(Dec. 23, 2020) A new title has been bestowed on the newest member of the three-member board for the NCUA, who is now “vice chairman,” according to a release from the agency late last week.

Kyle S. Hauptman, who was confirmed by the Senate to a seat on agency’s board Dec. 2 – and who joined his first two meetings of the board last week (on Dec. 17 and 18) – was, late in the day Friday, tapped as vice chairman of the panel. The title — while indeed an honor — is largely honorific: other than sitting in for the board chairman in that individual’s absence, and taking a role in some appeals for Freedom of Information Act (FOIA) request decisions (under part 792.28 of agency regulations), there are few specific duties, responsibilities or benefits attached to role, other than those assigned by NCUA Board Chairman Rodney Hood.

The new vice chairman, in a press statement, said that in his role he looks forward to “working with credit unions, my fellow Board Members, and Congress on solutions that provide regulatory relief for the credit union community and expand the use of technology to reach underserved communities.”

This week, Hauptman named veteran credit union service organization (CUSO) and state league executive Sarah Canepa Bang as his senior adviser. The agency, in a release Monday, said Bang has broad experience in the credit union industry that includes serving as executive vice president of industry relations and president and chief strategy officer at CO-OP Financial Services. Previously, she was (among other things) chief executive officer at Financial Service Centers Cooperative, Inc., and executive vice president of the Oregon Credit Union League and Affiliates.

In other agency personnel developments this week, NCUA officially announced the retirement of J. Owen Cole, associate director of the policy and markets division in the NCUA’s Office of Examination and Insurance at the end of this month. NCUA said Cole served in various roles during his 27-year tenure, including senior investment officer, director of the division of risk management, associate regional director of operations, deputy executive director, and acting chief of staff. Most recently he had also served as president of the NCUA Central Liquidity Facility, which addresses potential credit union system liquidity risks.

LINKS:

NCUA Board Designates Hauptman as Vice Chairman

Sarah Canepa Bang Appointed Senior Advisor to Vice Chairman Hauptman

Owen Cole, Associate Director for Policy and Markets, Announces Retirement

(Dec. 23, 2020) The Federal Reserve Board now has six (out of a total seven) members, as newest Gov. Christopher Waller joined the board after taking his oath of office last Friday. Waller was confirmed by the Senate Dec. 3; he is the former research director for the St. Louis Fed, and a former professor. Meanwhile, there is still no word on confirming the nominee to the seventh and final seat on the board. A vote on controversial nominee Judy Shelton has been stalled in the Senate since at least November; Senate leadership has yet to announce plans to take up the nomination again … Big banks saw their losses rise to more than $600 billion under conditions simulated in a second stress test conducted by the Federal Reserve – but the banks’ capital ratios, despite the losses, would continue to be well above the minimum required (falling from 12.2% to 9.6%, but still above the 4.5% minimum), the central bank said late last week. Nevertheless, the Fed plans to keep restrictions on the banks’ distributions to investors and share repurchases, and won’t make changes to capital requirements … How to spot warning signs of human trafficking is in the spotlight for a webinar next month sponsored by NCUA, set for Jan. 7. The agency said the event will provide an overview of human trafficking and its impact on communities, law enforcement’s efforts to combat it, and potential red flags in credit unions. Attendees will also learn how to report concerns about human trafficking to the proper authorities, the agency said. There is no charge for attending, although advance registration is required … This is the final issue of NASCUS Report for 2020; we’ll see you again on Jan. 8. In the meantime: Happy Holidays – and have a terrific New Year!

LINKS:

Federal Reserve Board releases second round of bank stress test results

Register Now for NCUA’s Human Trafficking Webinar on Jan. 7

(Dec. 18, 2020) Well-capitalized, federally insured credit unions could count subordinated debt as capital for risk-based net worth purposes under a new rule approved by the NCUA Board at its meeting Thursday.

The decision has been long sought by the state system, which would bring regulation of federally insured credit unions in line with regulations of some states that already allow their credit unions to issue secondary capital, including in the form of subordinated debt.

