Notice of Proposed Rulemaking and Request for Comment

NCUA: Subordinated Debt

Read NASCUS Legislative and Regulatory Affairs Department Summary Here

October 5, 2022

At the September 22, 2022, NCUA Board meeting, the Board approved for comment a proposed rule that would amend the Subordinated Debt rule (the Current Rule), which the Board finalized in December 2020 with an effective date of January 1, 2022. The proposal would make two changes related to the maturity of Subordinated Debt Notes and Grandfathered Secondary Capital (GSC).

The proposed rule also includes four other minor modifications to the current subordinated debt rule. The proposed rule in its entirety can be found here. Comments are due December 5, 2022.

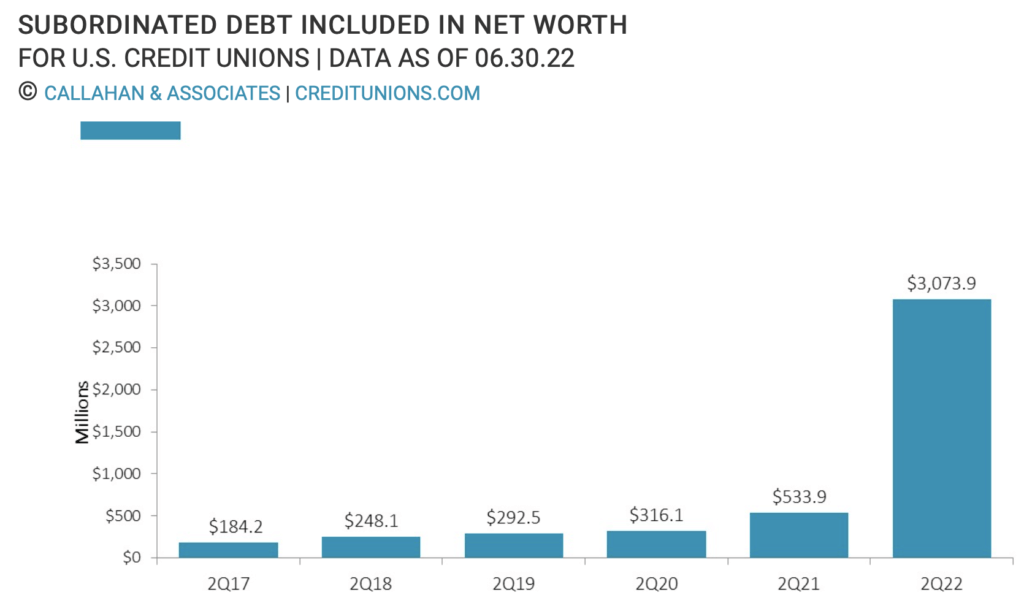

Aug. 22, 2022 — Updated rules from the National Credit Union Administration have resulted in a massive jump in the number of credit unions issuing subordinated debt and the overall dollar amount.

- Recent changes to regulations from the National Credit Union Administration have resulted in a surge in the number of credit unions issuing subordinated debt and the dollar amount being issued.

- Low-income credit unions (LICUs) have at times issued subordinated debt to expand their operations, typically using the capital for lending expansion and servicing, or for the acquisition of newer and more efficient financial technology. The advantage of subordinated debt is that credit unions can make loans or provide other services to members with borrowed money that is counted as net worth and thus not counted against their capitalization.

- Recently, the NCUA expanded the number of credit unions eligible to issue subordinated debt to include complex credit unions (those with more than $500 million in total assets) and newly chartered credit unions. This change was made in conjunction with the release of new regulatory capitalization ratios — risk-based capital and the Complex Credit Union Leverage Ratio — which are also designed for complex credit unions. Although only LICUs are permitted to include subordinated debt in net worth, complex and new credit unions can use it to bolster the new RBC value. By allowing these credit unions to issue subordinated debt, the NCUA is providing these institutions with a new route to adjust to the new regulatory thresholds.

- This new capitalization-requirement rules spurred a 170.8% quarterly increase in the dollar value of subordinated debt issued by credit unions industrywide. Alongside dollar growth, the number of credit unions using this tool to increase net worth is also expanding. As of the second quarter of 2022, 132 credit unions have issued subordinated debt. This is up from 86 institutions in the first quarter of 2022 and 80 in the fourth quarter of 2021, before the regulatory changes took effect. This increase has been driven by larger credit unions issuing subordinated debt as net worth: 64 of these 132 credit unions are complex credit unions, up from 44 in the fourth quarter of 2021.

