The Consumer Financial Protection Bureau is taking heat from banks and credit unions over its proposal to limit increases in credit card late fees that would otherwise increase because of rising inflation.

August 05, 2022 — Banks and credit unions are pushing back hard against an effort by the Consumer Financial Protection Bureau to put a halt to a roughly 9% hike next year in credit card late fees pegged to inflation.

The issue has been moot for years because inflation has been so low. But with the Consumer Price Index up 9% in the past year, the CFPB is calling into question whether credit card late fees should be tied to inflation, a provision set by the Federal Reserve in 2010.

Under the “safe harbor” provision, institutions can raise late fees due to inflation without any cost-benefit analysis as long as the fees being charged are “reasonable and proportional.” To receive the safe harbor, credit card issuers can charge $30 for the first late payment and $41 for subsequent late payments within six billing cycles.

Under a complicated formula, credit card late fees are expected to rise next year to an estimated $33 for the first late payment and $45 for subsequent late payments.

Consumer advocates and critics of the Fed’s safe harbor suggest that the CFPB intervene and put a halt to the inflation adjustments. CFPB Director Rohit Chopra wants to lower credit card late fees generally and has already called out financial institutions for charging consumers roughly $12 billion a year in late fees.

The CFPB received 42 comments to an advance notice of proposed rulemaking in June that seeks to determine how credit card issuers set late fees. A core part of the CFPB’s review involves determining whether late fees are generating more revenue than is necessary to cover their cost, a requirement set by the Fed.

But Chopra also has raised concerns about whether the Fed initially set late fees too high more than a decade ago and whether giving financial firms a safe harbor, with immunity from enforcement actions for setting fees at the safe harbor level, gives issuers an incentive to raise late fees every year.

David Silberman, a former acting CFPB deputy director who is now a lecturer at Harvard Law School, said the bureau should issue an interim final rule to prevent late fees from rising in 2023. Silberman, who is also an adjunct professor at Georgetown University’s McCourt School of Public Policy, said the increases pegged to inflation do not meet the Fed’s own standards.

“There is ample reason to doubt whether a safe harbor which increases with the current cost of living increases meets the reasonable and proportional requirement,” Silberman wrote in a comment letter. “Even if the safe harbor levels were set correctly in 2010 to cover costs and deter violations, there is no basis to presume that the current levels are reasonable and proportional to the violations (i.e. the late or missed payment) that triggers the fee.”

“These late fees are calculated as a business judgment to establish a deterrent effect to mitigate the risk of extending credit,” said Ann Petros, vice president of regulatory affairs at the National Association of Federally-Insured Credit Unions. “The bureau should not second-guess this business judgment or further limit fees across the board by reducing the safe harbor fee amounts.”

Of the 20 largest card issuers, 18 charge late fees at or near the maximum allowed. Many small banks and credit unions charge late fees of $25 or less, though Petros said that credit card payment processors set most fee limits and then pass their costs onto credit unions.

Bankers consider late fees to be a deterrent to consumers piling on debt. (Late fees and interest are charged to cardholders that fail to make the minimum payment by their credit card’s due date.)

Some commenters said the CFPB should look elsewhere for culprits charging excessive fees such as fintechs and buy now/pay later companies.

Others said that reducing late fees or eliminating the safe harbor would cause some level of havoc for the industry, forcing financial institutions to raise fees elsewhere or raise the cost of credit overall, which would impact small banks and credit unions.

“Any reduction in the safe harbor amount or elimination of the safe harbor would have an impact on the thousands of credit card issuers operating in this market, including small issuers,” wrote Paige Pidano Paridon, senior vice president and senior associate general counsel at the Bank Policy Institute.

The CFPB has the authority to regulate late fees under the Truth in Lending Act and Regulation Z, the Card Act’s implementing regulation.

Chi Chi Wu, a staff attorney at the National Consumer Law Center, said credit card late fees should be proportional to the debt owed. She suggested that the CFPB create a sliding scale under the safe harbor so that late fees are proportional to the account balance.