Thursday’s meeting was the first of two meetings for the board this week; it also meets today to consider its 2021 budget and the overhead transfer rate (OTR); see story below.

Key provisions of the final rule (137 pages long), approved unanimously by the board, include:

- Permission for low-income-designated credit unions (LICUs), complex credit unions, and new credit unions to issue subordinated debt for purposes of regulatory capital treatment.

- A maximum maturity of 20 years to be imposed on debt issued (with a minimum maturity of 5 years), and a minimum denomination of $100,000. The agency noted the maturity limit helps to clarify that the financial instruments issued are debt – and not equity in the credit unions (which are solely owned by the members; credit unions do not issue stock).

- Prohibitions on a credit union from being both an issuer and investor unless the credit union meets certain conditions related to mergers.

- A section addressing new rules and limits for making loans to other credit unions, including investing in subordinated debt at those credit unions.

The effective date for the final rule is Jan. 1, 2022 (which coincides with implementation of the new risk-based capital rule).

The final rule also grandfathers any secondary capital issued before the effective date of this final rule and preserves that capital’s Regulatory Capital treatment for 20 years after the effective date, the agency said. The “grandfathered secondary capital” generally, according to NCUA, remains subject to requirements in the agency’s current secondary capital rule.

The agency also noted a number of additions and amendments to other parts and sections of NCUA’s regulations through the new rule, including:

- Cohering changes to part 741 of NCUA rules to account for the other changes proposed in the final rule that apply to federally insured, state-chartered credit unions (FISCUs);

- A new section addressing limits on loans to other credit unions;

- An expansion of the borrowing rule to clarify that federal credit unions (FCUs) can borrow from any source;

- Revisions to the final RBC Rule and the payout priorities in an involuntary liquidation rule to account for subordinated debt and grandfathered secondary capital.

Several changes in the final from the proposal have also been made, the agency said, including:

- Amendment of the definition of “accredited Investor;”

- Provision of a longer timeframe in which to issue subordinated debt after approval;

- Reduction in the required number of years of pro forma financial statements an issuing credit union must provide with its application (from five years to two years);

- Clarification of the prohibition on subordinated debt issuances outside of the United States;

- Clarification that the NCUA Board will publish a fee schedule only if it makes a determination to charge a fee.

In announcing the unanimous vote on the new rule, NCUA Board Chairman Rodney Hood said he was pleased with the balance struck with the final rule. “I support giving complex credit unions the authority to prudently use subordinated debt as an additional tool to comply with risk-based capital requirements, and newly chartered credit unions the ability to use this tool to get up and running,” he said.

Last summer, in a comment letter on the proposal, NASCUS wrote that the development of the rule is an essential complement to the implementation of a risk-based capital rule. “Including Subordinated Debt in risk-based capital ratio calculations is consistent with the statutory purposes of both state and federal credit unions and is sound public policy,” NASCUS wrote. “This rule will help credit unions and their members, protect the share insurance fund, and help place natural person credit unions in the United States on par with credit unions and other depository institutions worldwide.”

Reaction from the banking industry to the board’s action was negative, as illustrated by comments from two of the industry’s largest advocacy groups. The American Bankers Association (ABA), in an op-ed published the day before the board acted, said it “firmly opposed” the final rule, claiming it will undermine the “statutory principle that credit unions should serve consumers of small means.” The Independent Community Bankers of America (ICBA) said in press statement Thursday that the rule will “allow outside investors to exploit the credit union tax subsidy.”

LINK:

Final rule: Subordinated debt (Parts 701, 702, 709, and 741)

(Dec. 18, 2020) NASCUS President and CEO Lucy Ito, in a press statement, praised the NCUA Board for finalizing the subordinated debt rule, noting the state system’s long support for such action.

“The state system has long said that subordinated debt should be a part of the risk-based capital framework because it encourages well-managed credit unions to attract additional loss-absorbing forms of capital that they would otherwise forego,” said NASCUS President and CEO Lucy Ito. “The risk-based capital rulemaking itself is intended to increase the capital buffer standing of a credit union before any effect on the share insurance fund, and subordinated debt is consistent with that goal.”