Courtesy of Callahan, CreditUnions.com

(Dec. 17, 2021) A final regulation tweaking the agency’s subordinated debt rule by amending the definition of “Grandfathered Secondary Capital” to include any secondary capital issued to U.S. government or one of its subdivisions under an application approved before January 1, 2022, irrespective of the date of issuance, was also approved by the board.

NCUA said the change will benefit eligible low-income credit unions that are either participating in the Treasury Department’s “Emergency Capital Investment Program” (ECIP) or other programs administered by the federal government that can be used to fund secondary capital, “if they do not receive the funds for such programs by Dec. 31.”

The final rule also provides that the expiration of regulatory capital treatment for these issuances is the later of 20 years from the date of issuance or Jan. 1, 2042.

NASCUS, in its comment letter on the proposal (submitted in October) recommended that “a basic sunset provision could provide compatibility between the Subordinated Debt rule and the rules of qualifying government funding program.”

LINK:

Final Rule, Parts 702 and 741, Subordinated Debt

NASCUS comment: Subordinated Debt 2021

(Nov. 12, 2021) Any issuances of secondary capital not completed by Jan. 1 will be subject to the requirements of the new subordinated debt rule, which becomes effective on that date, according to a letter published late last week by NCUA.

NASCUS has published a summary of the letter, which like all summaries from NASCUS, is available to members only.

The NCUA letter to credit unions ((LTCU 21-CU-13) states there is one potential exception: low-income designated credit unions are allowed to issue secondary capital approved in 2021, irrespective of the date of issuance, under a proposed rule issued by the agency in September. A final version of the rule, the letter stated, will be considered by the NCUA Board by Jan. 1.

The subordinated debt rule was approved by the NCUA Board nearly a year ago (in December 2020), with an effective date of the beginning of the new year. That rule allows well-capitalized, low-income designated, federally insured credit unions to count subordinated debt as capital for risk-based net worth purposes.

The proposal issued in September would amend that rule, slightly, by accommodating low-income credit union (LICU) access to federal investment programs, most notably the Treasury Department’s Emergency Capital Investment Program (ECIP). That program directs Treasury to make investments in “eligible institutions” to financially support small businesses and consumers in low-income and underserved communities. Those institutions include federally insured credit unions that are minority depository institutions (MDIs) or community development financial institutions (CDFIs) that are in sound financial condition. The investments are made in the form of subordinated debt.

Funding of secondary capital approved under the current rule would be permitted under the proposal beyond 2021, without the need to reapply under the subordinated debt rule – thus giving those credit unions a measure of regulatory relief.

“Given the current 45-day review period for secondary capital plans, any low-income credit union still planning to submit a secondary capital plan should do so as soon as possible,” the NCUA letter states. “Further, if a low-income designated credit union plans to submit a secondary capital plan this year, it should consider using the application requirements in section 702.408 of the final subordinated debt rule when drafting its plan and submitting an application.

“This can help avoid having to resubmit documentation as long as the application meets the requirements of the final rule,” NCUA wrote.

LINKS:

NCUA LTCU 21-CU-13: Subordinated Debt Final Rule Effective January 1, 2022

(Oct. 29, 2021) Now is the time to consider additional changes to the new subordinated debt rule – rather than adopt just one change to the rule — to ensure the rule is properly calibrated for use by low-income credit unions (LICUs), NASCUS told NCUA in a comment letter this week.

The NASCUS comment letter addressed a proposal issued Sept. 23 by the NCUA Board to amend its new subordinated debt rule (which takes effect Jan. 1) to accommodate credit union access to federal investment programs. No other changes to the new rule were offered. The proposed amendment put forward last month, according to NCUA staff, would amend the definition of “grandfathered secondary capital” to include any secondary capital issued to the U.S. government or one of its subdivisions under an application approved before Jan. 1, “irrespective of the date of issuance” (that is, when funds are issued), primarily to benefit low-income credit unions (LICUs).

The letter noted that the proposed amendment is necessary to permit LICUs to participate in the Treasury Department’s Emergency Capital Investment Program (ECIP) without having to reapply for capital treatment rule after the subordinated debt rule takes effect at the start of the new year. The association said it was fine with that change.

