(Dec. 4, 2020) A new member will be sitting at the next meeting of the NCUA Board when it gathers in about two weeks, thanks to action taken by the Senate this week.

Kyle Hauptman

Kyle S. Hauptman was confirmed by the Senate Wednesday on a bipartisan vote of 56-39, clearing the way for his swearing in and subsequent participation in a vote slated Dec. 17 on the agency’s 2021-2022 budget.

Nominated June 18 to the NCUA Board by President Donald Trump, Hauptman has most recently served as a staff director for the economic policy subcommittee of the Senate Banking Committee and as an economic policy advisor to Sen. Tom Cotton (R-Ark.). He worked on the 2016 Trump presidential transition team and served as a policy advisor on financial services for 2012 Republican presidential nominee Mitt Romney (now a U.S. senator representing Utah).

Confirmed to a term that continues into August 2025, Hauptman will take the seat recently vacated by J. Mark McWatters, whose term on the board expired in August 2019. McWatters had been serving in holdover capacity until his resignation Nov. 20.

That resignation followed by one day McWatters’ noting during an open board meeting that he would not approve of the agency’s proposed budget without certain changes.

NASCUS President and CEO Lucy Ito congratulated Hauptman on behalf of the state credit union system. “We look forward to working with him over the coming years,” Ito said. “There are a number of key issues of importance to state credit unions, including maintaining an equitable overhead transfer rate from the NCUSIF, continued consideration of subordinated debt for use by all federally insured credit unions, and on-going dialogue and collaboration between state and federal regulators. We are eager to meet with the newest NCUA Board member to discuss these and other issues as together we work toward a strong, and safe, credit union system.”

Hauptman’s confirmation fills out the membership of the agency’s board, as he joins Chairman Rodney Hood and Member Todd Harper. Both Hood and Hauptman are Republican appointees; Harper is a Democrat appointee. Hauptman becomes the third member to join the board in less than two years: both Hood and Harper joined the board in the spring of 2019 (although Hood is serving a second stint on the panel, having served on the board from 2005-09).

During a board briefing Wednesday, both Hood and Harper publicly congratulated Hauptman on his confirmation. Harper, further, noted that all three board members’ names now begin with the letter “H,” replacing the “Ms” on the board (when Chairman Debbie Matz, and Board Members Rick Metsger and J. Mark McWatters all served on the board together).

Interestingly, the last time all three board members’ last names began with the same letter (the “Ms”), all three, eventually, served as board chairmen. Harper could be in line to become the next board chairman (as a Democratic appointee) after Joe Biden is inaugurated as president Jan. 20.

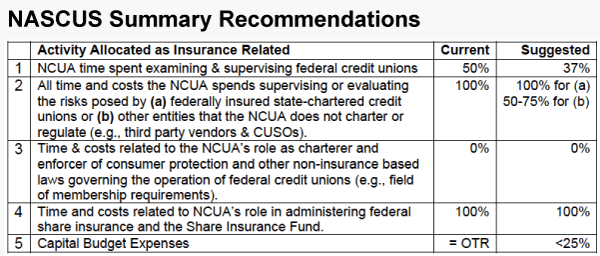

Dec. 4, 2020) NCUA should reconsider how it allocates expenses to the federal insurance fund for credit unions to pay for agency operations, in order to safeguard balance, equity – and ensure that more funds are available to cover any losses that may occur due to the financial impact of the coronavirus crisis, NASCUS told the agency this week.

In a presentation before the NCUA Board, NASCUS’ Lucy Ito made two key recommendations for expense allocations made by NCUA to cover its “insurance related costs” paid for by the National Credit Union Share Insurance Fund (NCUSIF) through transfers to the agency’s operating budget. The transfers are made via the overhead transfer rate (OTR), which NCUA is proposing be 1 percentage point higher in 2021 from this year, or 62.3%. The OTR represents the rate at which NCUA transfers money from the insurance fund to its operating budget to cover insurance-related costs.

The two key recommendations Ito made were: reduce the amount of the funds transferred to cover costs for examining federal credit unions (FCUs) from 50% to 37% of those costs, and reduce the amount of funds transferred to cover costs of evaluating risks of entities that NCUA does not charter or regulate (such as third-party vendors and CUSOs) from 100% to a range of between 50% and 75%.

