued travel reduction. The board anticipates this to shift as they fill vacant positions and travel ramps up into 2023.

There was also discussion surrounding transparency over the 2023 budget to ensure an opportunity for the industry to ask questions etc. The anticipated release to the public of the 2023 proposed budget is expected to be the end of September.

Vice Chair Hauptman also inquired if there would be a reduction in the operating fee imposed to credit unions due to the surplus.

Final Rule Parts 700,701,702,708a, 708b, 750 and 790 – Asset Threshold for Determination the Appropriate Supervisory Office – (Final ONES Rule)

As expected, at the NCUA Board meeting today, the board members unanimously passed a final rule regarding ONES supervision. Vice Chair Hauptman expressed his concerns that the rule doesn’t go far enough in terms of regulatory relief and pushed the board to identify means of regulatory relief for well-run institutions in a future discussion. Board Member Hood agreed and stated this isn’t the end of this rule, and it’s likely to see further iterations down the road as they continue to evaluate the industry as it evolves.

- No substantive changes to the final rule from the proposed rule.

Proposed Rule Part 748 – Cyber Incident Notification Requirements

Also, as expected, the board unanimously approved a proposed rule under Part 748 addressing cyber incident notification requirements, similar to those of the federal banking regulators. The timing for notification would be 72 hours from the date a FICU determines an incident has occurred.

From the NCUA: NCUA Board Issues Proposed Rule on Cyber Incident Reporting Requirements

The proposed rule and request for comment will have a 60-day comment window upon publication in the Federal Register. The NCUA has stated that to be reported, an incident must be considered “substantial.” The definition of what is considered “substantial” will be included in the request for public comment. It was discussed at the meeting that 3 incident types would be deemed substantial and reportable incidents:

- Federally Insured Credit Union identifies substantial loss of confidentiality/sensitive data as a result of unauthorized access/disruption of member services or integrity of a network or changed

- cyber-attack or exploitation of a vulnerability that disrupts business operations/member services

- Third-party service provider informs credit union data compromised by the third party – or upon a CU forming reasonable belief of compromise by a third party (whichever comes first)

Vice Chair Hauptman requested that if/when the rule is finalized, the NCUA must send out something directly to the industry – not just on the website – outlining examples of when to report and incidents that would not require reporting

![]() Bank of America (BAC.N) has set aside around $200 million for a regulatory matter connected to the unauthorized use of personal phones, its chief financial officer Alastair Borthwick said on Monday, adding that he expects the matter to be settled soon.

Bank of America (BAC.N) has set aside around $200 million for a regulatory matter connected to the unauthorized use of personal phones, its chief financial officer Alastair Borthwick said on Monday, adding that he expects the matter to be settled soon.

Last year, Reuters reported that the U.S. Securities and Exchange Commission (SEC) was looking into whether Wall Street banks have been adequately documenting employees’ work-related communications, such as text messages and emails, during the work-from-home period of the pandemic. read more

The remainder, roughly $200 million, is earmarked for other probes into how the bank kept track of employee communications on their personal devices, like cell phones, Borthwick said.

“The balance of the expense relates to an industry-wide issue and it concerns the use of unapproved personal devices,” he said on a call with reporters. “We hope to finalize that in the coming weeks,” he said.

During its second-quarter earnings on Monday, Bank of America recorded $425 million in expenses to address regulatory matters, $225 million of which related to federal regulatory fines issued last week over the bank’s handling of pandemic jobless benefits, Borthwick said. read more

In December, the SEC and the Commodity Futures Trading Commission fined J.P. Morgan Securities $200 million for “widespread” failures to preserve staff communications on personal mobile devices, messaging apps and emails. read more

Other major investment banks including Morgan Stanley (MS.N) and Citigroup (C.N) have also put aside cash to cover similar expected fines, the banks have said.

Regulators require banks to keep records of all business-related communications and as a result financial firms typically ban the use of personal email, texts and other social media channels for work purposes, although bankers do not always comply with those rules.

