(Nov. 12, 2021) A final rule on field of membership (FOM) shared facility requirements will be at least one of the items on the Nov. 18 NCUA Board meeting agenda, released this week.

The board will also receive three board briefings from staff – including one on the agency’s modernized examination tools – and consider the agency’s 2022-26 strategic plan

The board meeting is scheduled to begin at 10 a.m. Thursday at NCUA headquarters in Alexandria, Va.; it will be live-streamed via the Internet.

The final rule, as proposed nearly a year ago (in December 2020), would “modernize” requirements related to service facilities for multiple-common-bond federal credit unions (FCUs).

The proposal – which modifies Part 701, Appendix B, of NCUA regulations — would, the agency said, include any shared branch, shared ATM, or shared electronic facility in the definition of “service facility” for a multiple-common-bond FCU that participates in a shared branching network.“

According to NCUA, the FCU need not be an owner of the shared branch network for the shared branch or shared ATM to be a service facility. “These changes would apply to the definition of service facility both for additions of select groups to MCB FCUs and for expansions into underserved areas.”

The proposal was issued for comment on a 2-1 vote, with now-Board Chairman Todd Harper dissenting. Harper said he questioned the proposal’s ability, without changes, to increase service to underserved areas.

The shared service proposal is one of two outstanding proposals the board agreed in September to consider in upcoming meetings in November and December. Next month, the board will consider a proposal on mortgage servicing rights, which Harper also opposed.

The future of unanimous approval for both the FOM and mortgage servicing proposals may be a bit brighter, however: Harper said at last month’s NCUA Board meeting that he hoped to be able to support both in the upcoming votes.

Regarding the modernized exam tools: the agency is rolling out new implements for evaluating credit unions. Those include the agency’s Modern Examination & Risk Identification Tool, (MERIT), as well as associated programs: the Data Exchange Application (DEXA), NCUA Connect, and the Admin Portal.

The other two briefing will be a quarterly report on the National Credit Union Share Insurance Fund (NCUSIF) and an update on the agency’s response to the COVID-19 pandemic.

LINK:

Agenda, NCUA Board Nov. 18 meeting

(Oct. 29, 2021) Each of three town halls will be led by a member of the NCUA Board at its diversity, equity and inclusion (DEI) conference set for three days early next month, the agency said this week.

NASCUS President and CEO Lucy Ito is also participating in the event, sitting on two panels.

NCUA Board Chairman Todd Harper will lead off with the first town hall at the agency’s DEI Summit, which runs from Nov. 2 to Nov. 4. His session will discuss DEI in relationship to 2020-21 newsworthy events and the importance of having a leadership commitment to DEI. Other topics will include racism in banking and the role of credit unions in DEI, according to an NCUA press release.

Board Member Rodney Hood will host the second day’s town hall, which features two panels on financial inclusion. The first from a “non-federal perspective,” the second from inside the agency (particularly through the agency’s Advancing Communities through Credit, Education, Stability and Support (ACCESS) initiative.

Board Vice Chairman Kyle Hauptman will host the third day’s town hall, focusing on credit union financial inclusion initiatives and partnerships with external organizations.

The agency said it would also host several concurrent sessions following the Nov. 3 and Nov. 4 town halls, focusing on DEI subjects.

In addition, the credit union think-tank Filene Research Institute will report on results of recent studies and analysis of diversity surveys and research.

NASCUS’ Ito appears on two panels at the Summit: The first on Tuesday (Nov. 2, 4-4:45 p.m. ET) in the “Fireside Chat: What is the Credit Union’s Role in this DEI Journey.” Appearing alongside the NASCUS leader will be CUNA President Jim Nussle and NAFCU CEO B. Dan Berger. Samira Salem, CUNA vice president of DEI, will moderate the session.

The second panel featuring Ito will be Wednesday (Nov. 3; 2:15- 3:45 p.m. ET) in the panel “How to Increase Gender Diversity in the C-Suite.” Also on the panel will be Mary McDuffie (Navy Federal CU president and CEO), Shruti Miyashiro (Orange County’s CU CEO), Tracey Jackson (ResourceOne CU CFO). Eleni Giakoumopoulos, WOCCU Global Women’s Leadership Network program director, will moderate the session.

