(Sept. 24, 2021) In yet more action at its Thursday meeting, the NCUA Board approved a state member business lending rule in Oregon for exemption from NCUA’s revised member business lending rule. However, NASCUS noted that the approval highlights concerns for the state system about the 2016 rule that the approval was based on, and the need for future dialogue with the agency about that federal rule.

Under NCUA rules, state-chartered credit unions do not face NCUA examination of compliance with the agency’s member business (commercial lending) rule if the state rule is “no less restrictive” than the NCUA regulation. Oregon had presented its state business rule for consideration and approval by the NCUA Board that the rule complied with the federal regulation.

NASCUS’ Lucy Ito praised Oregon regulators for taking the time and effort to develop a rule that complied with the federal requirements. She also said the state system acknowledges the NCUA Board’s approval of the Oregon rule.

However, Ito said NASCUS has continuing concerns with the NCUA regulation adopted five years ago.

“From the modern inception of NCUA’s MBL (now commercial lending) rule, Part 723 has provided a path for states to implement a divergent, yet sound, rule governing commercial lending,” Ito said. “In the intervening years between 1998 and 2016, several states took advantage of that power—to the betterment of the entire credit union system. And those states did so without detrimental effect on the National Credit Union Share Insurance Fund. Indeed, in finalizing the 2016 rule, NCUA cited no shortcomings or enhanced risk in states that had adopted state-specific MBL rules.”

She noted that, under the previous rule, states both with and without state-specific rules led the way in removing the MBL personal guarantee requirement as a regulatory mandate, permitting loan-to-value (LTV) flexibility, and introducing the concept of viewing MBL through the prism of commercial lending terminology. She asserted that the federal agency emulated states on all these fronts several years after states had evolved these changes.

“In a rule meant to be principles-based, NCUA chose an unnecessarily prescriptive approach to managing the dual-chartering strength of the credit union system,” Ito said. “Rather than focusing on whether a state-specific rule increased risk to the NCUSIF in an unacceptable manner, the ‘no less restrictive’ limitation on state rules instead foreclosed, for practical purposes, the historical avenue by which the regulatory framework for commercial lending was advanced. This was and remains unfortunate,” she said.

The NASCUS leader added that, at a time when the agency is appropriately considering innovative approaches to accommodate digital assets and fintechs, “revisiting innovation in the regulation and supervision of commercial lending would be congruent with NCUA’s laudable future focused posture.”

She said the association looks forward to conferring with NCUA on reconsidering the MBL rule and other regulations “to assure the future vibrancy and health of the credit union system by fostering regulatory diversity and competition between charters and regulators while maintaining safety and soundness.”

LINK:

Oregon Member Business Lending Rule

(Sept. 24, 2021) NASCUS President and CEO Lucy Ito agreed with the NCUA Board for proposing the secondary capital changes to the subordinated debt rule scheduled to take effect at the first of next year. “The state system appreciates the board’s proposal to essentially make subordinated debt more accessible to LICUs,” Ito said. “That will serve to strengthen the use of subordinated debt and reduce burden on LICUs—two goals the state system has been seeking for years.”

Regarding the action on the three rules over the next three months – and particularly expansion of CUSO authorities, Ito noted that NASCUS supports the agency obtaining exam authority over technology service providers (TSPs) that provide services to federally insured credit unions — provided that any such authority requires NCUA to rely on state examinations of such service providers where such authority exists at the state level. Further, she noted, NASCUS supports efforts to strengthen state regulatory exam and supervision of third parties providing services to state-chartered credit unions.

(Clockwise from upper left: NASCUS’ Lucy Ito joins NASCUS Executive Vice President and General Counsel Brian Knight, and NCUA Office of Examination and Insurance Director Myra Toeppe in a discussion of key issues)

(Aug. 20, 2021) The surging Delta variant of the coronavirus is putting a damper on NCUA’s plan to resume on-site operations, including exams, the agency’s top supervisor told the NASCUS S3 conference this week.

According to NCUA Office of Examination and Insurance Director Myra Toeppe, the continued phasing-in of on-site operations depends on the virus variant. She indicated a timetable still needs to be determined. However, the agency is ready (and willing) to go into a credit union whenever it sees a risk to the insurance fund, she said.

“We’ll go in where we need to go in if we see a risk to the insurance fund; we have been clear on that,” Toeppe said during a Tuesday session of the conference. (She was sitting in on the session in place of NCUA Board Chairman Todd Harper, who was unable to attend.) “We do have problem case officers that are doing things. Our regional offices, if we need to be on site, they will get with the (NCUA) executive director to determine from an insurance perspective if we need to go in. We’ve actually had to do some conservatorships during this time. Those are the exception, not the rule.”

But Toeppe emphasized that the agency would move with caution in any event. “People matter,” she said.