The SEC’s head of enforcement has said banks’ failure to fully record all staff communications has hampered its probes into other, unrelated issues.

Courtesy of Elizabeth Dilts Marshall, Reuters

![]() The gains in the amount spent far outpace gains in the number of transactions.

The gains in the amount spent far outpace gains in the number of transactions.

PSCU reported Tuesday that the value of purchases it handles for affiliated credit unions rose much faster than the number of transactions in June, which it said indicated inflation was a growing factor in purchasing growth.

The St. Petersburg, Fla., payments CUSO found members whose credit unions use PSCU services spent 16% more by credit cards in value and 12% more in the number of transactions in June than they did in June 2021. By debit, they spent 7% more by value and 3% more by number.

“While overall consumer spending remained strong throughout June, current inflationary pressures are keeping growth in purchases outpacing growth in transactions,” Brian Scott, PSCU’s chief growth officer, said.

The U.S. Bureau of Labor Statistics reported July 13 that inflation rose a seasonally adjusted 1.3% from May to June, and rose 9.1% from June 2021 to June 2022 — the largest 12-month gain since November 1981.

“With another record Consumer Price Index increase announced this month, the Federal Reserve is under continued significant pressure to tame soaring inflation,” Scott said.

Overall spending by credit union members served through PSCU seemed to trend higher that retail spending among all U.S. consumers.

The U.S. Census Bureau reported July 15 that retail spending — excluding automobiles, auto parts and gasoline — rose 7% from June 2021 to June 2022. The seasonally adjusted increase from May to June was 0.7%.

In particular categories, the 12-month gains reported by PSCU bracketed those reported by Census:

- Grocery spending rose 8.9% from June 2021 to June 2022, according to the Census Bureau. PSCU reported a purchase gain of 15% by credit and 5% by debit. Transactions rose 11% by credit and 2% by debit.

- Gasoline spending rose 49.9%, according to the Census Bureau. PSCU reported purchase gains of 59% by credit and 35% by debit. Transactions rose 15% by credit and 5% by debit.

- Restaurant spending rose 13.7%, according to the Census Bureau. PSCU reported purchase gains of 20% by credit and 6% by debit. Transactions rose 16% by credit and 2% by debit.

PSCU’s July Payments Index found the average credit card balance for June 2022 was $2,733, up 3.5% or $93 from June 2021. June marked the fourth consecutive month in which year-over-year growth was over 2%.

PSCU’s numbers reflected the national pattern for both credit unions and banks. Credit card balances dwindled after COVID-19 was declared a pandemic in March 2020, and had remained below the February 2020 mark for more than two years.

However, balances have been rising this year. The Fed’s G-19 Consumer Credit Report released July 8 showed May balances at both banks and credit unions had finally exceeded their February 2020 levels. NAFCU Chief Economist Curt Long said then that high inflation is one reason he expects credit card balances to grow quickly through the rest of the year.

The credit card delinquency rate for June was 1.54%, 20 basis points lower than pre-pandemic June 2019 levels.

PSCU’s report was based on data from credit unions that have been processing payments with PSCU since January 2020. It encompassed 2.8 billion transactions valued at $140 billion of credit and debit card activity in the 12 months ending June 30.

Courtesy of Jim DuPlessis, Credit Union Times

As a benefit for all NASCUS members, this digital platform provides a searchable data catalog of state credit union regulatory agencies (structure, funding, examination programs) and key state credit union powers including: chartering, enforcement authority, field of membership, interstate operations, parity, investment powers, board governance, CUSO powers, supplemental capital, derivatives authority, privacy, usury, tax treatment and more.

As a benefit for all NASCUS members, this digital platform provides a searchable data catalog of state credit union regulatory agencies (structure, funding, examination programs) and key state credit union powers including: chartering, enforcement authority, field of membership, interstate operations, parity, investment powers, board governance, CUSO powers, supplemental capital, derivatives authority, privacy, usury, tax treatment and more.