Ito also thanked the board for moving forward on the final rule, which has been in the works for at least four years. She said NASCUS and state regulators look forward to working closely with NCUA in preparing for the implementation of the subordinated debt rule, and related capital rules, given the state system’s familiarity and experience with this form of capital

LINK:

Press statement by Lucy Ito on subordinated debt adoption

(Dec. 18, 2020) With a rare second monthly meeting scheduled for today (Friday, Dec. 18), the full-complement NCUA Board will consider the 2021 budget for the agency, which includes an increase of 1 percentage point for the overhead transfer rate (OTR), the rate at which the agency transfers funds from the federal savings insurance fund to the operating budget of the agency to cover its “insurance-related costs.”

More coverage of the meeting, which ensues after NASCUS Report’s deadline, will be included in next week’s report.

The board is expected to approve the $342.5 million budget as proposed, although likely on a split vote. Board Member Todd Harper has voiced objection to the lack of funding for consumer protection compliance staff in the budget and has said he would not support the budget unless that funding was put into place. Board Chairman Rodney Hood has no such objections; newest Board Member Kyle Hauptman (a Republican appointee like Hood) is expected to follow Hood’s lead on the budget.

For its part, NASCUS has taken no position on the budget, except with respect to the increase in the OTR, which would be 62.3% in 2021 (up from 61.3% in 2020).

In testimony two weeks ago before the NCUA Board at its public briefing about the 2021 budget, NASCUS urged NCUA to consider making changes to how it allocates expenses through the OTR to insurance-related activities, in order to ensure balance, equity and that more funds are available to cover any losses that may occur due to the financial impact of the coronavirus crisis.

“The 1% increase in the OTR for 2021 means there will be $3.3 million less to cover losses by the fund,” NASCUS’s Lucy Ito told the board. She noted that NASCUS recognized its recommendations cannot be implemented for 2021, but that the state system hopes they would be considered for future budgets. “We want to work with NCUA,” she said.

Friday’s board session is scheduled to get underway at 10 a.m. ET, and is being live-streamed via the Internet.

LINK:

NCUA Board Agenda for the Dec. 18, 2020 meeting

(Dec. 18, 2020) In other action at Thursday’s meeting, the NCUA Board issued one final rule and three proposed regulations – with three of those approved on split votes after Board Member Todd Harper (the lone Democrat appointee on the board) voted in opposition all three times.

The board:

- Approved (unanimously), an extension to Dec. 31, 2021 for a temporary final rule that increases the maximum aggregate amount of loan participations that a federally insured credit union (FICU) may purchase from a single originating lender without seeking a waiver from NCUA to the greater of $5 million or 200% of the FICU’s net worth (up from the greater of $500 million or 100% of the FICU’s net worth). The rule had been slated to expire at year’s end. The temporary rule, adopted by the NCUA Board as a relief measure for credit unions in the midst of the coronavirus crisis last spring, took effect April 21.

- Issued a proposed rule (on a 2-1 vote) on field of membership shared facility requirements (under Part 701, Appendix B, of agency rules) that NCUA said is intended to modernize requirements related to service facilities for multiple common bond (MCB) federal credit unions (FCUs). NCUA said the proposal includes any shared branch, shared ATM, or shared electronic facility in the definition of “service facility” for an MCB FCU that participates in a shared branching network. “The FCU need not be an owner of the shared branch network for the shared branch or shared ATM to be a service facility,” the agency said. “These changes would apply to the definition of service facility both for additions of select groups to MCB FCUs and for expansions into underserved areas.” Harper said he questioned the proposal’s ability, without changes, to increase service to underserved areas. The proposal will have a 30-day comment period.

- Released a second proposed rule (on a 2-1 vote), this one on mortgage servicing rights (under Parts 703 and 721 of agency rules), which would amend the agency’s investment regulation to permit FCUs to purchase mortgage servicing rights from other federally insured credit unions subject to certain conditions. Harper called the proposal “half baked,” but said he could find a way to support a final rule if changes were made. The proposal will be issued with a 30-day comment period.

