October 13, 2022 — The Federal Reserve Board and the Consumer Financial Protection Bureau today announced the dollar thresholds used to determine whether certain consumer credit and lease transactions in 2023 are exempt from Regulation Z (Truth in Lending) and Regulation M (Consumer Leasing).

By law, the agencies are required to adjust the thresholds annually based on the annual percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers, known as CPI-W. Transactions at or below the thresholds are subject to the protections of the regulations.

Specifically, based on the annual percentage increase in the CPI-W as of June 1, 2022, Regulation Z and Regulation M generally will apply to consumer credit transactions and consumer leases of $66,400 or less in 2023. However, private education loans and loans secured by real property, such as mortgages, are subject to Regulation Z regardless of the amount of the loan.

Read the Consumer Leasing (Regulation M).

Read the Truth in Lending (Regulation Z).

Questions for the Federal Reserve Board can be directed to Laura Benedict at [email protected] or (202) 452-2955.

Oct. 12, 2022 — New data reveals that nearly half of Americans (46%) are in credit card debt, with the average debt being $6,093. The findings are based on a survey of 1,001 Americans by Anytime Estimate, a unit of Clever Real estate.

The numbers are even more important given a rising rate environment, meaning the cost of that debt is going to grow, and the potential for a recession. The survey found that even two-thirds of those without credit card debt (66%) worry current conditions could soon have them falling behind on card payments.

The Findings

Among the findings:

- Of those in credit card debt, the average Baby Boomer ($8,208) owes more than the average Millennial ($6,182) and Gen Zer ($3,196).

- 76% of respondents have had credit card debt at some point in their lives.

- 1 in 8 Americans have missed a credit card payment in 2022.

- Millennials are four times more likely than Baby Boomers to report missing a payment in 2022 (13% vs. 3%).

- 35% of Americans have missed a credit card payment in the last five years.

- Half of Americans who have missed a credit card payment (50%) did so to afford basic living expenses, such as food, housing, or utilities.

- 80% of Americans with credit card debt are also in some other form of debt.

- Americans rank credit card debt as their most stressful form of debt — above medical debt, mortgage debt, and student loan debt.

- 27% of Americans don’t know their credit card interest rate, and 37% say they’ve opened a new credit card without prior research.

- About 1 in 3 Americans (31%) have had their credit card information stolen.

- The average credit card user spends $1,579 on their cards per month, with about 1 in 8 users (12%) spending over $5,000 per month.

- 1 in 3 Americans couldn’t cover a $2,000 emergency bill

The full analysis can be found here.

Reimbursing cyber scams

As banks are under pressure to compensate their scammed consumers, rising cybercrime rates translate to rising costs for the industry. More than half (58%) of those who conduct their banking online encounter scams via email or SMS at least once per week, and 23% report having fallen victim to a cyberattack.

Banks currently reimburse authorized push payment (APP) fraud at an average rate of 46%. Although many banking institutions are refusing reimbursements for online fraud, this is due to change soon, or else the situation will backfire. For example, measures supported by the UK government will require banks to reimburse everyone. This is only one illustration of the fact that if banks are to secure their consumers and their business line in 2022, they must prioritize cybersecurity more highly.

To exchange efficient strategies, banks will need to collaborate with governments and industry organizations. The public must continue to get education on preventative measures, but ultimately it is the banks’ responsibility to establish security models that will give them and their clients the greatest level of safety.

Maintain compliance with strict privacy regulations

The use of social engineering and account takeover fraud will increase over the next years. Financial institutions must not only conduct comprehensive data checks beyond document verification at account opening to fight this but also keep track of customer identities throughout the customer lifecycle.

Banks must decide how to manage sensitive personal data like biometrics as GDPR and other privacy regulations are being established throughout the world. As a result, many institutions believe that finding a partner that can protect this sensitive personal information is more practical than modernizing internal systems and processes.

Finally, the public is becoming more concerned about how technology corporations utilize personal data. More difficult questions will be raised as a result, and any responses must pass a strict ethical standard. The application of AI to compliance and fraud will need to be explained by banks. Ascertaining whether their partners and vendors have complete control over the technology they provide will also have an impact on vendor onboarding. Every bank will need to be able to justify decisions made to regulators and the broader public.

Leveraging AI to combat cyber fraud

Instead of being a subset of financial crime, banking fraud now coexists with ransomware, phishing, and other types of cybercrime. Fraudsters are functioning methodically, getting more skilled at spotting loopholes in the automated systems that financial institutions are putting in place, and getting better at learning through repetition.