Each day’s programs begin at 12:30 p.m. ET, NCUA said.

LINK:

Diversity, Equity and Inclusion Summit 2021

(Oct. 29, 2021) NCUA Board meetings in 2022 will be – again – on Thursdays, beginning at 10 a.m. ET, and skipping an August meeting, the agency said in a release this week. In most cases, the meetings will be on the third Thursday of the month – with the exceptions of January, May and September, when the meeting falls on the fourth Thursday of each month … NASCUS Credit Union Advisory Council Chairman Mike Williams, who is also president and CEO of Colorado Credit Union in Denver, was named a ‘Most Admired CEO’ by the Denver Business Journal this week. The award, the publication said, recognizes CEOs who are driving transformative change within their organization, industry, and the community … The Oregon Department of Consumer and Business Services has three openings for a Financial Examiner 3 extended to Nov. 29. See the link below for details (and other recent job openings) … Congrats to the New York Credit Union Association (NYCUA) for its steadfast efforts in achieving credit union authority to participate in its state’s program to provide commercial loans to small and mid-sized businesses at reduced interest rates. Legislation was signed by NY Gov. Kathy Hochul (D) to authorize credit unions to participate in the program – the culmination of an effort that NY credit unions began in the 1990s. The new law also allows marks the first time New York state has been authorized to deposit public funds in credit unions, according to NYCUA … Congrats, also, to CUNA, state associations and others for convincing congressional negotiators to keep out from the “framework” of the massive “build back better” legislation a provision that would require increased reporting of some members’ savings accounts by credit unions to the IRS. Reports Thursday indicated the provision has been omitted from the framework.

LINK:

NCUA Board Announces 2022 Meeting Schedule

(Oct. 22, 2021) Ransonware risks and threats to credit unions and other financial institutions are rising considerably, the NCUA Board was told Thursday, noting that the method now accounts for 10% of all cyber breaches.

The threat, NCUA Critical Infrastructure Division Director Ernie Chambers told the board, is enabled by cryptocurrency and has been cited as “among the largest of cybersecurity threats” today to financial institutions.

The cybersecurity presentation was made to the board partly in advance the updated Automated Cybersecurity Evaluation Toolbox (ACET), which will be introduced by the agency in a webinar set for next week (Oct. 28).

Chambers also cited phishing and supply chain attacks as key threats to the credit union system; he urged institutions to take steps to address each.

“NASCUS applauds NCUA’s comprehensive approach to fostering credit union cybersecurity resilience,” NASCUS’s Lucy Ito said. In addition to NCUA’s enhanced ACET self-assessment tool, she said, NASCUS supports the agency’s plan for rolling out Information Technology Risk Examination for Credit Unions (InTRExCU) in 2022. The system is based on the FDIC’s InTREx program for banks and has been adapted for credit union use.

“Several state agencies are already utilizing FDIC’s InTREx tools in state credit union IT examinations,” Ito noted. “This early adoption of InTREx in state regulator supervisory programs combined with NCUA’s InTRExCU pilot, together provide proof of concept for the relevance and value of adopting InTREx more broadly as a tool for evaluating credit union cyber hygiene and exposure.”

She said with most credit union CEOs citing cybersecurity risks as their greatest concern, utilizing a proven, scalable examination tool such as InTREx should be a “welcome addition to the national credit union system’s collective arsenal.”

LINK:

NCUA Board Briefing, Cybersecurity (in PowerPoint format)

(Oct. 1, 2021) Noting Harper’s comments about changes to the NCUA Board, NASCUS President and CEO said mandating that at least one board member have state credit union regulatory experience should be part of the conversation. “A board member who has served as a state credit union regulator would ensure that the state perspective is considered in the board’s deliberations, establishing diversity of voices and better fostering a robust dual charter system,” she said. “State-chartered credit unions now represent more than 50% of all credit union assets nationwide. Most state-chartered credit unions are federally insured. Without at least one board member with state credit union regulatory experience, NCUA has on occasion been prone to a federal credit union bias as the chartering body for federal credit unions.”