However, NASCUS added, the state system also supports additional changes to the subordinated debt rule to “maximize ECIP benefits to LICUs and further reduce regulatory burden.”

NASCUS wrote that it “strongly urged” the agency to “continue evaluating whether the Subordinated Debt rule is properly calibrated to the distinct features of the LICU ecosystem so as not to impede the important work done by these credit unions.”

For example, NASCUS argued, the agency should amend the final subordinated debt rule to allow instruments with 30-year maturities. “While NCUA will now permit LICUs to accept 30-year subordinated debt investment from the ECIP, the agency maintains that LICUs may only recognize 20 years of capital benefit from the funding,” NASCUS wrote. “There is no such fixed 20-year maturity limit in the current secondary capital rule for LICUs, and NCUA would be well within the spirit of the new final subordinated debt rule to allow ‘Grandfathered Secondary Capital’ to maintain the flexibility to set maturity limits based on funding needs and the marketplace.”

In general, the agency’s subordinated debt rule should provide for automatic exceptions to accommodate the terms of subsequent emergency government programs, NASCUS recommended. “Given the lingering effects of the pandemic, it is likely there could be additional Treasury Department funding programs and NCUA should provide certainty that credit unions will have equal opportunity to participate in those,” NASCUS wrote. “A basic sunset provision could provide compatibility between the Subordinated Debt rule and the rules of qualifying government funding program.”

LINK:

(Oct. 22, 2021) Eligible low-income credit unions (LICUs) may accept 30-year subordinated debt investments from a Treasury program meant to encourage the institutions to augment efforts to support small businesses and consumers, NCUA announced Thursday.

In a letter to credit unions (LTCU 21-CU-11) Thursday, the agency said the LICUs may accept the subordinated debt investments from the Treasury Department’s Emergency Capital Investment Program (ECIP). In addition, the agency said, the credit union may treat the investment as secondary capital in accordance with NCUA regulations. That is, provided that the LICU has an agency-approved secondary capital plan by year’s end.

According to NCUA Board Chairman Harper, the policy will allow ECIP-participating credit unions to fulfill that statutory mission and advance economic equity and justice. “Going forward, the NCUA will pursue additional action to permit ECIP funding to count as regulatory capital for the entire time it is held,” he said.

The agency’s subordinated debt rule, adopted in January, includes a 20-year limitation on the regulatory capital treatment of “Grandfathered Secondary Capital,” NCUA said. That is defined as any secondary capital issued under a secondary capital plan that was approved by the NCUA before Jan. 1, 2022. The agency indicated it plans, in the future, to clarify that ECIP participating credit unions may count ECIP funding as regulatory capital for the entire time it is held.

NCUA said the latest LTCU is the second step in a three-step process for ensuring credit unions can use ECIP. The first step was a proposed rule issued earlier this year to allow eligible credit unions to accept ECIP funding in 2022 without having to fill out a new subordinated debt application after the effective date of the new rule. The third step, according to the agency, will be more NCUA action – “sometime in 2022” — to permit ECIP funding to count as regulatory capital for the entire time it is held.

LINK:

NCUA LTCU 21-CU-11: Emergency Capital Investment Program Participation

(Oct. 8, 2021) Three new summaries were posted by NASCUS this week on: An NCUA regulatory alert on credit union credit card data submission to the CFPB; an NCUA letter to credit unions about the expiration of homeowner protection programs during the coronavirus crisis; and NCUA’s proposal to amend its subordinated debt rule to allow for the Treasury Department’s Emergency Capital Investment Program (ECIP).

All of the summaries are available to members only.

On Sept. 29, the NCUA issued a “regulatory alert” (21-RA-09) that essentially put credit unions on notice that they may begin submitting data on credit card agreements with their members, and applying data submission requirements, to CFPB’s “Collect” website, which gathers credit card information. The alert also lists important dates for credit unions to consider when submitting their data.

On Sept. 27, the agency sent a letter to federally insured credit unions (letter 21-CU-09), which outlined “critical information” for compliance with expiring pandemic-era homeowner protection programs. The letter noted several key areas, including the deadline for granting forbearance on mortgage payments. It also outlined steps that credit unions may take to continue providing relief to homeowners, even though several programs had expired.