Ito, providing the state system’s view of the agency budget, focused in her remarks exclusively on the OTR and costs that are allocated to it by the agency. She was one of three to make presentations to the NCUA Board members attending the meeting, Chairman Rodney Hood and Member Todd Harper. The others making presentations represented the Credit Union Natl. Assn. (CUNA) and Natl. Assn. of Federally Insured Credit Unions (NAFCU).

In recommending changes to the expense allocations, Ito said every dollar the agency transfers from the fund to cover expenses of the agency in “insurance-related costs” is a dollar that is not available to pay for credit union losses that are likely to arise as a result of the financial impact of the pandemic.

“The 1% increase in the OTR for 2021 means there will be $3.3 million less to cover losses by the fund,” Ito said.

In other comments, Ito recommended the agency reconsider how it allocates expenses paid by the fund for capital budget costs of its operations. For example, Ito said, given increasing state agency assumption of computer and other capital costs, “it would seem that the insurance fund would carry a much smaller percentage of NCUA’s computer software and other capital charges than the agency allocates to its role as the FCU chartering authority.”

She also suggested that the agency work with state supervisory authorities to validate their time allocation assumptions that make up portions of the OTR calculations. “We noted in last year’s budget briefing we would very much welcome the opportunity to sit with NCUA and understand out how NCUA reconciles the budgetary OTR with actual time allocations,” she said, adding that the invitation remains open from the association.

LINK:

NASCUS presentation, NCUA 2021 budget briefing (Dec. 2, 2020)

(Dec. 4, 2020) NASCUS supports making some changes to recordkeeping and travel rule regulations under rules implementing the Bank Secrecy Act (BSA) to promote calibrating the value of anti-money laundering measures with operational, compliance and expense considerations of credit unions and other institutions, NASCUS wrote in a comment letter filed Nov. 27.

In a letter to the Federal Reserve Board, NASCUS responded to a joint request for comments from the Fed and the Financial Crimes Enforcement Network (FinCEN). When the comment request was issued Oct. 23, the two agencies said they were issuing the portion of the rule concerning recordkeeping jointly because of their shared authority; the portion on travel was issued singly by FinCEN as it has sole authority over that area.

Under current rules, financial institutions must collect, retain, and transmit certain information related to funds transfers and transmittals of funds greater than $3,000, the agencies stated. Under the proposal, the applicable threshold for international transactions would drop to $250; the threshold for domestic transactions would remain the same ($3,000).

NASCUS, in its letter, wrote that lowering the threshold for fund transmittals beginning or ending outside of the U.S. will come with a cost for credit unions and other financial institutions. “For some institutions, the increased data storage requirements of capturing and preserving required information could be a significant burden, particularly as credit unions manage the economic dislocation resulting from the ongoing pandemic,” NASCUS wrote.

The association stated that the agencies should also consider that while the lower threshold applies only to transactions beginning or ending outside of the United States, for many institutions the best practice is to set data collection policies to the “lowest requirement” to ensure consistent compliance. The agencies’s proposal, NASCUS wrote, “would result in the capture and retention of significant amounts of data even for those credit unions doing only infrequent international funds transmittals,” NASCUS wrote.

In other comments, NASCUS also:

- Wrote that it supports including a specific standard for “reason to know” in the rule to mitigate the potential for confusion and uncertainty as to the standard to be met. “We would also recommend clear guidance on the obligations of all financial institutions in the chain of a funds transmission with respect to identifying cross-border transactions and compliance with the final rules,” NASCUS wrote. Under the proposal, funds transfer or transmittal of funds would be considered to begin or end outside the U.S. if a financial institution knows or has reason to know that the transmittor, transmittor’s financial institution, recipient, or recipient’s financial institution is located in, is ordinarily resident in, or is organized under the laws of a jurisdiction other than the United States or a jurisdiction within the United States.

- Urged FinCEN to continue to evaluate the BSA framework to eliminate redundant monitoring, reporting or recordkeeping requirements. “Reducing compliance burden in ‘other’ areas of the BSA would allow credit unions to reallocate resources to those areas where enhanced diligence, or more granular reporting might be needed by law enforcement,” NASCUS wrote.

(Dec. 4, 2020) The CFPB’s proposal to develop a rule on consumer access to financial records has been summarized by NASCUS and is posted on the website; the summary – the latest in the association’s continuing series to shine a light on key regulatory developments – is available to members only.

In October, the bureau finally released its advance notice of proposed rulemaking (ANPR) on the issue of consumer access to financial records, following up on a promise it made in July, which in turn followed a symposium on the subject in February.