For example, banks and mortgage lenders have started to link more of their fraud charges to the fact that their clients are doing more transactions using mobile banking apps. According to a LexisNexis survey, more than half of the respondents who worked for US banks and credit lenders say that mobile channel fraud has increased by 10% or more this year.

Today’s fraudsters collaborate with criminal gangs that provide crime as a service. As a result, frauds and forgeries become increasingly sophisticated, making them impossible for humans to detect without artificial intelligence (AI) to support their decision-making.

Decentralized currencies are at the center of attacks

Meanwhile, cryptocurrency has become a primary target of cyberattacks. Huge sums of money are frequently present on cryptocurrency exchanges and wallets, making them a powerful attraction for attackers trying to make money from their attacks.

These are sometimes straightforward social engineering attacks, and other times they are far more sophisticated technically. We expect to see more cyberattacks on decentralized currencies given the amount of money that can be stolen in a single successful attack (possibly reaching millions of dollars). For example, in December 2021 criminals stole nearly $200 million from the crypto trading platform Bitmart.

However, we should anticipate law enforcement and governments to become more actively involved in both the investigation of cryptocurrency assaults and the use of cryptocurrency vulnerabilities. For example, government agencies like the Securities Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) may try to regulate cryptocurrencies more strictly as they regulate traditional currencies.

Attacks bypassing MFA

Although multi-factor authentication is a prerequisite for enabling strong customer authentication, the latest attacks against Cisco and Uber have profoundly demonstrated that fraudsters can bypass MFA. Using sophisticated tactics and tools like auto-diallers, criminals have managed to intercept one-time passwords (OTP) and compromise banking accounts. Automating the process and creating what is known as MFA fatigue they force customers to give up OTPs to malicious bots.

OTP interception is now trivial compared to what it has been historically, and that innovation fundamentally shifts the economics in the favor of the attackers. The LexisNexis report highlighted this concern saying that balancing fraud detection with customer friction is a top challenge for banks. Banks need to embrace phishing-resistant MFA methods that eliminate the risk of being defrauded while offering a superb customer experience for all possible use cases and authentication journeys.

A bigger attack surface and higher attack sophistication levels are a result of the rising use of complicated technologies and interaction with third-party systems. Today, maintaining a strong cybersecurity posture entails more than merely defending sensitive systems and data from damaging external attacks. Additionally, it entails better data privacy, identity protection, and vulnerability management. Banks and financial institutions can outsource part of the burden of staying compliant with regulations and securing customer financial data by partnering with a trusted managed services provider. These companies aggregate experience and expertise to help banking institutions stay one step ahead of their adversaries.

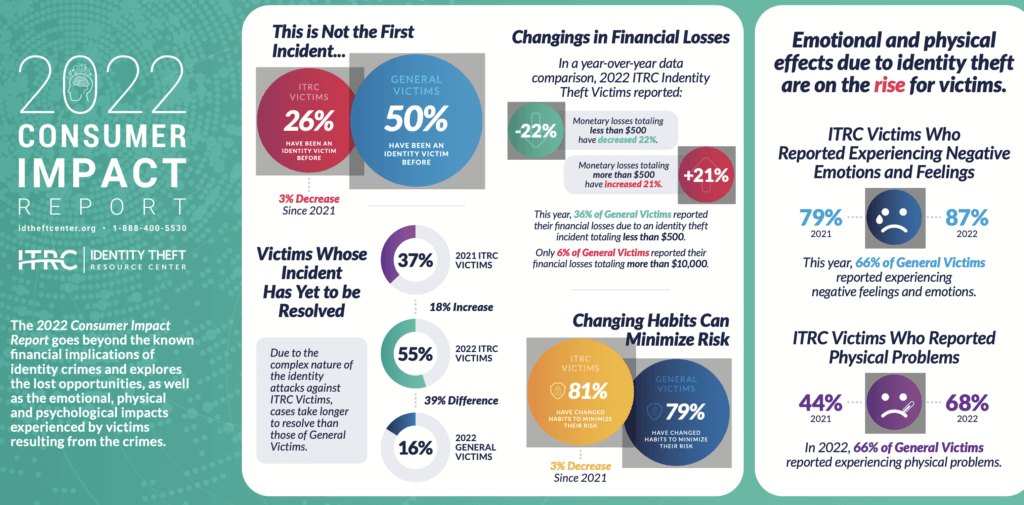

About the ITRC Consumer Impact Report

Since 2003, the ITRC has surveyed the identity crime victims who have contacted the Center to gauge the impact of identity compromises on individuals. Numerous studies by government agencies and private organizations focus on the financial impacts of identity-related crimes. However, the primary purpose of the ITRC Consumer Impact Report is to gauge the emotional, physical and practical effects on the day-to-day lives of victims, including lost opportunities.