Project-launch data points are based on the previous 2016 Profile model and are continuously being updated in real-time by our 45 Supervisory partners.

NASCUS members can access data by clicking on the “Database Search” by clicking on the button below. (Login required)

Select the dropdown preferences based on the section topic and the state(s) of interest, then press “search.” Once the results pop up, use the “export” or “print” features on the right side to save your search findings.

Regulators updating information can access their state-specific portal by clicking here.

The National Association of State Credit Union Supervisors (NASCUS) invites you to join us at an exclusive event that brings state regulators, credit union leaders, and industry stakeholders together in a three-day, collaborative networking environment.

The National Association of State Credit Union Supervisors (NASCUS) invites you to join us at an exclusive event that brings state regulators, credit union leaders, and industry stakeholders together in a three-day, collaborative networking environment.

NASCUS’s annual State System Summit (S3), combines thought-provoking educational sessions and networking opportunities for attendees to renew and expand professional connections.

Agenda Topics

This year’s summit will offer a deep dive into the evolution, challenges, and opportunities of digital assets in the marketplace, the continuing rise of fintech, the future of credit union powers, and balancing regulation.

We will strategize on the myriad of challenges that lie ahead, including

- Worldwide Geopolitical Instability

- Lingering Pandemic Dislocation

- Looming Inflation

- Increasingly Sophisticated Cyber-Attacks, and

- Burgeoning Compliance and Supervisory Obligations

Location

The Waterfront Beach Resort

21100 Pacific Coast Highway, Huntington Beach, CA 92648

The National Association of State Credit Union Supervisors (NASCUS) created the Pierre Jay Award to recognize individuals, programs, and/or organizations whose contributions have benefited the state credit union system in a significant way. This award honors those who have demonstrated outstanding service, leadership, and commitment to NASCUS and the state system. This distinction is NASCUS’s highest honor in recognizing champions of the state credit union system.

The National Association of State Credit Union Supervisors (NASCUS) created the Pierre Jay Award to recognize individuals, programs, and/or organizations whose contributions have benefited the state credit union system in a significant way. This award honors those who have demonstrated outstanding service, leadership, and commitment to NASCUS and the state system. This distinction is NASCUS’s highest honor in recognizing champions of the state credit union system.

Eligibility, Criteria, and Nomination Process

Any person, program, or organization whose contributions have significantly benefitted the state credit union system.

- Proven contributions that have benefited the state credit union system significantly

- Proven demonstration of service, leadership, and commitment to the state system and/or NASCUS

Candidates may be nominated for a singular achievement or for activities spanning the course of their careers.

Complete & Submit A Nomination Form Here or visit NASCUS.org for more information.

Nomination Closing Date: July 24, 2022

For more information or questions, please contact NASCUS President/CEO Brian Knight.

—

About the Award

First presented in 1997, the Pierre Jay Award is named for the first Commissioner of Banks in Massachusetts, Pierre Jay. He learned of the cooperative credit union movement in Milan, Italy, and quickly embraced the concept. Working with philanthropist and credit union pioneer Edward Filene of Boston, Jay championed credit union development in the United States.

NASCUS members may submit nominations for the Pierre Jay for individuals and organizations that have demonstrated extraordinary commitment and dedication to the credit union system and/or to NASCUS.

NASCUS’ Pierre Jay Award Committee reviews nominations and a winner(s) are announced during NASCUS’s annual State System Summit (S3).

View List Of Previous Winners Here

November 16, 2021

Your credit union’s board members, committee members, and team members should not miss the NASCUS Michigan Industry Day!

With the Department of Insurance and Financial Services, we invite you to participate in an industry networking event. Take advantage of this excellent training opportunity for credit unions.

With the Department of Insurance and Financial Services, we invite you to participate in an industry networking event. Take advantage of this excellent training opportunity for credit unions.

