One of my biggest pet peeves in all of finance is the overdraft fee. I first wrote in 2019 that we were moving to a world of no overdraft fees. This was before major banks changed anything in response to the fintech push for no overdraft fees.

By 2021, it was clear that we had reached a tipping point on overdraft fees as many major banks either eliminated the practice or reduced the amount of their fees. This is partly due to the CFPB and their targeting of so-called “junk fees” like overdrafts. This has resulted in a dramatic drop in overdraft revenue for banks.

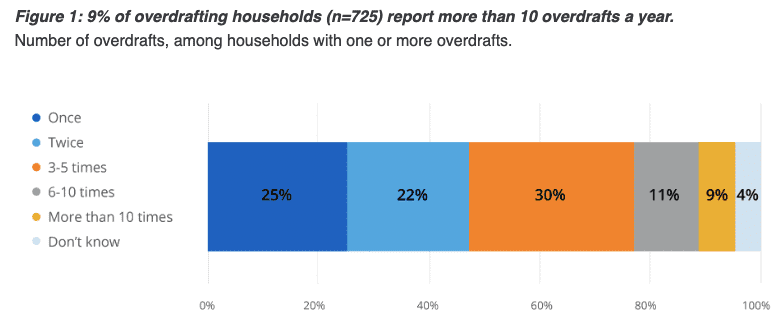

With this backdrop, I was interested in receiving an update from the Financial Health Network on overdraft fees as part of their annual FinHealth Spend Report (the full report will be out later this month). This report examines household spending on various financial products such as overdraft, payday and pawn, credit cards, and auto loans.

There were some very interesting findings in this report:

- 17% of U.S. households reported having overdrafted in 2022, unchanged from 2021

- 46% of Financially Vulnerable households reported paying an overdraft or NSF fee in 2022

- 9% of U.S. households that overdraft reported doing so more than ten times

It is the last point I want to focus on here. For the population who overdraft a lot (more than ten times a year), 35% of them said their last overdraft was intentional. So, they are using their bank account for short-term and costly funding. If you are talking APRs, this type of funding can go as high as 18,000%—no wonder the CFPB is cracking down on the practice.

For small transactions, those less than $25, 60% of respondents would have rather had their transaction declined than send them into an overdraft. But that means 40% of people are fine paying a $35 fee for overdrawing their account by less than $25.

We are moving towards a better system for overdrafts

Many fintech companies offer short-term financing when money is needed. Dave pioneered this product, but companies like Chime, Varo, MoneyLion, and Current all offer affordable small-dollar financing or fee-free overdrafts.

The report also shared that 81% of households overdrafted more than 10 times in 2022 prefer to incur a fee rather than have the purchase or payment declined. So, these people living on the financial edge are happy to pay a fee, but they really need a program that helps them get back on their feet.

It feels like we are in a transition period right now. The old overdraft system has been chipped away by fintechs, with many banks now jumping on board to offer no overdraft fees. But we are not yet where the most financially unstable people can rely on their financial institutions to provide inexpensive options.

I want to see a world where no financial institution can make significant money in fees off the most vulnerable subset of their customer base. It should no longer be expensive to be poor. We are on our way to this world, but more work needs to be done. This new report from the Financial Health Network makes that clear.

Courtesy of Peter Renton, FintechNexus

Courtesy of Moebs $ervices, moebs.com

The result would be:

- 678.2 Million debit cards purchases of gas, groceries, dentist, etc., would be declined.

- 60 Million Americans’ ACH payments returned NSF for cell phones, auto loans, mortgages, etc.

- $33.4 Billion of overdraft revenue would not be charged to the consumer.

- 111,000 financial institution employees would lose their jobs.

This is what the Consumer Financial Protection Bureau, not Congress, is considering doing. The CFPB reports to the President of the United States, not Congress.

What follows is Moebs $ervices’ Study on The Evolution of Overdrafts done in two parts.

- This is Part I – the History of Overdrafts.

- Part II – the Overdraft Solution is subsequently provided in the next issue.

(If you would like a copy of the full study now, email [email protected]).

The Evolution of Overdrafts

Study by Moebs $ervices, Inc. ©2022

Consumers make financial mistakes. Most are just ordinary errors while some are intentional and even fraudulent. Checking accounts, or transaction accounts, as the rest of the world calls them, suffer the brunt of these errors. The leading cause of these mistakes, or 77.4% of all service charges on deposits, are overdrafts.