Technology also has lowered the cost of collections, making it easier and cheaper for credit card issuers to use automated methods to collect overdue payments and delinquent debts, Wu said.

Another wrinkle involves minimum credit card payments. Currently, a late fee cannot exceed the minimum amount required. But if late fees go up, issuers also will have to raise the minimum payment floor, Silberman said.

Click here to read the entire article with quotes.

Courtesy of Kate Berry, American Banker

![]() The gains in the amount spent far outpace gains in the number of transactions.

The gains in the amount spent far outpace gains in the number of transactions.

PSCU reported Tuesday that the value of purchases it handles for affiliated credit unions rose much faster than the number of transactions in June, which it said indicated inflation was a growing factor in purchasing growth.

The St. Petersburg, Fla., payments CUSO found members whose credit unions use PSCU services spent 16% more by credit cards in value and 12% more in the number of transactions in June than they did in June 2021. By debit, they spent 7% more by value and 3% more by number.

“While overall consumer spending remained strong throughout June, current inflationary pressures are keeping growth in purchases outpacing growth in transactions,” Brian Scott, PSCU’s chief growth officer, said.

The U.S. Bureau of Labor Statistics reported July 13 that inflation rose a seasonally adjusted 1.3% from May to June, and rose 9.1% from June 2021 to June 2022 — the largest 12-month gain since November 1981.

“With another record Consumer Price Index increase announced this month, the Federal Reserve is under continued significant pressure to tame soaring inflation,” Scott said.

Overall spending by credit union members served through PSCU seemed to trend higher that retail spending among all U.S. consumers.

The U.S. Census Bureau reported July 15 that retail spending — excluding automobiles, auto parts and gasoline — rose 7% from June 2021 to June 2022. The seasonally adjusted increase from May to June was 0.7%.

In particular categories, the 12-month gains reported by PSCU bracketed those reported by Census:

- Grocery spending rose 8.9% from June 2021 to June 2022, according to the Census Bureau. PSCU reported a purchase gain of 15% by credit and 5% by debit. Transactions rose 11% by credit and 2% by debit.

- Gasoline spending rose 49.9%, according to the Census Bureau. PSCU reported purchase gains of 59% by credit and 35% by debit. Transactions rose 15% by credit and 5% by debit.

- Restaurant spending rose 13.7%, according to the Census Bureau. PSCU reported purchase gains of 20% by credit and 6% by debit. Transactions rose 16% by credit and 2% by debit.

PSCU’s July Payments Index found the average credit card balance for June 2022 was $2,733, up 3.5% or $93 from June 2021. June marked the fourth consecutive month in which year-over-year growth was over 2%.

PSCU’s numbers reflected the national pattern for both credit unions and banks. Credit card balances dwindled after COVID-19 was declared a pandemic in March 2020, and had remained below the February 2020 mark for more than two years.

However, balances have been rising this year. The Fed’s G-19 Consumer Credit Report released July 8 showed May balances at both banks and credit unions had finally exceeded their February 2020 levels. NAFCU Chief Economist Curt Long said then that high inflation is one reason he expects credit card balances to grow quickly through the rest of the year.

The credit card delinquency rate for June was 1.54%, 20 basis points lower than pre-pandemic June 2019 levels.

PSCU’s report was based on data from credit unions that have been processing payments with PSCU since January 2020. It encompassed 2.8 billion transactions valued at $140 billion of credit and debit card activity in the 12 months ending June 30.