Finally, on Sept. 23 – because of its monthly meeting – the NCUA Board issued a proposal to amend its new subordinated debt rule to accommodate credit union access to federal investment programs – but making no other changes to the rule taking effect Jan. 1. The proposal, according to NCUA staff, would amend the definition of “grandfathered secondary capital” to include any secondary capital issued to the U.S. government or one of its subdivisions under an application approved before Jan. 1, “irrespective of the date of issuance” (that is, when funds are issued), primarily to benefit low-income credit unions (LICUs).

LINKS:

NASCUS Summary: Navigating and Understanding the End of Pandemic-Era Homeowner Protection Programs

NASCUS Summary: Changes to NCUA Subordinated Debt rule

(Sept. 24, 2021) NASCUS President and CEO Lucy Ito agreed with the NCUA Board for proposing the secondary capital changes to the subordinated debt rule scheduled to take effect at the first of next year. “The state system appreciates the board’s proposal to essentially make subordinated debt more accessible to LICUs,” Ito said. “That will serve to strengthen the use of subordinated debt and reduce burden on LICUs—two goals the state system has been seeking for years.”

Regarding the action on the three rules over the next three months – and particularly expansion of CUSO authorities, Ito noted that NASCUS supports the agency obtaining exam authority over technology service providers (TSPs) that provide services to federally insured credit unions — provided that any such authority requires NCUA to rely on state examinations of such service providers where such authority exists at the state level. Further, she noted, NASCUS supports efforts to strengthen state regulatory exam and supervision of third parties providing services to state-chartered credit unions.

(Sept. 24, 2021) A proposed change to the new subordinated debt rule to accommodate credit union access to federal investment programs – but making no other changes to the rule taking effect Jan. 1 – was approved unanimously for a 30-day comment period by the NCUA Board Thursday.

In other action, the board agreed – on a split vote, with Chairman Todd Harper dissenting – to act on three outstanding proposed rules over the course of the next three, monthly board meetings dealing with credit union service organization (CUSO) authorities, field of membership (FOM) shared service facility requirements, and mortgage servicing rights (see following item).

The subordinated debt proposal, according to NCUA staff, would amend the definition of “grandfathered secondary capital” to include any secondary capital issued to the U.S. government or one of its subdivisions under an application approved before Jan. 1, “irrespective of the date of issuance” (that is, when funds are issued), primarily to benefit low-income credit unions (LICUs).

According to NCUA, the benefit would accrue to the LICUs that are either participating in the Treasury Department’s Emergency Capital Investment Program (ECIP) — or other programs administered by the federal government – “that can be used to fund secondary capital, if they do not receive the funds for such programs by Dec. 31, 2021.”

This proposal also provides that the expiration of regulatory capital treatment for the issuances is the later of 20 years from the date of issuance or Jan. 1, 2042, according to NCUA.

The ECIP (created by this year’s Consolidated Appropriations Act) directs Treasury to make investments in “eligible institutions” to financially support small businesses and consumers in low-income and underserved communities. Those institutions include federally insured credit unions that are minority depository institutions (MDIs) or community development financial institutions (CDFIs) that are in sound financial condition. The investments are made in the form of subordinated debt.

However, although LICUs are also eligible to apply to NCUA for secondary capital treatment for the investments, under current rules those institutions approved by NCUA for the program and not funded by year’s end would have to reapply for regulatory capital treatment under the subordinated debt rule.

The proposal would permit funding of secondary capital approved under the current rule, beyond 2021, without the need to reapply under the subordinated debt rule – thus giving those credit unions a measure of regulatory relief.

According to NCUA, as of Sept. 17, 44 LICUs have received approval to issue secondary capital under the ECIP for an aggregate amount of approximately $1.9 billion.

LINK:

Proposed Rule, 702 and 703, Subordinated Debt

(Sept. 17, 2021) A proposed rule on subordinated debt will be on the agenda of the NCUA Board when it meets next week, according to an agenda published Thursday by the agency.

According to the agenda posted on its website, the NCUA Board will consider a rule on the subordinated debt under parts 702 (capital adequacy) and 703 (investment and deposit activities) under its regulations.

Late last year, the agency adopted a subordinated debt final rule on allowing well-capitalized, federally insured credit unions to count the debt instrument as capital for risk-based net worth purposes. Under the final rule ultimately published in January of this year, the rule is slated to take effect Jan. 1, 2022. That date is the same that new risk-based capital rules for credit unions are to take effect.