This year’s report reflects the responses of 120 victims who contacted the ITRC between April 2021 and March 2022. In the time period covered by this report, new forms of identity attacks emerged. Social media account take-over grew by more than 1,000 percent in just one year. We sought additional input, specifically from victims whose social media accounts were compromised. This survey includes the responses of 97 victims who contacted the ITRC and shows the impacts of the loss of access to a social media account are more significant than first believed.

Previous Consumer Impact Reports dating back to 2003 only reflected the experience of victims who contacted the ITRC. To get a broader view of the trends and impacts affecting consumers in general, this year, the ITRC asked 1,371 consumers in an online survey if they had been the victim of an identity crime and, if so, how it impacted them. Responses from this broader set of self-identified victims using similar questions asked of victims who contacted the ITRC show both significant differences and common experiences.

October 05, 2022 — The Federal Bureau of Investigation (FBI) and CISA have published a joint public service announcement that:

- Assesses malicious cyber activity aiming to compromise election infrastructure is unlikely to result in large-scale disruptions or prevent voting.

- Confirms “the FBI and CISA have no reporting to suggest cyber activity has ever prevented a registered voter from casting a ballot, compromised the integrity of any ballots cast, or affected the accuracy of voter registration information.”

The PSA also describes the extensive safeguards in place to protect election infrastructure and includes recommendations for protecting against election-related cyber threats.

Malicious Cyber Activity Against Election Infrastructure Unlikely to Disrupt or Prevent Voting

![]() The Federal Bureau of Investigation (FBI) and the Cybersecurity and Infrastructure Security Agency (CISA) assess that any attempts by cyber actors to compromise election infrastructure are unlikely to result in large- scale disruptions or prevent voting. As of the date of this report, the FBI and CISA have no reporting to suggest cyber activity has ever prevented a registered voter from casting a ballot, compromised the integrity of any ballots cast, or affected the accuracy of voter registration information. Any attempts tracked by FBI and CISA have remained localized and were blocked or successfully mitigated with minimal or no disruption to election processes.

The Federal Bureau of Investigation (FBI) and the Cybersecurity and Infrastructure Security Agency (CISA) assess that any attempts by cyber actors to compromise election infrastructure are unlikely to result in large- scale disruptions or prevent voting. As of the date of this report, the FBI and CISA have no reporting to suggest cyber activity has ever prevented a registered voter from casting a ballot, compromised the integrity of any ballots cast, or affected the accuracy of voter registration information. Any attempts tracked by FBI and CISA have remained localized and were blocked or successfully mitigated with minimal or no disruption to election processes.

The public should be aware that election officials use a variety of technological, physical, and procedural controls to mitigate the likelihood of malicious cyber activity (e.g., phishing, ransomware, denial of service, or domain spoofing) affecting the confidentiality, integrity, or availability of election infrastructure systems or data that would alter votes or otherwise disrupt or prevent voting. These include failsafe measures, such as provisional ballots and backup pollbooks, and safeguards that protect against voting malfunctions (e.g., logic and accuracy testing, chain of custody procedures, paper ballots, and post-election audits). Given the extensive safeguards in place and distributed nature of election infrastructure, the FBI and CISA continue to assess that attempts to manipulate votes at scale would be difficult to conduct undetected.

The public should be aware that election officials use a variety of technological, physical, and procedural controls to mitigate the likelihood of malicious cyber activity (e.g., phishing, ransomware, denial of service, or domain spoofing) affecting the confidentiality, integrity, or availability of election infrastructure systems or data that would alter votes or otherwise disrupt or prevent voting. These include failsafe measures, such as provisional ballots and backup pollbooks, and safeguards that protect against voting malfunctions (e.g., logic and accuracy testing, chain of custody procedures, paper ballots, and post-election audits). Given the extensive safeguards in place and distributed nature of election infrastructure, the FBI and CISA continue to assess that attempts to manipulate votes at scale would be difficult to conduct undetected.

Election systems that house voter registration information or manage non- voting election processes continue to be a target of interest for malicious threat actors. Cyber actors may also seek to spread or amplify false or exaggerated claims of cybersecurity compromises to election infrastructure; however, these attempts would not prevent voting or the accurate reporting of results.a

The FBI and CISA will continue to quickly respond to any potential threats, provide recommendations to harden election infrastructure, notify stakeholders of threats and intrusion activity, and impose risks and consequences on cyber actors seeking to threaten U.S. elections.