These facts come from an extensive Overdraft Study by Moebs $ervices, an economic research firm.

An overdraft is defined as a credit, but not a loan by the Federal Reserve and other regulators. An overdraft is when a transaction account has a debit balance, or withdrawals (debits) mainly debit cards, exceed deposits (credits) mainly direct deposits of payroll or ACH credits.

Click here to read the full article

Related reading: Summary in CUToday.info “One Forecast: ‘Half of CUs Could Close”

From CU Times: The answer to how credit unions can replace lost overdraft fee revenue lies in their card programs

Some of the biggest players in financial services are eliminating overdraft fees. Bank of America and Wells Fargo are just a few of the big names either reducing or eliminating overdraft fees, and many credit unions are also scrapping these fees.

While overdraft fees have been a nuisance to consumers, they are not the only ones pushing for this change. Regulators are becoming increasingly suspicious of overdraft fees, too. With this kind of pressure building, more and more financial institutions are likely to follow suit and say goodbye to overdraft fees.

Without this revenue source, where does this leave financial institutions? A study from the Center for Responsible Lending found that, for institutions with assets of $1 billion or more, overdraft or insufficient funds fees are about 5% of their non-interest income. When overdraft fees disappear, how can a credit union replace that revenue? For many credit unions, the answer lies in their card programs.

The Current State of Cards

Credit and debit cards are another source of non-interest income for credit unions because of the interchange fees they bring in. Most institutions get their interchange check every month and take it for granted. It’s easy money. If it’s not broken, why fix it?

The fact of the matter is credit unions have a huge opportunity to grow their interchange revenue by making some adjustments to their card programs and this growth can help soften the blow of losing out on overdraft fees. Regardless of their overdraft fee strategy, however, this is an important opportunity for credit unions to become more successful and help their bottom line, while also meeting the needs of members.

Read More Here

Courtesy of Kelly Payne, Credit Union Times

![]() Related article: ‘One Of The Biggest Concerns’ Facing The Movement

Related article: ‘One Of The Biggest Concerns’ Facing The Movement

Is the growing trend by some large banks and larger credit unions to reduce or even eliminate their nonsufficient funds fees creating a dilemma for smaller CUs? One credit union CEO told CUToday.info the issue is “one of the biggest concerns facing the credit union movement in many years.”

Feb. 4, 2022 — The phrase “overdraft protection” does not appear in the “semiannual regulatory agenda” published this week by the CFPB in the Federal Register. But there may be more to come on that, in future, on that and other issues.

According to the agenda filed by the bureau, it expects that its new director – Rohit Chopra, confirmed last fall by the Senate – “will assess what regulatory actions the Bureau should prioritize to best further its consumer protection mission and that the Spring 2022 Agenda will reflect his priorities.”

Recently, Chopra has signaled that the agency is looking closely at overdraft programs. In December, the agency released a statement that three of the nation’s largest banks brought in more than two of every five dollars charged in overdraft fees in 2019, while smaller financial institutions – which charged less on average – were also heavily reliant on the fee income from the programs. In a statement, Chopra said then the bureau would be taking action “to restore meaningful competition to this market.”

However, he gave no timing for the action.

In the meantime, apparently, the bureau is continuing to work on other issues that may emerge in 2022 as rulemakings. Among them, according to the semiannual regulatory agenda published by the agency:

- Public availability from financial institutions of certain information from credit applications made by women-owned, minority-owned, and small businesses.

- Addressing the availability of consumer financial account data in electronic form.

- Certain regulations relating to “Property Assessed Clean Energy” (PACE) financing (a tool for consumers to finance certain improvements to residential real property).

- Quality controls for automated valuation models (AVMs), with other federal financial institution regulators

- Closing out its rulemaking over the discontinuation of LIBOR, in particular by helping “to ensure that any changes to an index underlying [certain] loans (including home equity, student, reserve mortgages and others) as a result of the transition to a different index due to the discontinuation of LIBOR are done by industry in an orderly, transparent, and fair manner.”

LINK:

CFPB Semiannual Regulatory Agenda

(Jan. 21, 2022) Credit risk management, cybersecurity and payment systems are the three top supervisory priorities for NCUA, the agency said this week.

Additionally, the agency indicated it will also be taking a closer look at overdraft programs at credit unions, with an eye to perhaps further action in 2023.