On third-party vendor authority, Ito reiterated NASCUS’ support for it, as long as NCUA relies on state exams for technology services providers where the authority exists. Further, she said, NASCUS supports efforts to strengthen state regulatory exam and supervision of third parties providing services to state-chartered credit unions.

(Sept. 17, 2021) A proposed rule on subordinated debt will be on the agenda of the NCUA Board when it meets next week, according to an agenda published Thursday by the agency.

According to the agenda posted on its website, the NCUA Board will consider a rule on the subordinated debt under parts 702 (capital adequacy) and 703 (investment and deposit activities) under its regulations.

Late last year, the agency adopted a subordinated debt final rule on allowing well-capitalized, federally insured credit unions to count the debt instrument as capital for risk-based net worth purposes. Under the final rule ultimately published in January of this year, the rule is slated to take effect Jan. 1, 2022. That date is the same that new risk-based capital rules for credit unions are to take effect.

The rule also grandfathered any secondary capital issued before the rule’s effective date of Jan. 1, and preserves that capital’s regulatory capital treatment for 20 years after the effective date. The “grandfathered secondary capital” generally, the agency said, remains subject to requirements in the agency’s current secondary capital rule.

Also on the agenda for the board’s meeting next week is:

- A quarterly report on the National Credit Union Share Insurance Fund;

- A review of the business loan rule for Oregon credit unions (to determine if the state rule covers all the provisions in the NCUA rule and is no less restrictive, thus exempting credit unions in the state from compliance);

- A 2021 mid-session budget review;

- And an item merely listed as “NCUA Board Agenda.” No other information is given.

The board meeting is scheduled to get underway at 10 a.m. ET, and will be streamed live via the Internet.

LINK:

NCUA Board Agenda for the Sept. 23, 2021 Meeting

(May 14, 2021) A final rule on investments in derivatives by credit unions, and two items that could have a significant impact on a savings insurance premium for credit unions, are all on the agenda for the NCUA Board when it meets on Thursday.

The final rule on derivatives follows up on a proposal from the agency issued in October, which was designed to make current regulations less prescriptive and more principles-based. The proposal would also expand federal credit unions’ (FCUs) authority to purchase and use derivatives as part of their interest-rate risk (IRR) management.

NASCUS, in its comment letter on the proposal filed with the agency in late December, said the state system supports the proposal, but made two recommendations to make the rule more flexible for the needs of state credit unions. First, NASCUS said the agency should eliminate redundant supervisory notice requirements where applicable. NCUA, the association wrote, should provide an exemption from its notice requirement for FISCUs in states where pre-approval or pre-notification is required to be given to the state regulator.

Second, NASCUS wrote that the agency should incorporate exempt derivatives transactions directly into part 741.219 of its rules – the section that covers FISCUs and investment requirements. Specifically, NASCUS “strongly recommended” that — to facilitate FISCU compliance – the agency should incorporate the excluded transactions under the proposal (under part 703.14 of NCUA rules, which only apply to FCUs) directly into a new subpart (d) of section 741.219. Restating the excluded transactions directly in the relevant FISCU rule, NASCUS wrote, “is a better organizational framework that more clearly communicates to FISCUs the required compliance obligations.”

NASCUS also acknowledged in its letter that a key part of the proposal is continued recognition by NCUA of the primacy of state law in determining investment authority for FISCUs.