Recommendations

- For information about registering to vote, polling locations, voting by mail, provisional ballot process, and final election results, rely on state and local government election officials.

- Remain alert to election-related schemes which may attempt to impede election administration.

- Be wary of emails or phone calls from unfamiliar email addresses or phone numbers that make suspicious claims about the elections process or of social media posts that appear to spread inconsistent information about election-related incidents or results.

- Do not communicate with unsolicited email senders, open attachments from unknown individuals, or provide personal information via email without confirming the requester’s identity. Be aware that many emails requesting your personal information often appear to be legitimate.

- Verify through multiple, reliable sources any reports about compromises of voter information or voting systems, and consider searching for other reliable sources before sharing such information via social media or other avenues.

- Be cautious with websites not affiliated with local or state government that solicit voting information, like voter registration information. Websites that end in “.gov” or websites you know are affiliated with your state or local election office are usually trustworthy. Be sure to know what your state and local elections office websites are in advance to avoid inadvertently providing your information to nefarious websites or actors.

- Report potential crimes—such as cyber targeting of voting systems—to your local FBI Field Office.

- Report cyber-related incidents on election infrastructure to your local election officials and CISA ([email protected]).

![]() October 4, 2022 — A new report released by Sen. Elizabeth Warren (D-MA) has found reports of scams and fraud on the bank-owned P2P payment network Zelle are surging, but banks have refused to refund customers for most of their losses, even in the face of federal consumer protection law.

October 4, 2022 — A new report released by Sen. Elizabeth Warren (D-MA) has found reports of scams and fraud on the bank-owned P2P payment network Zelle are surging, but banks have refused to refund customers for most of their losses, even in the face of federal consumer protection law.

The report comes at the same time CUToday.info has been reporting on lawsuits filed against financial institutions, including some credit unions, over fraud on the Zelle platform.

The Zelle money transfer system is run by Early Warning, a consortium based in Scottsdale, Ariz., that is owned by seven banks: Bank of America, Capital One, JPMorgan Chase, PNC, Truist, U.S. Bank and Wells Fargo.

Warren said the findings are based on data reported by several of the banks that run the Zelle network, which found the four banks that provided data are on pace to exceed $255 million in fraud on Zelle this year, up from $90 million in 2020, according to the report.

Zelle “is rampant with fraud and theft, and few customers are getting refunded,” said Warren, who sits on the Senate’s Banking Committee.

Acrimonious Hearing

The New York Times noted the report follows a Senate hearing last month that turned acrimonious when Warren pressed the leaders of several large banks about their lack of response to her requests for information about Zelle fraud.

“You didn’t provide any of the information that we requested in our letter, none of it,” Warren said at the hearing. “So, what I want to know is, is that because you don’t keep track when your customers report fraudulent Zelle transactions? Or is it because you do keep track and you know exactly how many fraudulent transactions have been reported, and you want to keep that report a secret?”

Four banks — Bank of America, PNC Bank, U.S. Bank and Truist — provided the data on which Warren’s report was based.

Wide Variations

According to the report, that data revealed wide variations in how the banks addressed fraud claims. PNC refunded only 14% of the 10,683 claims it received about unauthorized Zelle payments, while Truist repaid 82% of its 24,752 claims.

In response to the Warren report, Early Warning responded with a statement that said, “The proportion of fraud and scams has steadily decreased” on its network since its launch in 2017.

In 2021, the company said people sent $490 billion through Zelle (compared with $230 billion through Venmo, its closest rival), a 60% increase from the $307 billion sent in 2020.

Bankers’ Group Responds

Meanwhile, in response to the Warren report, Independent Community Bankers of America President and CEO Rebeca Romero Rainey said,

“ICBA and the nation’s community banks are outraged by increasingly sophisticated fraud perpetrated by criminals against consumers, including those duped into authorizing payments to scammers using Zelle and other peer-to-peer payments services.

“With more than 99.9% of Zelle transactions sent without any report of fraud or scams, community banks appreciate the ability to offer the quick and efficient payments services that customers demand while encouraging Zelle and the largest banks to take measures that improve consumer awareness and protections against fraud. Consumer protection is ingrained in the community bank business model…

“Regulatory restrictions are not the answer to P2P fraud because they will never keep up with the pace of evolving fraud and will serve to disrupt banking services, forcing consumers to look to nonbank money transmission services that operate outside of the banking sector,” Romero Rainey continued. “Further, unlimited liability for P2P fraud under Regulation E would have a disproportionate impact on community banks.