Overall, NCUA said in its letter to credit unions (22-CU-02), it will continue to conduct examination and supervision activities primarily offsite, given the uncertainty associated with the coronavirus crisis.

“Working with our public health consultant, the agency continues to closely monitor the COVID-19 pandemic trends and will resume onsite examination and supervision work when safe to do so,” the letter stated.

On its apparent top priority of credit risk management, the agency said its examiners would continue to review management and mitigation efforts at credit unions. “For all lending programs, credit unions’ risk management practices should be commensurate with the level of complexity and nature of their lending activities,” the agency letter states. “Credit unions must maintain safe-and-sound lending practices and comply with consumer financial protection laws, including disclosures and regulatory reporting requirements.”

Examiners will focus on adjustments credit unions made to lending programs to address borrowers facing financial hardship, the letter states. Examiners will also emphasize reviewing policies that address the use of loan workout strategies, risk-management practices, and “new strategies implemented to provide funds to borrowers under distress, including programs authorized under the CARES Act and extended in the Consolidated Appropriations Act, 2021,” the letter states. Examiners will evaluate credit unions’ controls, reporting, and tracking of these programs, in particular, NCUA wrote.

“NCUA examiners will not criticize a credit union’s efforts to provide prudent relief for borrowers when such efforts are conducted in a reasonable manner with proper controls and management oversight,” the letter stated.

On cybersecurity, the agency said it is developing updated information security examination procedures tailored to institutions of varying size and complexity. The procedures will be piloted and finalized this year, NCUA said. “Cybersecurity risks remain a significant threat to the financial system,” the letter stated. “Ransomware, third-party/supply chain risks, and business email compromises, in particular, continue to be of concern.”

The agency asserted that payment systems are growing in complexity and risk for credit unions and consumers, pledging increased focus in the area. “Today’s environment of easy and fast electronic processing of transactions relies on technology, the applications and their controls, and the underlying security of the platforms facilitating the transactions,” NCUA wrote. “The changes in payment systems increase the risk of fraud, illicit use, and breaches of data security.”

Key points of the other priorities include:

- Overdraft programs (consumer financial protection): Examiners will request information about a credit union’s policies and procedures governing its overdraft programs and the monitoring tools and audit of its overdraft programs, as well as the communications it provides to consumers about such programs. “We anticipate using this documentation for a fuller review of credit unions’ overdraft programs in 2023,” NCUA wrote.

- Loan-loss reserving: The agency reminded that credit unions subject to generally accepted accounting principles (GAAP) are required to implement the current expected credit losses (CECL) accounting methodology by the start of next year. (Credit unions under $10 million are not required to follow GAAP.) All federal credit unions, the agency noted, will be required to have a reasonable reserve methodology, provided the methodology adequately covers known and probable loan losses. Federally insured, state-chartered credit unions (FISCUs) should refer to state law on GAAP accounting requirements and CECL standard applicability, the agency wrote.

- Loan participations: Examiners will verify that credit unions have evaluated the risk in the loan participation transactions and how that risk fits within the tolerance levels established by the credit union’s board. At a transactional level, NCUA said, each loan participation must have separate and distinct records for individual payments, including principal, interest, fees, escrows, and other information relating to individual loans.

- LIBOR transition: Examiners will focus on credit unions with significant LIBOR exposure or inadequate fallback language.

LINK:

NCUA Letter to Credit Unions 22-CU-02: NCUA’s 2022 Supervisory Priorities

(Dec. 17, 2021) Six regulatory activities in 2022 by CFPB have been identified by the agency as “key” actions, according to a rulemaking agency released Monday – but action on overdraft fees was not one of them.

The bureau said the list of matters the agency plans to pursue from now through Oct. 31 of next year “reflects the continuation of significant rulemakings that further our consumer financial protection mission and help to advance the country’s economic recovery from the financial crisis related to the COVID-19 pandemic.”

The key actions, the agency said are:

- Small Business Lending Data Collection

- Availability of electronic consumer financial account data

- Property Assessed Clean Energy (PACE) Financing

- Standards for Automated Valuation Models (AVMs)

- Facilitating transition away from LIBOR Index

- Reviewing existing regulations and market monitoring

Conspicuously missing from the list of “key actions” is anything new on regulating overdraft fees at banks and credit unions. Two weeks ago, the agency signaled it would be acting on the fees with the aim, it said, of restoring “meaningful competition.” The bureau also said it would be enhancing its supervisory and enforcement scrutiny of banks that are heavily dependent on overdraft fees. “In recent years, the CFPB ordered TD Bank to pay $122 million in penalties and customer restitution, and ordered TCF Bank to pay $30 million in penalties and restitution,” the agency noted.