The bureau said in October that its ANPR is aimed at fulfilling its obligations under a provision of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank). The proposal’s summary states that the provision (Sec. 1033) provides that the agency will issue rules prescribing that a consumer financial services provider must make available to a consumer information in the control or possession of the provider concerning the consumer financial product or service that the consumer obtained from the provider.

The ANPR seeks comments and information, CFPB said, on costs and benefits of consumer data access, competitive incentives, standard-setting, access scope, consumer control and privacy and data security and accuracy.

In late February, the bureau sponsored a symposium on the law’s requirement for consumer records access rules. The event featured panels discussing benefit and risks of consumer-authorized data access, as well as developments in the area of records access. Then in July, the bureau gave a sort of “head’s up” that the ANPR was coming, saying that the call for information would help the agency understand and address “competing perspectives.”

Comments are due on the ANPR Feb. 4.

LINK:

NASCUS summary: CFPB’s ANPR on consumer access to financial records (members only)

(Dec. 4, 2020) Credit unions, banks and other entities questioning whether to comply with regulatory requirements can submit a request to the CFPB to clear up any uncertainty, the agency said under a new policy finalized this week.

NASCUS has already outlined the new policy in a summary (available to members only).

“Regulatory certainty promotes compliance if the law applies and avoids unnecessary compliance costs if the law does not,” the CFPB said of its new policy in a release.

In June, the bureau unveiled a pilot program to allow entities to submit a request for clarity on its regulations “where uncertainty exists.” The “pilot advisory opinion” program (referred to as “AO”) reviewed the submissions, selected topics based on the program’s priorities, and then made responses available to the public. The program was proposed as a procedural rule with a request for comment.

Monday’s release by the bureau made the program permanent. Under the final policy, the bureau said, any person or entity can submit a request for an advisory opinion via email (to [email protected]). The bureau said it would review the submissions received, prioritize certain requests for response, and issue opinions with a description of the incoming request.

The bureau said it may also decide to issue advisory opinions on its own initiative, and that (to increase transparency), it would publish all advisory opinions in the Federal Register and on its website.

LINKS:

NASCUS summary: Advisory opinions policy (members only)

(Dec. 4, 2020) Following the Senate’s action to fill out the membership of the NCUA Board, on Thursday the Senate filled one of two empty seats on the Federal Reserve Board, confirming Christopher Waller. But it wasn’t a cakewalk: by many accounts, it was one of the closest confirmation votes ever for a central bank board member.

Waller, now executive vice president/director of research for the Federal Reserve Bank of St. Louis (and a former professor of economics at the University of Notre Dame), was confirmed on a vote of 48-47, with all Democrats and Republican Sen. Rand Paul (Ky.) voting against.

Thursday’s vote marked the first time the Senate had confirmed a Fed governor in a lame-duck period that follows the November election before the president’s term ends in January. Further, Fed governors are more typically confirmed on much more lop-sided votes, with 60 votes or more in favor.

The close vote for Waller (considered a “non-controversial” nominee) may signal bad news for the future on the Fed Board for the nominee to the other open seat: Judy Shelton. She has received a cool reception in the Senate, particularly among Democrats, for her past comments about bringing back the gold standard, questioning the effectiveness of federal deposit insurance, and the Fed’s independence from political influence.

Last month, Shelton’s nomination came before the Senate and failed to earn enough votes to cut off debate – action that would have paved the way for a final vote on her nomination. The close vote on Waller likely indicates the controversial Shelton will have a tough time being considered again in the Senate. In fact, Senate Majority Whip John Thune (R-S.D.) said Thursday that another vote on Shelton’s nomination was “unlikely” at this point.

(Dec. 4, 2020) The Utah Department of Financial Institutions (DFI) is the latest state credit union regulator to earn accreditation from NASCUS, the association announced this week. The Utah DFI, which regulates 30 credit unions across the state, earned its accreditation for five years.

The accreditation is the result of a substantive process that includes disciplined self-evaluation, peer review and ongoing monitoring. The process is administered by the NASCUS Performance Standards Committee (PSC) and measures a state regulatory agency’s ability and resources to effectively carry out its regulatory and supervisory programs. A credit union state supervisory agency must demonstrate that it meets standards in agency administration and finance, personnel and training, examination, supervision and legislative powers to earn accreditation.