“Instead, policymakers should focus more on the fraudsters and work with P2P technology vendors to maximize consumer awareness of fraud schemes and implement safeguards, such as multifactor authentication, to reduce consumer approvals of fraudulent transactions without delaying consumer access to their funds.”

Article courtesy of CUToday.info

Agency Accepting Comments and Budget Briefing Presentation Requests

Agency Accepting Comments and Budget Briefing Presentation Requests

Sept. 29, 2022 — The National Credit Union Administration’s staff draft budget for 2023–2024 is now available on the agency’s website for review and comment. The staff draft budget has also been submitted for publication in the Federal Register, and the comment period is open until October 28, 2022.

The proposed combined 2023 staff draft budget is $367.0 million, or 8.1 percent higher than the 2022 budget. The proposed operating budget is $350.8 million, which is 9.6 percent higher than in 2022. The proposed 2023 capital budget is $11.2 million, or 14.1 percent lower than in 2022. The proposed Share Insurance Fund administrative budget is $4.9 million, or 21.5 percent lower than in 2022. The proposed budget summary and detailed budget justifications can be found on the Budget and Supplementary Materials page on NCUA.gov.

The agency will hold a public budget briefing at its Central Office on Wednesday, October 19, 2022, beginning at 10 a.m. Eastern. The meeting will be livestreamed on NCUA.gov.

To Comment on the Proposed Budget:

- Submit comments on Docket # NCUA-2022-0145 at the Federal eRulemaking Portal by October 28, 2022.

- Comments should provide specific, actionable recommendations.

To Request an In-Person Presentation at the October 19 Budget Briefing:

- Email your request to [email protected] by October 12, 2022.

- Include the presenter’s name, title, affiliation, mailing address, email address, and telephone number.

- The Board Secretary will notify approved presenters and give them their allotted presentation times.

For those approved to present at the budget briefing, written statements and presentations must be sent to [email protected] by 5 p.m. Eastern on October 14, 2022. In addition to delivering remarks at the budget briefing, registered presenters will have the opportunity to pose questions about the budget to NCUA staff.

The Board will consider a final budget at an open meeting later this year.

Sept. 22, 2022 — As various government agencies and reports use slight inflationary easing to show the economy isn’t in such bad shape, there’s an unescapable chill in the air, and it’s not just winter. It’s the cold reality that living is less affordable than ever.

Sept. 22, 2022 — As various government agencies and reports use slight inflationary easing to show the economy isn’t in such bad shape, there’s an unescapable chill in the air, and it’s not just winter. It’s the cold reality that living is less affordable than ever.

To track these trends, PYMNTS has partnered with LendingClub on the “New Reality Check: the Paycheck-to-Paycheck Report,” an ongoing series tracking how Americans at various income levels and in different demographics are affording — if just barely — the cost of living.

In a conversation with PYMNTS’ Karen Webster, LendingClub CEO Scott Sanborn pushed past recent marginal improvements to Labor Department inflation numbers, pointing to the fact that credit card balances are growing, delinquencies are rising and we don’t have the full picture.

What remains unspoken, he said, “is the way they report delinquencies is on their entire outstanding percentage of delinquent loans on their outstanding portfolio. The thing about credit cards is I think the average age of the balance is between five and seven years. You have this massive amount of balance that’s old, that’s very stable.”

While personal loan delinquencies are not apples to apples as a credit card comparison, he said that “if you look by vintage, the quarterly [credit] delinquencies are fanning like crazy, and none of them are talking about it.”

Portfolio delinquencies may look okay, but that’s a function of time and new balances which haven’t had time to hit issuers yet.

“Just compare the first six months of credit cards issued in Q2 of this year versus the first six months in any of the last 5 to 10 years,” he said. “They look remarkably worse, but nobody’s talking about it.”

See also: NEW DATA: US Consumers Face Emergency Expenses 3.5x Larger Than Fed Estimates

Webster marveled at the fact that the Apple Card is being offered to subprime borrowers with scores as low as 620 to 660 given that backdrop. Sanborn sees that as an unavoidable buy-on terms trap that manufacturers/retailers like Apple are now stuck in.

He said, “As a retailer, the idea that somebody walks into the Apple Store and says, ‘I’d like to buy a new iPad,’ and you say, ‘No, I’m sorry, you can’t have one,’ that’s the business of extending credit. It’s super painful for people who aren’t in the business of credit.”

To keep that machine making sales and not declining brand loyalists, Apple and others are demanding and committing to approval rate minimums from their finance partners — in Apple’s case, Goldman Sachs — some of which end up in that delinquency pile.