The agency’s top examiner also offered a strong defense for NCUA’s call for third-party vendor exam authority. “We do need it,” Toeppe, a former savings and loan regulator, said. “When I first came over to NCUA, I was stunned we didn’t have third-party vendor exam authority. I was used to always having it.” She said her former agency was never accused of abusing the authority, “and it was never a problem.”

Toeppe said NCUA sees reliance “more and more and more” by credit unions on the use of vendors and third parties to help them in a number of areas. She cited data processing and lending as examples.

The agency executive asserted that use of third-party vendors can become a source of risk to the share insurance fund. “And that’s always my focus,” she said. “We want to be sure we aren’t exposing the insurance fund to undue risk. And that’s really where it comes from; it’s a risk perspective for NCUA.”

She added that if the agency secures the authority (which will take an act of Congress to do so), NCUA would use it cautiously. She disputed some reports that the agency would be “ramping up” such as by hiring 500 additional examiners. “I think we’d use (the authority) prudently, where needed, just exactly like the state supervisors have done,” she said. “Where it’s needed, when it’s needed when we see a risk– just like the state supervisors, they’ve used it prudently. The banking regulators use it prudently. I don’t think there would be any difference.

She said that using the authority, when needed, is necessary to avoid a regulatory blind spot. “From (the perspective of) managing the share insurance fund, that makes us very nervous. That’s one thing that keeps me up at night,” she said.

In other comments, Toeppe said:

- Cybersecurity is a persistent threat; the one risk that just doesn’t go away. “We have ebbs and flows of other risks, but cybersecurity just keeps coming,” she said. “It just doesn’t stop, it’s in everything. It’s the constant ‘come at you’ thing. It’s high level, persistent.”

- NCUA is not discouraging mergers among credit unions (as opposed to banking regulators with banks, under an executive order from President Joe Biden). “We don’t tell (credit unions) no you can’t merge, but we want to make sure they are doing the right thing.”

- She has no problem with credit unions buying banks, as long as the transaction is done well and the credit union has done its homework. “Everyone thinks we rubber stamp them,” she said, adding the agency does not. She said the transaction must make sense, and that the agency has be sure of the risk that the insurance fund is taking on with the transaction.

(Aug. 20, 2021) State credit unions are growing their assets and members, spurred to some extent by the financial impact of the COVID-19 pandemic, NASCUS President and CEO Lucy Ito told the opening session of the NASCUS 2021 State System Summit (S3) Tuesday.

Ito’s remarks were among the first at the S3 conference, which assembled a diverse group of more than 115 attendees throughout the country, including state regulators, credit unions, industry partners, and the media. The annual event serves as the state system’s annual conference, and offers a unique opportunity to bring together credit union regulators and practitioners for open dialogue and mutual exchange.

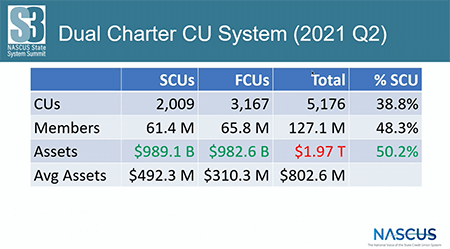

Ito indicated that state credit union asset growth of 21.3% from the end of the first quarter 2020 to end of first quarter 2021 (to $989.1 billion) was astronomical but not surprising, given the influx of savings most financial institutions experienced related to the financial impact of the coronavirus crisis. However, she did say that the membership growth of 3.67% for the period (to 61.4 million) – and decline in the number of state credit unions by just more than 2% (to 1,009) — was typical for the state system.

She noted that the consolidation of credit unions over the last three years, however, has slowed slightly. At year-end 2018, she said, the number of state credit unions dropped by 3.6%; the rate slowed to 2.3% in 2019. Last year, the number dropped at an even slower rate of 2.2%. “Possibly into 2021, consolidation could be slowed a bit in that credit unions may not be pursuing mergers given the other things that they are dealing with,” she said.

Notably, Ito reported, the state system at the end of the first quarter held slightly more than half (50.2%) of all assets in the whole credit union system; memberships were just under the halfway mark, she said, at 48.3%. Overall, two out of every five credit unions (38.8%) are state credit unions. However, state credit unions on average are larger than their federal brethren, at $492.3 million in assets, compared to $310.3 million for FCUs, she pointed out.

On conversions of charters, Ito said over the last 13 years (as of the end of the second quarter of each year), more credit unions (103) with more assets (about $60 billion) have converted from federal to state. She noted, however, that since 2016 when NCUA approved modernization of its field of membership rules for FCUs, that more credit unions have been converting from state to federal (50 conversions to federal charter, versus 40 to states). Those totals include the first two quarters of this year.