- Advanced yet a third proposed rule – this one on overdraft policy (under Part 701 of NCUA rules) – also on a 2-1 vote. The proposal would remove the requirement that an FCU’s written overdraft policy establish a 45-day time limit for a member to either deposit funds or obtain an approved loan from the FCU to cover each overdraft, and replace it with a requirement that the written policy must establish a specific time limit that is “both reasonable and applicable to all members for a member either to deposit funds or obtain an approved loan from the FCU to cover each overdraft.” In May, the board tabled a proposed interim final rule to let FCUs decide how long members have to resolve account overdrafts. The proposal was tabled after failing to win a second from one of two board members when Chairman Hood asked for it (both members Harper and McWatters expressed opposition to a final rule). Back in May, Harper said the rule would (among other things) allow credit unions to garnish members’ income – including any economic stimulus relief funds – to pay off overdraft debt. Harper reiterated his objections Thursday (“I couldn’t support it then, I can’t now,” he said). Comments are due 30 days after publication in the Federal Register.

The board also set the “normal operating level” for the National Credit Union Share Insurance Fund (NCUSIF) at 1.38 for the coming year, no change from 2020. The NOL represents the target level of reserves in the fund relative to shares insured (referred to as the equity level). Generally, it is the level of reserves the board believes is needed to deal with anticipated losses from credit unions (if any) throughout the year, without lowering the reserving rate below 1.20%, the point at which an insurance premium would be required.

Along those lines, staff told Board Member Harper that it estimates the equity level of the fund at year-end will be 1.32% — well above the level at which a premium would be required. Agreeing with staff that chances of a premium in 2021 now look “next to zero,” Harper said that would be “welcome news to many credit unions.”

LINKS:

Temporary Final Rule, Regulatory Relief in Response to COVID-19

Proposed rule, Field of Membership Shared Facility Requirements

Proposed Rule, Mortgage Servicing Rights

Proposed Rule, Part 701, Overdraft Policy.

Board Briefing, Share Insurance Fund 2021 Normal Operating Level

(Dec. 11, 2020) Following up on plans announced in the wake of reported ethics failings by former staffers, the NCUA this week announced the selection of Elizabeth J. Fischmann as its first chief ethics counsel, effective Dec. 21.

Fischmann, the agency said, will oversee the NCUA’s new Office of Ethics Counsel that will certify the agency’s compliance with relevant federal ethics laws and regulations, promote accountability and ethical conduct, and help ensure the success of the NCUA’s ethics programs, including programs designed to prevent harassment, discrimination, and misconduct in the workplace. She will report directly to the NCUA Board and will be supervised by the NCUA chairman.

Currently, Fischmann serves as the associate general counsel for ethics and designated agency ethics official for the U.S. Department of Health and Human Services, where she administers and supervises the HHS-wide ethics program. She has also served as an associate counsel at the U.S. Office of Government Ethics and Deputy Counsel for the U.S. Department of the Navy, the NCUA said. Fischmann earned a Juris Doctorate from Georgetown University Law Center and a Bachelor of Arts from the University of Virginia, according to NCUA; she’s a member of the District of Columbia and Maryland Bars.

NCUA announced plans earlier this year to establish the ethics counsel office in April, about six weeks after a report was made public by the NCUA Office of Inspector General (OIG) substantiated allegations by then-Deputy General Counsel Lara Daly-Sims that she and then-General Counsel Mike McKenna drank alcohol and went to strip clubs during work hours.