Location:

Firekeepers Casino Hotel

11177 Michigan Avenue

Battle Creek, Michigan 49014

- Cost to attend: $199 Members and $299 Non-Members

- Questions: Click here to contact Isaida Woo, Ed.D, Vice President, Education

Agenda November 16

8:30 am – 9:00 am Breakfast

9:00 am – 9:15 am Opening Remarks

Speakers: Anita Fox, Director, Michigan Department of Insurance and Financial Services

Denice Schultheiss, Director, Michigan Office of Credit Unions, Michigan Department of Insurance and Financial Services

Brian Knight, President and CEO, NASCUS

9:30 am-10:45 am Compliance Update

Speaker: Glory LeDu, CEO, League InfoSight

10:45 am-11:00 am Break

11:00 am-12:00 pm Economic Development

12:00 pm-1:00 pm Lunch

1:00 pm-2:00 pm National Issues

Speaker: Brian Knight, President and CEO, NASCUS

2:00 pm-2:15 pm Break

2:15 pm-3:00 pm Troubled Commercial Real Estate (CRE)

3:00 pm-3:30 pm Closing Remarks

Speakers: Anita Fox, Director, Michigan Department of Insurance and Financial Services

Denice Schultheiss, Director, Michigan Office of Credit Unions, Michigan Department of Insurance and Financial Services

sCourtesy of Colby Smith, Financial Times

Minutes from June meeting suggest even tighter monetary policy may be needed from US central bank.

Top Federal Reserve officials think entrenched inflation is a “significant risk” to the US economy and fear tighter monetary policy will be needed if price growth exceeds their expectations, according to an account of their most recent meeting. The minutes of the US central bank’s June meeting, when the Fed delivered the first 0.75 percentage point rate rise since 1994, also showed that policymakers now support raising interest rates to the point at which economic activity is restrained, with the possibility that they could become “even more restrictive” if warranted by the data.

Top Federal Reserve officials think entrenched inflation is a “significant risk” to the US economy and fear tighter monetary policy will be needed if price growth exceeds their expectations, according to an account of their most recent meeting. The minutes of the US central bank’s June meeting, when the Fed delivered the first 0.75 percentage point rate rise since 1994, also showed that policymakers now support raising interest rates to the point at which economic activity is restrained, with the possibility that they could become “even more restrictive” if warranted by the data.

“Many participants judged that a significant risk now facing the committee was that elevated inflation could become entrenched if the public began to question the resolve of the committee to adjust the stance of policy as warranted,” the minutes said.

The notes from the Federal Open Market Committee, which were released on Wednesday, revealed the alarm spreading through the top ranks of the US central bank over inflation, which is running at an annual pace of 8.6 percent. The account also showed the lengths officials were willing to go to ensure prices do not spiral also showed the lengths officials were willing to go to ensure prices do not spiral further out of control.

The Fed will decide whether to raise rates by 0.50 percentage points or 0.75 percentage points at its meeting this month, although several officials have indicated their support for the larger increase.

“If inflation becomes entrenched in consumer and business psyches, it will be much more difficult to lower it over the medium term,” said Kathy Bostjancic, chief US economist at Oxford Economics. “That is the breaking point for [the Fed], and they really want to do their best to ensure that it doesn’t happen.”

She added: “The longer inflation remains high, the more it will become embedded in expectations.”The minutes showed that participants were increasingly aware that their plans to tighten monetary policy would slow the pace of economic growth. Most noted that the risks to the outlook were “skewed to the downside” given the possibility that further tightening could weigh on activity.

The minutes echoed recent comments from Fed chair Jay Powell, who has emphasized that the central bank has little room for maneuver as it tries to tame inflation without causing widespread job losses.

A US recession is now “certainly a possibility”, and would in large part depend on factors outside of the Fed’s control, he said last month, pointing to the war in Ukraine and prolonged Covid-19 lockdowns in China.

Powell reiterated that message last week on a panel with other central bankers, when he warned that a failure to restore price stability would lead to an even worse outcome for the US economy.

Click here to read the entire article.