‘A Fundamental Misunderstanding’

On the larger issue of perceptions around paycheck-to-paycheck living in America, the most recent New Reality Check study found that 59% of U.S. consumers lived paycheck to paycheck in July, down from 61% in June. However, on the 12-month view, it trended up from 54% in July 2021.

These consumers exist on a continuum of living check to check, from comfortably handling monthly expenses to struggling to meet rising costs, with more now falling behind. Asked why paycheck-to-paycheck consumers are often written off as “poor” or irresponsible, Sanborn sees decades of pile-on effects that erased hard-won benefits like pensions as the real culprit.

“There’s just a fundamental misunderstanding,” he said. “There’s room for interpretation on what does it mean to live paycheck to paycheck? And if what you think of living paycheck to paycheck is you use your paycheck to cover only 100% discretionary items and then you’re out, that is a definition. But the reality is, who’s to determine what’s discretionary?”

Learn more: How Did $1,400 Become the ‘New’ Average Emergency Expense?

Running down the list — transportation, dining, contributing to 401k and HAS plans — he said these could be considered “discretionary” as much as date night, underscoring the confusion.

Here again, Sanborn invoked perception versus reality. Noting that “$370 billion worth of deposits left the system — that’s a record, that is people tapping into their savings,” he said it’s also clear in retail sales trade-downs and rents that are now up 15% year over year.

“Back to this point of being poor and living paycheck to paycheck are not the same thing,” he continued. “Yes, the inflation over the last year has been acute, but over the longer arc of the last 20 years, cost of housing, cost of healthcare, cost of education are all going up exponentially, and over that entire 20-plus-year period, wages have only recently in the last two years started to move.”

Paycheck-to-Paycheck Living Hits Crisis Levels

His underlying point is that perceptions of paycheck-to-paycheck consumers are hopelessly outdated and misaligned with the financial realities of 2022, and even prior years.

Illustrating his point, he said, “If you are able to have a credit card that has a balance, you’re credit worthy. Equating it to whether it’s a lower income [individual] or lower credit quality is not accurate. The data does not support that. Why else would 54% of Americans have credit card debt that they do not pay off? If they had the capacity to pay it off, they would.”

In a move to give struggling consumers options, LendingClub acquired Radius Bancorp in 2021, adding savings accounts to its portfolio in a bid to help consumers boost their financial health.

Sanborn said, “We’re helping them legitimately find savings by offering one of the highest rates possible on the savings account in the country. That’s the commercial aspect. But the human aspect, the broader the policy aspect is we’re all talking about the climate crisis and that’s real. This is also a crisis, and it’s also real, and it is also happening. We have this massive bubble of people heading toward retirement that are not going to be able to afford retirement.”

Conceding that there’s no silver bullet solution, Sanborn believes housing, healthcare and retirement are three major areas deserving public-private action with urgency.

Chairwoman of the House Committee on Financial Services, delivered the following statement at a Subcommittee on National Security, International Development, and Monetary Policy hearing entitled, “Under the Radar: Alternative Payment Systems and the National Security Impacts of Their Growth.”

Thank you very much, Chairman Himes, for convening this hearing on the current and future national security challenges related to the growth of alternative payment systems. These systems can drive inclusion and offer convenience, but because they are generally outside of the western financial system, they also offer opportunities for sanctions evasion and other financial crime.

Further, they rival U.S. dollar-led trade and payments systems, potentially undermining the strength of the dollar and our ability to leverage tools like economic and trade sanctions. So, I look forward to hearing from today’s witnesses on what Congress needs to consider regarding this growing concern.

Research by Boston Fed economist finds borrowers and lenders incentivized to take more risk

Research by Boston Fed economist finds borrowers and lenders incentivized to take more risk

September 15, 2022 — In 2010, researcher Mattia Landoni obtained access to data on thousands of short-term loans known as “repos” that were issued in the three years before the 2007-2008 financial crisis. But like many of his colleagues, Landoni assumed that data on repos would be boring since they were generally thought of as safe. He did not take a closer look at it until 2014, at the urging of fellow researcher Jun Kyung Auh.

He quickly realized he was wrong: Repos were not boring. In fact, the lack of transparency into how they are made or how lenders manage risk has implications that could impact the economy’s fragility, said Landoni, now a senior financial economist at the Federal Reserve Bank of Boston.

“We need to understand what we are seeing here, or we could be just as blindsided by the next financial crisis as we were in 2007,” said Landoni, who works in the Bank’s Supervision, Regulation & Credit department.