However, states continued to gain more assets in the conversions over that time period: $26.4 billion compared to $17 billion for conversions to federal. But that trend may be about to change. So far in 2021, she pointed out, there have been seven conversions, with four of those from state to federal and accounting for $2.4 billion in assets. The three federal to state conversions, she noted, totaled only $328.5 million in assets. “It makes me wonder if this is a turning point in conversions,” she said.

“At this time we have a state and federal system that is basically 50-50,” Ito said. “As we look to the future, factors that will affect future trends (of the share of the market) include continued mergers depending on the size of those and whether or not they change charters; conversions; interstate operations as state borders become less important in people’s lives; and field of membership flexibility.”

She said that, historically, when federal credit unions have converted to states, it is because of the field of membership flexibility that is available in some states, especially the ability to mix and match geographic community fields of membership with associations or with select employee groups.

In other comments, Ito asserted that charter competitiveness within the states will be a key to future growth and success. She noted that parity between credit union charters within states – and even parity between charters of other states (for at least five states: Connecticut, Idaho, Texas, Utah and Washington) or other financial institutions – will play an increasingly large role for states.

“Competitiveness is key; credit unions do need to be able to keep up and compete,” Ito said. “Certainly, as all of us experienced both in our professional and personal lives during the pandemic, just the digitization of our lives accelerated and certainly the pressures on credit unions and other depositories has grown much more intense.”

(Aug. 13, 2021) NASCUS’ Lucy Ito congratulated Harper for the renomination. She noted his experience with credit union issues in both regulatory and legislative areas, and his focus on consumer protections and capital requirements for credit unions. “NASCUS has established a strong rapport with the chairman, which enables both sides to share insights and concerns candidly for the ultimate benefit of a strong dual chartering system,” Ito said. “We look forward to continuing the dialog with Chairman Harper and wish him the best as the confirmation process unfolds.”

(July 23, 2021) NASCUS President and CEO Lucy Ito said the state system welcomes the proposal and that it will carefully analyze it and offer comments. “NASCUS has encouraged NCUA to consider adopting an off-ramp to the RBC rule that has an effect that is similar to the banking agencies’ CBLR,” she said.

The state system had strongly urged the agency to move forward on the CCULR, rather than adopt a proposed risk-based leverage ratio (RBLR) requirement. Ito said NASCUS was pleased the agency dropped the latter approach. “The RBLR approach may have created a perceived conflict with the new subordinated debt rule, by requiring the agency to modify the rule,” she said. “That could have put a damper on credit unions’ attempts to apply subordinated debt toward their capital calculations.”

But the proposed CCULR, she noted, would not require that change – and allow credit unions moving forward on subordinated debt to continue their plans. “The CCULR proposal allows both the 2015 RBC rule and subordinated debt rules to go into effect,” she said. “The optional nature of the CCULR would also permit parallel development of subordinated debt with the simultaneous implementation of the existing 2015 RBC rules, providing credit unions with the choice to opt in and out of the CCULR in the future.”

(May 21, 2021) The development that, at least for now, a premium won’t be necessary to be paid by federally insured credit unions to the NCUSIF is good news for all credit unions, NASCUS President and CEO Lucy Ito said Thursday. However, she cautioned, vigilance is crucial. “Certainly there is more ahead to play out for the economy – but there is no crystal ball on the outcome for any of us. The credit union system, in any event, will have to watch all indicators carefully to determine which way things are going, and even consider some alternative approaches if necessary. Board Member Rodney Hood asked several insightful questions about the insurance fund’s investment powers and strategies – which may spark a conversation about an alternative approach for staving off premiums in the future. In any event: the state system will be part of any conversations about the fund’s finances, and the impact on the state system.”

(April 30, 2021) Issues and policies being pursued by the state system were outlined this week by NASCUS President and CEO Lucy Ito during a presentation hosted by CU*Answers’ “The CUSO Challenge.”

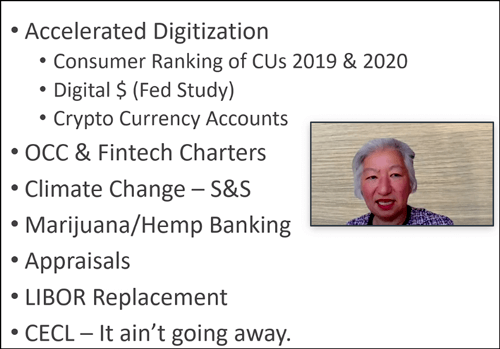

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

In the teleconference, Ito listed key issues being followed by NASCUS as: accelerated digitization among financial institutions (including competition from banks and others working with customers unable to leave their homes during the coronavirus crisis); the rise of new charters (including fintechs), climate change (and its impact on safety and soundness), marijuana and hemp banking (to make it safe for credit unions to serve their members with legal businesses offering those products), and other issues.