LINK:

Elizabeth Fischmann Named NCUA Chief Ethics Counsel

(Dec. 11, 2020) Following passage of the NASCUS DEI Public Policy in August , the NASCUS Regulatory Board and Credit Union Advisory Council voted unanimously to sign the Credit Union Diversity, Equity, and Inclusion Collective Pledge at its Joint Leadership meeting on Dec. 4. The CU DEI Collective believes diversity, equity, and inclusion are fundamental to good business and to a vibrant, relevant, and growing credit union movement. Signing the pledge reflects NASCUS’ long-standing commitment to DEI and newfound solidarity with the broader credit union movement. NASCUS remains committed to a diverse and inclusive workforce and leadership and we proudly join forces with the CU DEI Collective. See the links below for more … NASCUS is still taking applications for the position of Communications and Marketing Director; see the link below for the job’s details, including how to apply.

(Dec. 11, 2020) Two new summaries were posted this week by NASCUS, outlining an NCUA final rule on corporate credit unions and an interagency proposal about codifying the use of “supervisory guidance” from federal agencies. Both are available to members only.

Corporate final rule clarifies provisions

The final rule on corporate credit unions, generally aimed at clarifying a number of provisions in NCUA’s rules, was adopted unanimously by the NCUA Board in October. The rule takes effect next week (Dec. 14), and addresses five key areas:

- permits a corporate credit union to make a minimal investment in a credit union service organization (CUSO) without the service organization being subjected to heightened agency oversight;

- expands the categories of senior staff positions at member credit unions eligible to serve on a corporate credit union’s board;

- removes the “experience and independence” requirement for a corporate CU’s enterprise risk management (ERM) expert;

- clarifies the definition of a collateralized debt obligation;

- simplifies the requirement for net interest income modeling.

Although the proposal did contain two provisions regarding proposed subordinated debt offerings by credit unions, the final rule leaves those out. NCUA decided to remove both of those provisions, noting that both sections would be addressed in a final rule on subordinated debt in the future. The agency added that it does not envision any changes to the proposed definition of a debt instrument included in the proposal.

‘Supervisory guidance’ would be codified

In late October, NCUA joined the federal banking agencies and the CFPB in proposing a rule (for a comment period ending Jan. 4) aimed at clarifying and codifying the role of supervisory guidance from federal financial institution regulators. Under the proposal, the meaning of “supervisory guidance” would be clarified as meaning, essentially, it doesn’t have the force of law. If finalized, the proposal would codify an interagency statement issued by all of the agencies in September 2018. That statement was intended to make clear that, unlike a statute or regulation, supervisory guidance is not the same as statute or regulation. “Supervisory guidance does not have the force and effect of law, and the agencies do not take enforcement actions based on supervisory guidance,” the 2018 statement read.

NCUA has maintained that the proposal will not create a burden for credit unions – partially because, the agency said, NCUA has followed the intent of the proposal for at least the last seven years. NCUA has noted that, at least since 2013, all “documents of resolution” for credit unions have been to specific statutory and regulatory citations – a practice, the agency has vowed, would not change under the proposed rule.

LINKS:

Summary: corporate rule (members only)

Summary: role of supervisory guidance (members only)

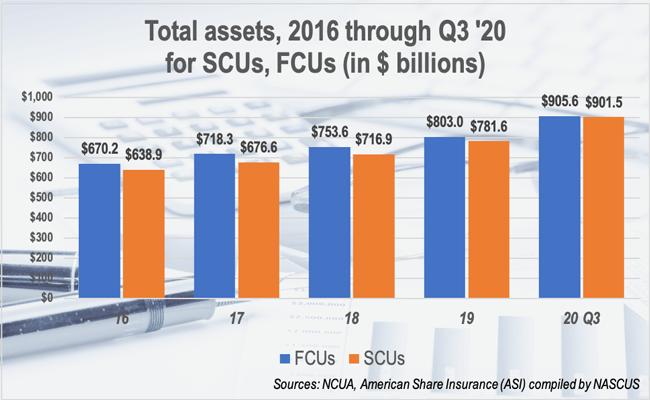

(Dec. 11, 2020) State credit unions maintained their hold of half of all credit union assets during the third quarter, according to the latest quarterly financial results released by NCUA late last week, and other results compiled by NASCUS.

However: asset growth for all charters of credit unions – state (federally and privately insured) and federal – dropped off considerably during the third quarter.