“Congratulations to the Utah DFI for achieving this distinction,” said NASCUS’ Lucy Ito. “Accreditation is credible evidence of an agency’s capabilities, which also benefits credit unions in the state by providing recognition of the professionalism of a state agency’s regulators, supervisors and staff – and illustrates how a state regulatory agency has met the highest levels of regulatory proficiency.”

More than 85% of state-chartered credit union assets are supervised by NASCUS’ accredited state agencies. The NASCUS Accreditation Program was adopted in 1989 to administer and assure the quality standards of states’ credit union examination and supervision. Modeled on the university accreditation concept, the program applies national standards of performance to a state’s credit union regulatory program.

LINK:

NASCUS Accreditation Program

(Dec. 4, 2020) John Ducrest, long-time (since 2004) Louisiana commissioner of financial institutions in the state’s Office of Financial Institutions (OFI), has retired, effective Dec. 2. Among many other contributions to NASCUS, Ducrest drove critical enhancements to NASCUS’ Accreditation Program and most recently served as Chairman of the NASCUS Performance Standards Committee. Christine Kirkland has been named acting commissioner of the OFI … Meanwhile, in Kansas, Vickie Hurt has assumed her duties (as of Nov. 28) of acting administrator of the Kansas credit union administrator; the state’s Senate is expected to take up her confirmation as permanent administrator in the 2021 legislative session. She is also a former credit union CEO and board member of the Kansas Credit Union Association. Hurt replaces Jerel Wright in the position, who retired Nov. 28 following 14 years of service (1997-2005 and 2014-20).

(Dec. 4, 2020) CU Campus 365 is an alliance between NASCUS and BAI, the industry leader in compliance training, with a history of more than 95 years in the financial services industry. The product is a new compliance and professional skills training benefit for NASCUS credit union members that offers credit unions affordable, efficient, and comprehensive solutions for compliance training and professional skills learning featuring the latest in courseware and the BAI Learning Manager, a learning management system (LMS) specifically designed to meet the demands of the financial services industry. With it, credit unions have the tools they need to minimize compliance risk and increase employee development. Click on the link below to learn more and to schedule your demo of the program.

LINK:

Welcome to CU Campus 365!

(Dec. 4, 2020) Nominations for the NASCUS 2020 Pierre Jay Award – which recognizes the individuals, programs or organizations whose contributions have benefited the state credit union system in a significant way – are due Dec. 31. The award honors those who have demonstrated outstanding service, leadership and commitment to NASCUS and the state system. The award will be conferred during a virtual event in the first quarter of 2021. NASCUS members may nominate any person, program, or organization who or that has made a significant contribution to the state credit union system is eligible to be nominated. Nominees do not necessarily need to be affiliated with NASCUS. Examples of individuals, programs or organizations to be nominated include credit union organizations, volunteers (including committee members), staff members, or chief staff executives; and, state/federal organizations, state/federal lawmakers, state/federal regulators, or others. See the link below to submit a nomination.

LINK:

Pierre Jay Award: Details, nomination form

(Dec. 4, 2020) NASCUS credit union members will receive their 2021 membership dues via email invoices next week, arriving from the address of [email protected]; subject line will be “NASCUS 2021 Membership Dues Invoice.” Those who do not receive their invoice by Friday, Dec. 11, should send an email to NASCUS at [email protected]. NASCUS recognizes the impact the global pandemic has had on credit unions, and in 2021 the effects likely will be felt the most. NASCUS reassessed its value proposition to credit unions and doubled down on the commitment to deliver affordable alternatives to professional development through new compliance training solutions and the development and delivery of exclusive resources in collaboration with state regulators, as well as the many other unique products and services NASCUS provides. We will continue to monitor and solicit member feedback to build on benefits that credit unions value the most.

(Dec. 4, 2020) Banks, “as soon as practicable,” should cease entering into new contracts that employ LIBOR as a reference rate in loan contracts, the three federal banking agencies said this week. LIBOR (London Interbank Offer Rate), which is being phased out because the transactions it is based on don’t occur as often as they did in prior years, is used by many banks (and credit unions) as a benchmark for such products as adjustable mortgage loans. The agencies’ recommendation is being made, they said, in order to facilitate an orderly – and safe and sound – transition to alternative reference rates. Meanwhile, the administrator of the soon-to-be-defunct LIBOR (Intercontinental Exchange (ICE)) also this week proposed a plan to cease publishing the U.S. dollars version of the rate at the end of next year.