The rule also grandfathered any secondary capital issued before the rule’s effective date of Jan. 1, and preserves that capital’s regulatory capital treatment for 20 years after the effective date. The “grandfathered secondary capital” generally, the agency said, remains subject to requirements in the agency’s current secondary capital rule.

Also on the agenda for the board’s meeting next week is:

- A quarterly report on the National Credit Union Share Insurance Fund;

- A review of the business loan rule for Oregon credit unions (to determine if the state rule covers all the provisions in the NCUA rule and is no less restrictive, thus exempting credit unions in the state from compliance);

- A 2021 mid-session budget review;

- And an item merely listed as “NCUA Board Agenda.” No other information is given.

The board meeting is scheduled to get underway at 10 a.m. ET, and will be streamed live via the Internet.

LINK:

NCUA Board Agenda for the Sept. 23, 2021 Meeting

NASCUS’ Lucy Ito discusses achievements and NASCUS, and the outlook for credit unions, during her interview with Mike Lawson, CUBroadcast.com (click on the arrow to view the complete video)

(June 4, 2021) Bringing attention to the overhead transfer rate (OTR) policies of NCUA, and securing authority for credit unions to issue subordinated debt, are two of the achievements NASCUS President and CEO Lucy Ito cited as attained during her tenure as leader of the state system organization during a video interview this week.

In May, Ito announced that she would retire from her position at the association, effective at the beginning of 2022.

Responding to questions from Mike Lawson of CUBroadcast (a web-based video interview program) Ito said that raising awareness of the OTR – the rate at which the agency transfers funds from National Credit Union Share Insurance Fund (NCUSIF) to cover insurance-related operating costs of the agency – ultimately resulted in the agency making changes to the formula for determining the rate.

In 2017, the NCUA Board voted to adopt a “simplified approach” to setting the rate, reflecting that “safety and soundness is not the sole domain of the insurer.” Reform of the OTR methodology had been a target for NASCUS and the state system for more than 20 years.

She also noted as an achievement the new subordinated debt rule, which was finalized by NCUA in December and is scheduled to take effect at the beginning of 2022. The rule would allow well-capitalized, federally insured credit unions to count subordinated debt as capital for risk-based net worth purposes. It was long sought by the state system, which has argued that such a rule would bring regulation of federally insured credit unions in line with regulations of some states that already allow their credit unions to issue secondary capital, including in the form of subordinated debt.

However, in her interview this week, Ito said the state system continues to look for changes in the rule. She noted the benefit of having a rule in place, and that “that’s something we can work with.”

In other comments during the 20-minute interview, Ito:

- Noted the common denominators of people who work in credit unions as being “service and duty.”

- Reflected on the commonalities of state regulators and leaders of credit unions, as both groups are service oriented and really feel a responsibility to protect and help others.”

- Suggested that the best way for the credit union community to succeed and maintain relevancy to consumers — in the face of mounting competition from such things as digital currencies and players such as PayPal – is collaboration among themselves and their related organizations (including associations). “Where there are shared problems, and shared objectives, let’s work together to address both,” she said.

(March 12, 2021) Two new summaries of final rules on corporate credit union purchase of subordinated debt, and on joint ownership share accounts, were posted by NASCUS this week.

Both are available to members only.

In October the NCUA Board approved a new corporate credit union rule that, as proposed, included a section on corporate purchase of credit union subordinated debt. However, the portion on purchase of subordinated debt was left out of the final rule. The board said then it would adopt that portion of the rule once it had finalized the subordinated debt final rule. Since that rule was adopted in December, the board then finalized late last month the subordinated debt portion of the corporate rule. NASCUS supported the provision.

The final rule takes effect Jan. 1.

The joint ownership share accounts final rule was approved by the NCUA Board at its Feb. 18 meeting. The rule, which takes effect March 26, would allow account records information other than a signature card to support the insured status of a joint ownership share account in a credit union. The final rule provides federally insured credit unions with an alternative method to satisfy the membership card or account signature card requirement. NASCUS supported the proposal.

LINKS:

NASCUS summary: Corporate Credit Unions (purchase of subordinated debt) (members only)

NASCUS summary: Joint Ownership Share Accounts (members only)