According to the third-quarter results from NCUA (and results from privately insured credit unions collected by private insurer American Share Insurance (ASI) and compiled by NASCUS), state credit unions (SCUs, federally and privately insured) held $901.5 billion in total assets, up 15.3% since the beginning of the year. That accounts for 49.9% of all credit union assets. Federal credit unions, (FCUs) meanwhile, held $905.6 billion in assets, up 12.8% from the year’s start – and accounting for 50.1% of all assets. There were 2,027 SCUs, and 3,213 FCUs, at the end of the third quarter.

Much of the asset growth, however, occurred in the first half of the year – particularly the second quarter – and asset growth slowed in the third quarter. For example, assets for SCUs expanded from year-end 2019 by 12.6% in the first six months of the year (about 8.4% in the second quarter), but only by about 2.7% from the second to the third quarter. FCUs saw a similar growth pattern, with asset growth at mid-year of 10.9% from the end of 2019, but only 1.8% from the second to third quarter.

An influx of savings spurred by stimulus checks to individuals (which were largely recorded in the second quarter), and by payments for enhanced unemployment insurance (UI) and through the Paycheck Protection Program (PPP) payments to workers, is attributed to the asset growth. There were no additional stimulus checks in the third quarter, and enhanced UI came to an end during the quarter.

“Although the 2,037 state-chartered credit unions make up only about 39% of all credit unions across the nation, they have an outsize influence on the lives of their nearly 60 million members who trust these institutions to safeguard their savings and provide them with needed financial services,” said NASCUS President and CEO Lucy Ito, referring to the more than 48% of all credit union members who belong to SCUs.

Other results from the third quarter results show:

- SCU memberships have grown by 3.3% since the beginning the year (1.4% during the third quarter, adding more than 810,000 memberships). FCUs have expanded their memberships by 2.2% since year-end 2019, and less than 1% in the third quarter for 600,000 memberships. Since the end of last year, more than 3.3 million memberships have been added, for a total of 125 million.

- The number of credit unions continued to drop through the first three quarters of the year, with 5,240 reporting their financial results at the end of the third quarter – 107 fewer than at the end of 2019. Of those, 37 were SCUs and 70 FCUs.

LINK:

NCUA Releases Q3 2020 Credit Union System Performance Data

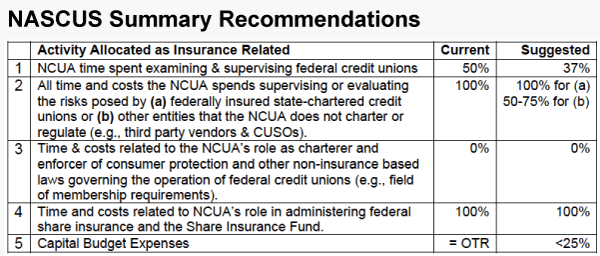

Dec. 4, 2020) NCUA should reconsider how it allocates expenses to the federal insurance fund for credit unions to pay for agency operations, in order to safeguard balance, equity – and ensure that more funds are available to cover any losses that may occur due to the financial impact of the coronavirus crisis, NASCUS told the agency this week.

In a presentation before the NCUA Board, NASCUS’ Lucy Ito made two key recommendations for expense allocations made by NCUA to cover its “insurance related costs” paid for by the National Credit Union Share Insurance Fund (NCUSIF) through transfers to the agency’s operating budget. The transfers are made via the overhead transfer rate (OTR), which NCUA is proposing be 1 percentage point higher in 2021 from this year, or 62.3%. The OTR represents the rate at which NCUA transfers money from the insurance fund to its operating budget to cover insurance-related costs.

The two key recommendations Ito made were: reduce the amount of the funds transferred to cover costs for examining federal credit unions (FCUs) from 50% to 37% of those costs, and reduce the amount of funds transferred to cover costs of evaluating risks of entities that NCUA does not charter or regulate (such as third-party vendors and CUSOs) from 100% to a range of between 50% and 75%.