Courtesy of Jim DuPlessis, Credit Union Times

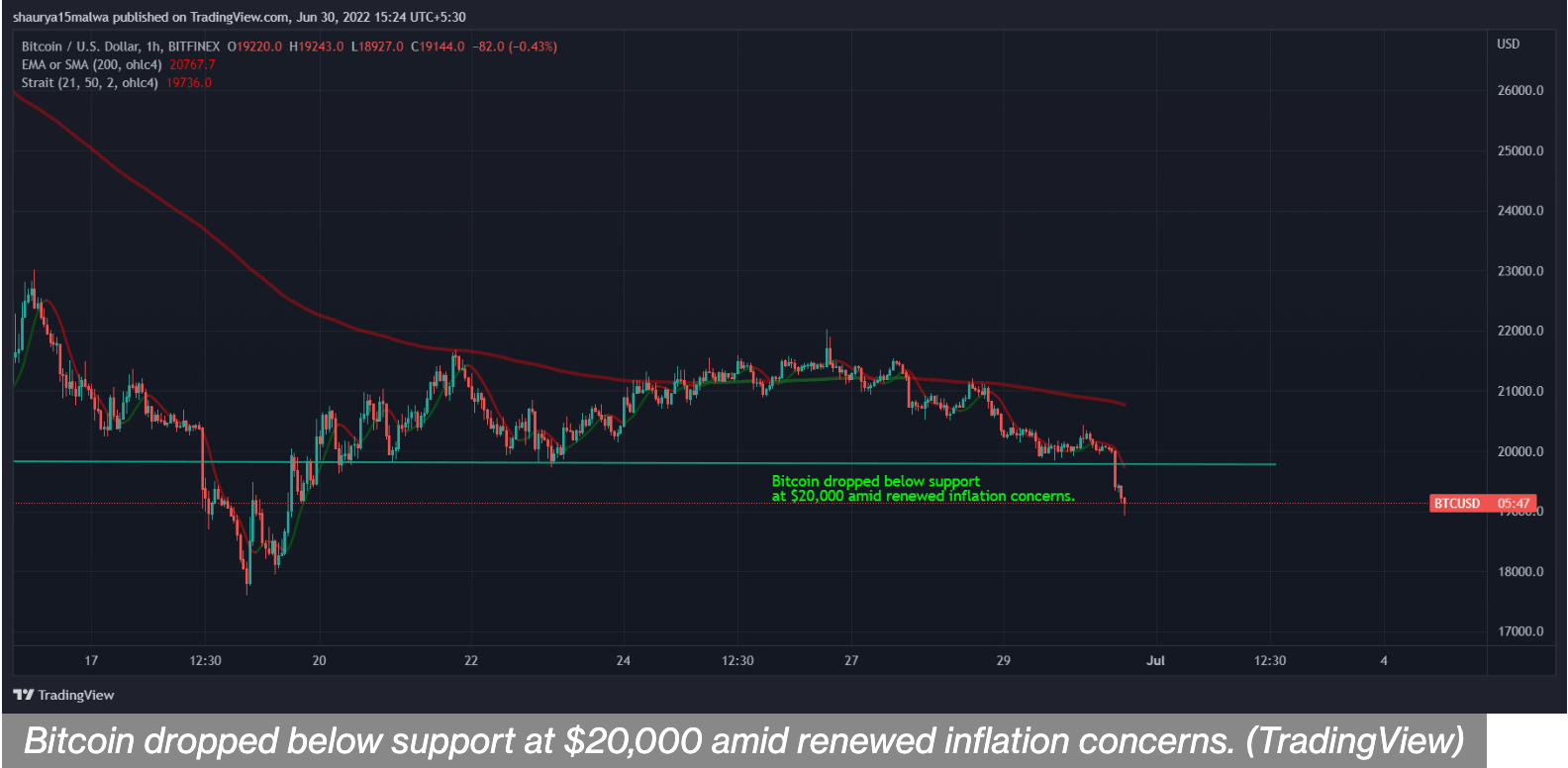

Jun 30, 2022 — Central bank leaders warned Wednesday that inflation is going to last longer than some estimated.

Bitcoin fell toward $19,000 during Asian afternoon hours after central bankers renewed inflation warnings at the European Central Bank’s annual forum on Wednesday.

The asset dropped 5.5% in the past 24 hours, and is on track for a record 40% monthly decline. Other large cryptocurrencies also weakened, with ether dropping 9.9% in the past 24 hours and Solana’s SOL falling as much as 11%. Total cryptocurrency market capitalization fell 4.3%.