Regarding the insurance fund and the future of a premium, the NCUA Board will also consider at next week’s meeting:

- Issuing a comment request on the National Credit Union Share Insurance Fund’s (NCUSIF) “normal operating level” (NOL), which is the reserve level at which the board has determined the fund can adequately cover any losses presented to the fund. The NOL plays a key role in determining whether a premium will be charged to credit unions to bolster the fund’s reserves. The subject of a premium has been the focus recently of considerable discussion. However, NCUA Board Chairman Todd Harper has repeatedly said the question is increasingly not if, but when, a premium will be charged. Separately (but related): In September, the FDIC Board adopted a restoration plan for the agency’s Deposit Insurance Fund (DIF) which — much like the NCUSIF — had been diluted by the massive influx of savings as a result of the financial impact of the coronavirus crisis. The FDIC plan would restore the fund’s reserve ratio to at least 1.35% of reserves to total insured funds within eight years, as required under federal law — but would require no “extraordinary measures” – such as increasing assessment rates. Instead, the agency said last fall that it would, over the next eight years: monitor deposit balance trends, potential losses, and other factors that affect the reserve ratio; maintain the current schedule of assessment rates for insured banks and other institutions; and provide updates to its loss and income projections at least semiannually.

- A quarterly report on the NCUSIF, which should include details on the latest equity level of the fund, which also has an impact on a future premium. Lately, the equity level (the amount of total reserves in the fund relative to total savings insured) has been dropping as insured savings have been growing, spurred by member deposits of federal stimulus payments and other savings. Federal law requires that if the NCUSIF equity ratio drops below 1.2%, the board must adopt a “restoration plan” to bring the equity ratio back up to the fund NOL – including a premium. The insurance fund closed 2020 with an equity level of 1.26%, well below the current NOL of 1.38% (but an improvement from earlier in the year when the equity level stood at just 1.22%).

The board meeting gets underway at 10 a.m. ET; audio of the meeting will be live-streamed via the Internet.

LINK:

NCUA Board meeting agenda, May 20

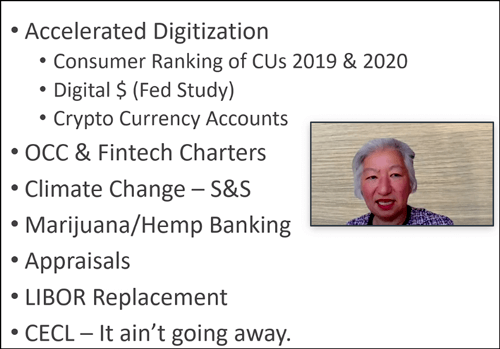

(April 30, 2021) Issues and policies being pursued by the state system were outlined this week by NASCUS President and CEO Lucy Ito during a presentation hosted by CU*Answers’ “The CUSO Challenge.”

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

Ito also laid out NASCUS’ approach for “renovating” the Federal Credit Union Act, to bring the underlying federal line more in line with contemporary times, and to give the state system (which now represents more than half of the total assets of the entire credit union system) fair representation.

Among other things, Ito recommended separating the insurance function from the supervisory role of NCUA, a long-standing position of the association. NASCUS’ position is that the current structure of the National Credit Union Share Insurance Fund (NCUSIF) presents a potential conflict of interest within the agency unless those functions are internally separated. (NASCUS has also noted that any changes to the statutory structure of the NCUSIF should be evaluated and developed in conjunction with state regulators and credit union stakeholders, since state regulators have experience and expertise with statutory and operational construct of the bank deposit insurance fund that would help inform possible changes to the insurance fund.)

She also noted NASCUS’ support for expanding the NCUA Board from three to five members. In any event, NASCUS also supports reserving one seat on the board for a person with experience as a state credit union regulator.

Other renovations to the FCU Act mentioned by Ito included: updating field of membership, regulatory capital, member business lending and investments authorities, and considering changes to board compensation, annual meeting and member expulsion requirements.

(April 23, 2021) While no new regulations were proposed or finalized, the NCUA Board did indicate at its meeting Thursday that final rules on two NASCUS-supported proposals – on capitalization of interest and derivatives — are nearing the point of being considered soon, according to comments during this week’s meeting.

In open session of the NCUA Board, Chairman Todd Harper said staff is “working through” issues on proposed rules for capitalization of interest and on derivatives. Harper said he was hopeful to see actions on the proposals “in the near future.”