Ito, providing the state system’s view of the agency budget, focused in her remarks exclusively on the OTR and costs that are allocated to it by the agency. She was one of three to make presentations to the NCUA Board members attending the meeting, Chairman Rodney Hood and Member Todd Harper. The others making presentations represented the Credit Union Natl. Assn. (CUNA) and Natl. Assn. of Federally Insured Credit Unions (NAFCU).

In recommending changes to the expense allocations, Ito said every dollar the agency transfers from the fund to cover expenses of the agency in “insurance-related costs” is a dollar that is not available to pay for credit union losses that are likely to arise as a result of the financial impact of the pandemic.

“The 1% increase in the OTR for 2021 means there will be $3.3 million less to cover losses by the fund,” Ito said.

In other comments, Ito recommended the agency reconsider how it allocates expenses paid by the fund for capital budget costs of its operations. For example, Ito said, given increasing state agency assumption of computer and other capital costs, “it would seem that the insurance fund would carry a much smaller percentage of NCUA’s computer software and other capital charges than the agency allocates to its role as the FCU chartering authority.”

She also suggested that the agency work with state supervisory authorities to validate their time allocation assumptions that make up portions of the OTR calculations. “We noted in last year’s budget briefing we would very much welcome the opportunity to sit with NCUA and understand out how NCUA reconciles the budgetary OTR with actual time allocations,” she said, adding that the invitation remains open from the association.

LINK:

NASCUS presentation, NCUA 2021 budget briefing (Dec. 2, 2020)

(Dec. 4, 2020) A new member will be sitting at the next meeting of the NCUA Board when it gathers in about two weeks, thanks to action taken by the Senate this week.

Kyle Hauptman

Kyle S. Hauptman was confirmed by the Senate Wednesday on a bipartisan vote of 56-39, clearing the way for his swearing in and subsequent participation in a vote slated Dec. 17 on the agency’s 2021-2022 budget.

Nominated June 18 to the NCUA Board by President Donald Trump, Hauptman has most recently served as a staff director for the economic policy subcommittee of the Senate Banking Committee and as an economic policy advisor to Sen. Tom Cotton (R-Ark.). He worked on the 2016 Trump presidential transition team and served as a policy advisor on financial services for 2012 Republican presidential nominee Mitt Romney (now a U.S. senator representing Utah).

Confirmed to a term that continues into August 2025, Hauptman will take the seat recently vacated by J. Mark McWatters, whose term on the board expired in August 2019. McWatters had been serving in holdover capacity until his resignation Nov. 20.

That resignation followed by one day McWatters’ noting during an open board meeting that he would not approve of the agency’s proposed budget without certain changes.

NASCUS President and CEO Lucy Ito congratulated Hauptman on behalf of the state credit union system. “We look forward to working with him over the coming years,” Ito said. “There are a number of key issues of importance to state credit unions, including maintaining an equitable overhead transfer rate from the NCUSIF, continued consideration of subordinated debt for use by all federally insured credit unions, and on-going dialogue and collaboration between state and federal regulators. We are eager to meet with the newest NCUA Board member to discuss these and other issues as together we work toward a strong, and safe, credit union system.”

Hauptman’s confirmation fills out the membership of the agency’s board, as he joins Chairman Rodney Hood and Member Todd Harper. Both Hood and Hauptman are Republican appointees; Harper is a Democrat appointee. Hauptman becomes the third member to join the board in less than two years: both Hood and Harper joined the board in the spring of 2019 (although Hood is serving a second stint on the panel, having served on the board from 2005-09).

During a board briefing Wednesday, both Hood and Harper publicly congratulated Hauptman on his confirmation. Harper, further, noted that all three board members’ names now begin with the letter “H,” replacing the “Ms” on the board (when Chairman Debbie Matz, and Board Members Rick Metsger and J. Mark McWatters all served on the board together).

Interestingly, the last time all three board members’ last names began with the same letter (the “Ms”), all three, eventually, served as board chairmen. Harper could be in line to become the next board chairman (as a Democratic appointee) after Joe Biden is inaugurated as president Jan. 20.