LINK:

(Dec. 3, 2021) Action to “restore meaningful competition” to the overdraft fee market was vowed this week by the CFPB, which noted that both small and large financial institutions “heavily rely” on the fees for revenue.

No details of what that action would be, however, were cited by the agency. However, the agency’s press release stated that CFPB will be “enhancing its supervisory and enforcement scrutiny of banks that are heavily dependent on overdraft fees. “In recent years, the CFPB ordered TD Bank to pay $122 million in penalties and customer restitution, and ordered TCF Bank to pay $30 million in penalties and restitution,” the press release recalled, perhaps as an indication of what the bureau has in mind.

Bureau Director Rohit Chopra criticized financial institutions for their reliance on the fees. “Rather than competing on quality service and attractive interest rates, many banks have become hooked on overdraft fees to feed their profit model,” he said.

The bureau reported on research it conducted that asserted banks continue to “rely heavily” on overdraft and non-sufficient funds (NSF) revenue. The bureau said the total revenue collected from those sources in 2019 was $15.47 billion – 44% of which came from customers for the banks JP Morgan Chase, Wells Fargo and Bank of America. Overall, the bureau said, revenue from the fees made up nearly two out of every three dollars generated in fees at the institutions.

“The CFPB also found that while small institutions with overdraft programs charged lower fees on average, consumer outcomes were similar to those found at larger banks,” the bureau stated. “The research also notes that, despite a drop in fees collected, many of the fee harvesting practices persisted during the COVID-19 pandemic.”

Additionally, the agency said, its research shows that aggregate overdraft and NSF fee revenues reported in Call Reports for banks with assets of more than $1 billion saw a small but steady annual increase of around 1.7% per year to $11.97 billion in 2019.

“Reliance on such fees varied considerably among institutions in the Call Reports, but was generally stable over time for any given institution,” the bureau said. “While aggregate overdraft and NSF fee revenues declined by 26.2% in 2020, increased checking account balances resulting from federal stimulus payments likely contributed to this decline.”

LINK

CFPB Research Shows Banks’ Deep Dependence on Overdraft Fees

(July 9, 2021) Consumer complaints about federal student loans fell off during the coronavirus crisis, but protests about overdraft fees on checking accounts surged due to financial institutions attempting to help consumers have access to economic impact payments (EIPs), according to the complaint bulletin issued late last week by CFPB.

The bureau’s bulletin looks at consumer complaints related to three actions taken by Congress in response to the coronavirus crisis. Those were: suspension of monthly payments for federal student loans, issuance of EIPs to eligible households; and promulgation of an interim final rule in support of the Center for Disease Control and Prevention (CDC)’s eviction moratorium.

The bulletin said the key takeaways from the bureau’s analysis of these actions showed:

- Federal student loan complaint volume decreased significantly following suspension of payments; however, borrowers reported issues with customer service and sometimes experienced delays in getting responses to their complaints.

- The customer service issues in student loan complaints raise concerns about servicers’ preparedness for student loan borrowers resuming payments, particularly borrowers who have experienced a decrease in income.

- Renters have submitted few complaints about third-party debt collectors, or attorneys, who are attempting to carry out an eviction; more often, renters described issues with collections for past evictions or expressed concerns about negative credit reporting.

- Consumers reported being charged overdraft fees on their checking accounts when funds advanced by their financial institutions—so consumers could have access to all of their EIP funds—were later reversed.

Regarding the overdraft fees, the bulleting notes that financial institutions – as a courtesy to consumers who had overdrawn deposit accounts – advanced to their members or customers an amount equal to the negative balance so those consumers could reap full advantage of the EIP. However, the bulletin notes, those advances were later reversed, typically 30 days after the advance.

According to the bulletin, a limited number of complaints were received that consumers did not realize that an advance was posted to their account. “Many of these consumers reported learning of the advance only after the funds were debited from their accounts several weeks later,” the bulletin asserts.