Landoni and Auh teamed up on a paper that examines risk-taking associated with repos, “Loan Terms and Collateral: Evidence from the Bilateral Repo Market,” which is forthcoming in The Journal of Finance. The researchers find that repo loans against low-quality collateral are riskier than those against high-quality collateral. But they also find that there are incentives for both lenders and borrowers to continue engaging in these riskier loans.

The researchers said lenders appear to take more risk and receive more compensation when collateral quality is lower, and loans against low-quality collateral are cheaper for borrowers.

Quality, transparency of securities used as collateral varies widely

“Repo” is short for “repurchase agreement,” a short-term, collateral-backed loan. A “bilateral” repo is between two parties. The firm acting as the borrower agrees to sell securities – such as stocks and bonds – to another firm, and then repurchase those same securities at a higher price. The securities act as collateral, meaning the buyer keeps them if the seller breaks the agreement.

But the quality of the collateral varies widely. The researchers observed two main types of securities used as collateral: mortgage-backed securities and collateralized debt obligations.

Landoni said mortgage-backed securities have some degree of transparency because they are backed by real estate loans.

“You can list each mortgage by zip code, so you know exactly what is going into that (security),” he said.

Collateralized debt obligations are backed by a pool of loans and assets, and are, in theory, no more or less risky than mortgage-backed securities. But the researchers found that they are less transparent and more complex, making it harder to assess their value. And, Landoni said, “They were of lower quality, on average.”

Paper: Loans against lower-quality collateral are riskier, but attractive

For their paper, Landoni and Auh created a dataset of more than 13,000 “uncleared” repo loans – meaning they were made directly between two parties. The loans were made between a large hedge fund and major financial institutions from 2004-2007.

The length of the loans spanned one day to six months, and their principal amounts ranged from about $30,000 to more than $700 million, with a median of about $10.5 million.

The researchers analyzed the data and studied the prices of securities being used as collateral. They also created a model to determine what was causing patterns they observed in the dataset.

They found that, despite their higher margins, repo loans against lower-quality collateral were riskier than loans against higher-quality collateral. But both lenders and borrowers had incentives to engage in these riskier loans.

Why? The researchers said it relates to lender optimism and a behavior called “reaching for yield:” Lenders offer a relatively cheaper loan to a borrower with lower-quality collateral in exchange for the chance to take more risk and potentially earn more money.

Since borrowers can get cheaper loans using low-quality collateral, they have an incentive to continue buying it. And that gives the firms that produce securities used as low-quality collateral an incentive to keep creating them.

The researchers said it is critical to continue learning more about this market as the risks lenders take there could have significant impacts on the overall economy.

Landoni said efforts are ongoing to gather more information about the bilateral repo market. He added that he hopes the study helps inform a pilot program in the U.S. Treasury’s Office of Financial Research that is focused on establishing data collection and disclosure protocols.

Courtesy of Amanda Blanco, Federal Reserve Bank of Boston

Sept. 22, 2022 — NCUA held it’s first in-person board meeting since the start of the COVID-19 pandemic. The board thanked the NCUA staff for all of their efforts.

The Board unanimously approved two items:

- A notice of proposed rulemaking, NCUA Part 701, Appendix A, Federal Credit Union Bylaws, Member Expulsion

- A notice of proposed rulemaking, NCUA Part 702, Subordinated Debt

Proposed Rule, NCUA Part 701, Appendix A, Federal Credit union Bylaws, Member Expulsion

- On March 15, 2022, Congress enacted the Credit Union Governance Modernization Act of 2022. Under the statute, NCUA has 18 months following the date of enactment to develop a policy by which a federal credit union (FCU) may be expelled for cause by a two-thirds vote of a quorum of the FCU’s board of directors. The proposed rule would amend the standard FCU bylaws to adopt such a policy. The 18-month period to adopt a final rule enacting a policy on member expulsion ends September 15, 2023.

- NCUA Chairman Todd M. Harper Statement on the Member Expulsion Proposed Rule

Proposed Rule, Part 702, Subordinated Debt

- The proposal would make two changes to the Subordinated Debt rule (Current Rule) related to the maturity of Subordinated Debt Notes and Grandfathered Secondary Capital. Specifically, this proposal would replace the maximum maturity of Notes with a requirement that any credit union seeking to issue Notes with maturities longer than 20 years demonstrate how such instruments would continue to be considered “debt.”

- This proposed rule would also extend the Regulatory Capital treatment of grandfathered secondary capital to the later of 30 years from the date of issuance or January 1, 2052.

- The proposed rule would also make four minor modifications to the Current Rule to make it more user-friendly and flexible. Specifically, the proposal would:

- amend the definition of “Qualified Counsel” to clarify that such person(s) is not required to be licensed to practice law in every jurisdiction that may relate to an issuance.