Ito also laid out NASCUS’ approach for “renovating” the Federal Credit Union Act, to bring the underlying federal line more in line with contemporary times, and to give the state system (which now represents more than half of the total assets of the entire credit union system) fair representation.

Among other things, Ito recommended separating the insurance function from the supervisory role of NCUA, a long-standing position of the association. NASCUS’ position is that the current structure of the National Credit Union Share Insurance Fund (NCUSIF) presents a potential conflict of interest within the agency unless those functions are internally separated. (NASCUS has also noted that any changes to the statutory structure of the NCUSIF should be evaluated and developed in conjunction with state regulators and credit union stakeholders, since state regulators have experience and expertise with statutory and operational construct of the bank deposit insurance fund that would help inform possible changes to the insurance fund.)

She also noted NASCUS’ support for expanding the NCUA Board from three to five members. In any event, NASCUS also supports reserving one seat on the board for a person with experience as a state credit union regulator.

Other renovations to the FCU Act mentioned by Ito included: updating field of membership, regulatory capital, member business lending and investments authorities, and considering changes to board compensation, annual meeting and member expulsion requirements.

(April 23, 2021) Following the Thursday NCUA Board meeting, NASCUS President and CEO Lucy Ito echoed the comments the association filed earlier this year that the agency should move forward quickly on finalizing the capitalization of interest rule. “As we said in February, we have no doubt credit unions will exercise the ability to capitalize interest to the benefit of their members in need. We are confident in the ability of state examiners to provide supervisory oversight of loan workouts and modifications,” she said. “Modernizing the existing and overly prescriptive limitations related to credit union loan modifications is crucial. When finalized, this rule will benefit both credit unions and economically distressed members – sorely needed relief for both.”

(Feb. 19, 2021) NASCUS President and CEO Lucy Ito commended all three board members for their vigilance in monitoring the insurance fund equity ratio, “especially in light of the root cause for the downward pressure on the ratio: a dramatic and likely continuing increase in insured shares related to economic stimulus payments, and not unsafe or unsound operating practices by credit unions.”

She also agreed with comments by both Vice Chairman Hauptman and Board Member Hood that the agency must proceed carefully regarding a premium, and with Harper about any decisions made about a premium be data driven.

“NASCUS is also intrigued by the suggestion of possible congressional action to expand the investment authority of the insurance fund that would maximize yield while assuring the protection of the fund,” Ito said, noting comments made by Harper during the meeting. “The state system will be studying the statutorily permissible investments by the NCUSIF compared to the FDIC to inform potential legislation.”

(Jan. 29, 2021) On behalf of the state system, NASCUS President and CEO Lucy Ito congratulated new Chairman Harper, noting his experience with credit unions.

“State regulators and credit unions recognize the breadth and depth of his knowledge of the consumer financial services market and his dedication to a robust dual chartering framework that ultimately benefits members of both state and federal credit unions,” Ito said in a press statement. “Working together, we hope to achieve our shared objectives of a safe, sound and strong credit union system that can innovate and grow in the interests of our members.”

The NASCUS leader also extended thanks to former Chairman Hood for working with the state system over the past two years. “We are especially grateful for his support of the 2019 Document of Cooperation between NCUA and NASCUS which provides a durable roadmap for federal-state partnership,” she said.

Finally, Ito said the state system looks forward to working with Vice Chairman Hauptman, who also serves as the NCUA Board liaison to NASCUS, “particularly as both NASCUS and the agency foster collaboration and alignment between state and federal regulators and the whole NCUA Board.”

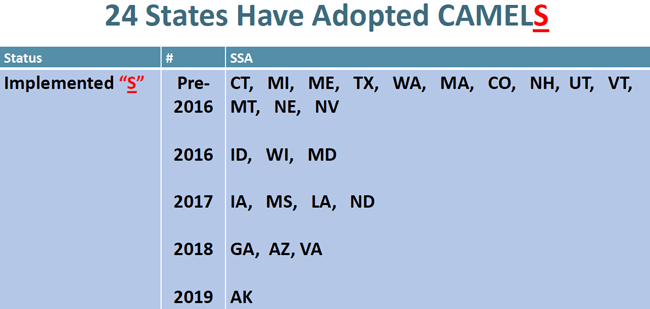

(Jan. 15, 2021) Lucy Ito praised the NCUA Board for moving forward on expansion of the rating system to include the “S” component. “We’re almost at the finish line – but we are willing and able to keep working with the agency to complete the process, and see this change made in time to be effective in 2022,” she said. “The state system is driving toward this goal out of a desire to have consistent standards set across the credit union system, and to reduce risk. For some time, state examiners have observed that the extended low-yield environment may encourage greater risk taking by financial institutions. We urge the agency to finalize this proposal as soon as possible following the comment period and as soon as practicable following necessary technical re-programming.”