“In response to these complaints, several financial institutions reiterated the intention of the advance was so that consumers could make full use of their stimulus payments,” the bulletin states. “In some limited circumstances, financial institutions refunded overdraft fees charged to the consumers’ accounts, stating they were refunding the fees as a courtesy.” A breakdown of what sort of financial institution (credit union, bank or other) refunded the fees was not provided.

LINK:

CFPB Complaint Bulletin: COVID-19 issues described in consumer complaints

(Dec. 18, 2020) In other action at Thursday’s meeting, the NCUA Board issued one final rule and three proposed regulations – with three of those approved on split votes after Board Member Todd Harper (the lone Democrat appointee on the board) voted in opposition all three times.

The board:

- Approved (unanimously), an extension to Dec. 31, 2021 for a temporary final rule that increases the maximum aggregate amount of loan participations that a federally insured credit union (FICU) may purchase from a single originating lender without seeking a waiver from NCUA to the greater of $5 million or 200% of the FICU’s net worth (up from the greater of $500 million or 100% of the FICU’s net worth). The rule had been slated to expire at year’s end. The temporary rule, adopted by the NCUA Board as a relief measure for credit unions in the midst of the coronavirus crisis last spring, took effect April 21.

- Issued a proposed rule (on a 2-1 vote) on field of membership shared facility requirements (under Part 701, Appendix B, of agency rules) that NCUA said is intended to modernize requirements related to service facilities for multiple common bond (MCB) federal credit unions (FCUs). NCUA said the proposal includes any shared branch, shared ATM, or shared electronic facility in the definition of “service facility” for an MCB FCU that participates in a shared branching network. “The FCU need not be an owner of the shared branch network for the shared branch or shared ATM to be a service facility,” the agency said. “These changes would apply to the definition of service facility both for additions of select groups to MCB FCUs and for expansions into underserved areas.” Harper said he questioned the proposal’s ability, without changes, to increase service to underserved areas. The proposal will have a 30-day comment period.

- Released a second proposed rule (on a 2-1 vote), this one on mortgage servicing rights (under Parts 703 and 721 of agency rules), which would amend the agency’s investment regulation to permit FCUs to purchase mortgage servicing rights from other federally insured credit unions subject to certain conditions. Harper called the proposal “half baked,” but said he could find a way to support a final rule if changes were made. The proposal will be issued with a 30-day comment period.

- Advanced yet a third proposed rule – this one on overdraft policy (under Part 701 of NCUA rules) – also on a 2-1 vote. The proposal would remove the requirement that an FCU’s written overdraft policy establish a 45-day time limit for a member to either deposit funds or obtain an approved loan from the FCU to cover each overdraft, and replace it with a requirement that the written policy must establish a specific time limit that is “both reasonable and applicable to all members for a member either to deposit funds or obtain an approved loan from the FCU to cover each overdraft.” In May, the board tabled a proposed interim final rule to let FCUs decide how long members have to resolve account overdrafts. The proposal was tabled after failing to win a second from one of two board members when Chairman Hood asked for it (both members Harper and McWatters expressed opposition to a final rule). Back in May, Harper said the rule would (among other things) allow credit unions to garnish members’ income – including any economic stimulus relief funds – to pay off overdraft debt. Harper reiterated his objections Thursday (“I couldn’t support it then, I can’t now,” he said). Comments are due 30 days after publication in the Federal Register.

The board also set the “normal operating level” for the National Credit Union Share Insurance Fund (NCUSIF) at 1.38 for the coming year, no change from 2020. The NOL represents the target level of reserves in the fund relative to shares insured (referred to as the equity level). Generally, it is the level of reserves the board believes is needed to deal with anticipated losses from credit unions (if any) throughout the year, without lowering the reserving rate below 1.20%, the point at which an insurance premium would be required.

Along those lines, staff told Board Member Harper that it estimates the equity level of the fund at year-end will be 1.32% — well above the level at which a premium would be required. Agreeing with staff that chances of a premium in 2021 now look “next to zero,” Harper said that would be “welcome news to many credit unions.”

LINKS:

Temporary Final Rule, Regulatory Relief in Response to COVID-19

Proposed rule, Field of Membership Shared Facility Requirements

Proposed Rule, Mortgage Servicing Rights

Proposed Rule, Part 701, Overdraft Policy.

Board Briefing, Share Insurance Fund 2021 Normal Operating Level