- amend two sections of the Current Rule to remove the “statement of cash flow” from the Pro Forma Financial Statements requirement and replace it with a requirement for “cash flow projections.”

- revise the section of the Current Rule on filing requirements and inspection of documents.

- the proposal would remove a parenthetical reference related to grandfathered secondary capital that no longer counts as Regulatory Capital.

- Read: NCUA Chairman Todd M. Harper’s Statement on Amendments to the Subordinated Debt Rule

Each proposal will have a 60-day comment period upon publication in the Federal Register.

June 30, 2022: NCUSIF briefing

Read all Board Member statements from this meeting.

- The Board was briefed on the June 30, 2022 – NCUSIF

- The Equity Ratio – as of June 30, 2022, the Equity Ratio remained the same from December 2021 at 1.26%.

- The NCUA projects the NCUSIF equity ratio to reach 1.30 percent for period ending December 31, 2022.

Each board member stressed that while the fund is stable with an increase in the ratio projected, the board must proceed carefully when making any decisions about the share insurance fund due to inflation and increased operating costs. They also stressed the importance of monitoring and managing liquidity issues in the industry due to the significant increase in interest rates.

The board also discussed the expiration of CARES Act relief and the need for Central Liquidity Facility agent membership. The board stressed they will continue to work with Congress.

Ongoing growth in home and auto lending means the industry is gradually shedding the high liquidity levels brought on by pandemic relief programs.

Courtesy of CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

Take Aways

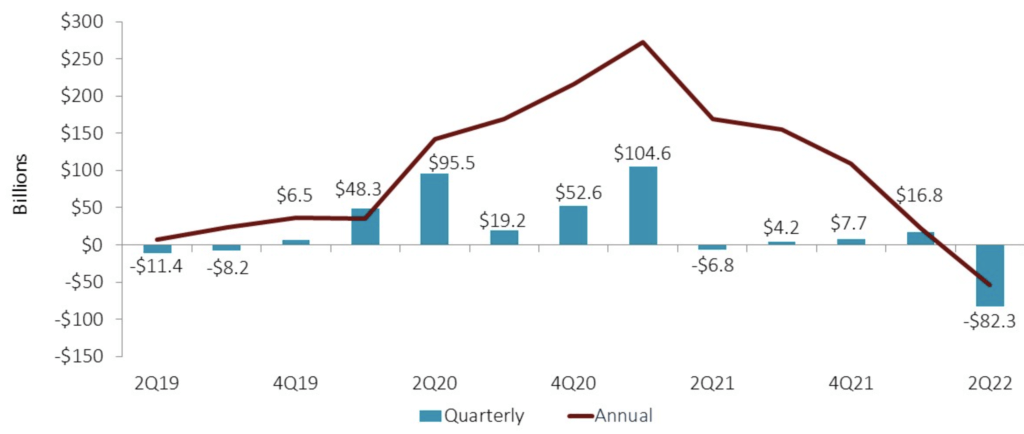

- The federal government took a variety of steps to provide economic relief during the first year of the pandemic, including distributing trillions of dollars directly to consumers. As a result, credit union shares grew at record rates – well outpacing loan growth – leading to sizeable increases in liquidity. However, with the pandemic now mostly in the rearview mirror, credit unions are beginning to unwind the liquidity built up during the crisis. Credit unions reported 6.6% quarterly growth in outstanding loan balances as of 2Q22, well outpacing share growth over the same period, leading to liquidity outflows of $82.3 billion since March. This is a large change from 1Q22, when liquidity moderately increased by $16.8 billion.

- As economic activity expands, this liquidity is being converted from cash into impactful loans. Overall, the dollar value of loans rose by $86.6 billion in the second quarter, increasing total loans by 6.6%. This expansion was driven by credit union members taking out loans for first mortgages (up $26.8 billion this quarter, or 5.36%) and used cars (up $18.4 billion this quarter, or 6.72%). Both growth rates are five-year highs. The loan-to-share ratio has increased from 70.22% in March to 74.73% at the half-year mark.

- Not only is this loan growth helping members purchase homes and cars, it also translates to an impact on earnings for credit unions. As cash balances are converted into loans, credit unions increase earnings off the higher yield. Net interest margin is beginning to tick up, rising 10 basis points from the end of March to 2.67%.

- Rising interest rates make it unclear whether this record loan demand will continue. However, the effects of the economic reopening and federal relief funds on the demand for auto and home financing has certainly led to a repurposing of credit union liquidity.