The issue of action on proposed or pending regulations was brought up by Board Member Rodney Hood. Thursday’s meeting included only board briefings, on cybersecurity and an interim final rule addressing the impact of savings growth due to the coronavirus crisis on credit union capital.

Hood, in his comments, suggested the board work in the future “in a bipartisan manner” to develop board meeting agendas for “robust rulemaking opportunities.” Hood indicated that there are proposed rules awaiting action (and proposals waiting to be unveiled) that he and the other board members want to see move forward.

The capitalization of interest rule was proposed in November by the NCUA Board; it would remove the prohibition in agency rules against the capitalization of interest in connection with loan workouts and modifications, particularly as they struggled with the financial impact of the coronavirus crisis.

NASCUS, in its February comment letter, supported the proposal and called for its expeditious completion. NASCUS also recommended the agency reconsider the blanket prohibition against additional advances, to cover credit union fees and provide them with “the full range of options for managing and structuring loan work outs as other depository institutions.”

The derivatives rule was proposed in October; it would make the agency’s regulation less prescriptive and more “principles-based,” expanding federal credit unions’ authority to purchase and use derivatives as part of their interest-rate risk (IRR) management. NASCUS likewise supported the proposal in its December comment letter, calling for two changes: eliminate the redundant supervisory notice requirements where applicable, and incorporate exempt derivatives transactions directly into part 741.219 of NCUA rules – the section that covers federally insured state-chartered credit unions (FISCUS) and investment requirements.

NASCUS also noted that the proposal continues recognition by NCUA of the primacy of state law in determining investment authority for FISCUs.

Both items were issued for comment without objection by any members of the board.

NASCUS comment: Proposed Rule — Derivatives (RIN 3133–AF29)

(April 16, 2021) In a development Friday morning, the NCUA Board announced it had adopted an interim final rule (IFR) by notation vote that reduces the earnings retention requirement for credit unions classified as adequately capitalized, and permitting an undercapitalized credit union to submit a streamlined net worth restoration plan if it becomes undercapitalized predominantly because of share growth during the coronavirus crisis.

The board adopted the IFR – which is substantially similar to a rule adopted last May but that lapsed at year-end 2020 – in a notation vote. The IFR is also the subject of a briefing for the board at its regular monthly meeting Thursday (April 22). That same meeting will also include a board briefing on cybersecurity.

The IFR takes effect immediately; the vote also keeps the temporary measures in place until March 31, 2022.

Last May, the board issued an IFR that waived the earnings retention requirement for “adequately capitalized” credit unions and eased net worth restoration plan requirements for some “undercapitalized” credit unions. That rule, approved with an expiration date of Dec. 31, 2020, was intended to help ensure that federally insured credit unions (FICUs) remained operational and liquid during the COVID-19 crisis.

NCUA called this week’s rule “substantially similar” to the regulation adopted nearly a year ago. The agency said that, due to the pandemic’s continued financial and economic disruptions, it was necessary to reintroduce the two temporary relief measures.

Under the first provision of the IFR (reducing the earnings retention requirement for credit unions classified as adequately capitalized), NCUA said those credit unions unable to meet the requirement will not have to submit a written application requesting approval to decrease their earnings retention amount.

“However, if a credit union either poses an undue risk to the National Credit Union Share Insurance Fund or exhibits material safety and soundness concerns, the appropriate NCUA Regional Director may require the credit union to submit an earnings transfer waiver request,” the agency said.

Under the second provision (permitting an undercapitalized credit union to submit a streamlined net worth restoration plan if it becomes undercapitalized predominantly because of share growth due to the crisis), if a credit union becomes less than adequately capitalized for reasons other than share growth, it must still submit a net worth restoration plan under the current requirements in NCUA’s regulations.

In a statement, NCUA Board Chairman Todd Harper said the changes reflect the impact of the influx of savings by members into their credit unions from stimulus payments and other sources. “The latest round of stimulus spending has further expanded credit unions’ balance sheets,” Harper said. “As a result, many well-run credit unions with positive earnings now have lower net worth ratios. Given the continued uncertainty with the pandemic and share growth many credit unions are seeing, this targeted, tailored and temporary rule will provide critical relief so eligible credit unions can focus their limited resources on their members’ needs instead of planning for earnings transfers and developing detailed net worth restoration plans.”

Board Vice Chairman Kyle Hauptman characterized the rule as a method for allowing credit unions to stay focused on serving members. Board Member Rodney Hood observed that “while this temporary relief wasn’t widely utilized last year when it expired, it now appears we need this tool now for credit unions.”

The IFR has a 60-day comment period, ending on June 18.

LINKS:

Temporary Regulatory Relief in Response to COVID-19 – Prompt Corrective Action

NCUA Board April 22 open meeting agenda

(March 19, 2021) Asset data as of March 31, 2020 will be used to determine the applicability of regulatory asset thresholds for such things as capital planning and stress testing at larger credit unions for the remainder of this year and all of next, under an interim final rule approved by the NCUA Board Thursday.

The new rule will affect about 10 large credit unions, NCUA said, including those with state charters. It is meant to mitigate the impact of the influx of savings to credit unions, particularly larger ones, during the coronavirus crisis. The savings surge has been fueled, at least in part, by federal stimulus payments (including the one just recently approved by Congress of $1,400 to individuals). Coupled with that surge, NCUA said, has been a slowdown in spending by consumers as they hunkered down for the economic downturn caused by the crisis, keeping share accounts higher.

“For FICUs (federally insured credit unions) just below $10 billion in assets, these factors have resulted in their balance sheets swelling by an average of about 14 percent, and in one case by more than 34 percent,” NCUA said. “In contrast, in 2019, FICUs with assets just below the $10 billion threshold had an average asset growth of only 9 percent.”

The agency asserted that, due to the surge in assets, many FICUs have been or will be pushed over the asset thresholds subjecting them to additional regulatory requirements, or supervision by the agency’s Office of National Examinations and Supervision (ONES), which mostly oversees larger credit unions. “Complying with these new or more stringent regulatory standards would impose additional transition and compliance costs on such FICUs that otherwise may not have become subject to these requirements at this time,” NCUA stated. “This interim final rule gives affected FICUs more time to either reduce their balance sheets, or to prepare for higher regulatory standards.”

NCUA also estimated that the balance sheet growth has not significantly increased the risk profile of the affected credit unions, although the agency reserves the authority to subject a credit union to ONES supervision or to designate it as a Tier I/II/III credit union depending on the circumstances surrounding the growth and the risks associated with the type or assets held or any additional activities undertaken by a credit union.

The interim final rule – approved unanimously by the board — takes effect upon publication in the Federal Register; a comment period of 60 days was also set for the rule.

In other action, the board approved (also unanimously) another interim final rule, that one updating its regulations for the Central Liquidity Facility (CLF). The changes grew out of the passage in December of the Consolidated Appropriations Act, 2021. That legislation extended several enhancements to the CLF (such as more flexible memberships) made in last year’s Coronavirus Aid, Relief, and Economic Security (CARES) Act. The new rule amends the NCUA’s CLF regulation to reflect these extensions. This rule also takes effect on publication in the Federal Register, and also will have a 60-day comment period.

LINK:

Interim final rule: Asset thresholds

Interim final rule: CLF conforming rules

(March 12, 2021) Two interim final rules – one on the agency’s Central Liquidity Facility, the other on asset thresholds pertaining to large credit unions – are slated for action Thursday (March 18) by the NCUA Board.

The three-member board, meeting in a virtual setting with audio transmitted via the Internet, will also receive a briefing on the NCUA Guaranteed Note (NGN) and Asset Management Estates Programs.

The interim rule on the CLF is under part 725 of the agency’s rules and regulations (governing operations and membership in the facility). The asset thresholds interim rule pertains to parts 700 (definitions), 702 (capital adequacy), 708a (bank conversions and mergers), 708b (mergers among credit unions), and 790 (NCUA operations).