Federal Reserve Chairman Jerome Powell reiterated the central bank’s commitment to increasing interest rates to curtail inflation. Speaking at the ECB meeting, he said he was more concerned about the challenge posed by inflation than about the possibility of higher interest rates pushing the U.S. economy into a recession.

“Is there a risk we would go too far? Certainly, there’s a risk,” Powell said. “The bigger mistake to make – let’s put it that way – would be to fail to restore price stability.”

Powell said the Fed had to raise rates rapidly, Reuters reported, adding that a gradual increase could cause consumers to feel that higher prices of commodities would persist. About a week ago, his comments suggested rate hikes could soften before next year.

U.S. equity market futures fell following Powell’s comments, with S&P 500 futures dropping 1.59% and those on the tech-heavy Nasdaq 100 falling 1.9%. Asian markets were in the red with Japan’s Nikkei 225 declining 1.54% and the Asian-focused index Asia Dow falling 1.14%.

Central banks across the globe are weighing interest rate increases amid surging price pressures. Spain reported a 37-year record inflation of 10% earlier this week, while India and China are grappling with the risks of economic contraction.

Such concerns add to already critical selling pressure on bitcoin. The crypto has traded similarly to risky technology stocks in the past few months and has fallen 58% this year.

Contagion risks from within the crypto industry, such as the possible insolvency of crypto lenders and the blowup of prominent crypto fund Three Arrows Capital, have further caused downward pressure on the asset that was otherwise conceived as a potential hedge against inflation.

Michel Euler/Pool via REUTERS

June 1 – Jamie Dimon, Chairman and Chief Executive of JPMorgan Chase & Co described the challenges facing the U.S. economy akin to an “hurricane” down the road and urged the Federal Reserve to take forceful measures to avoid tipping the world’s biggest economy into a recession.

Dimon’s comments come a day after President Joe Biden met with Federal Reserve Chair Jerome Powell to discuss inflation, which is hovering at 40-year highs.

“It’s a hurricane,” Dimon told a banking conference, adding that the current situation is unprecedented. “Right now, it’s kind of sunny, things are doing fine. Everyone thinks the Fed can handle this. That hurricane is right out there down the road coming our way. We just don’t know if it’s a minor one or Superstorm Sandy,” he added.

The Fed is under pressure to decisively make a dent in an inflation rate that is running at more than three times its 2% goal and has caused a jump in the cost of living for Americans. It faces a difficult task in dampening demand enough to curb inflation while not causing a recession.

“The Fed has to meet this now with raising rates and QT (quantitative tightening). In my view, they have to do QT. They do not have a choice because there’s so much liquidity in the system,” Dimon said.

Major central banks, already plotting interest rate hikes in a fight against inflation, are also preparing a common pullback from key financial markets in a first-ever round of global quantitative tightening expected to restrict credit and add stress to an already-slowing world economy.

The inflation battle has become the focal point of Biden’s June agenda amidst his sagging opinion polls and before November’s congressional election.

Uncertainty about the U.S. central bank’s policy move, the war in Ukraine, prolonged supply-chain snarls due to COVID-19 and higher Treasury yields have rocked global stock markets, with the benchmark S&P 500 index (.SPX) falling 13.3% year-to-date.

“You gotta brace yourself. JPMorgan is bracing ourselves, and we’re going to be very conservative in our balance sheet,” Dimon added.

SOFT LANDING?

Wells Fargo & Co’s (WFC.N) CEO warned that the Federal Reserve would find it “extremely difficult” to manage a soft landing of the economy as the central bank seeks to douse the inflation fire with interest rate hikes. The CEO of the fourth-largest U.S. lender also said that Wells Fargo is seeing a direct impact from inflation on consumers’ spending, particularly on fuel and food.

“The scenario of a soft landing is … extremely difficult to achieve in the environment that we’re in today,” Wells Fargo Chief Executive Officer Charlie Scharf said at the conference.

“If there is a short recession, that’s not all that deep… there will be some pain as you go through it, overall, everyone will be just fine coming out of it,” he added.

Scharf said while the overall consumer spending is strong, growth is slowing.

“Corporations are still spending, where they can they’re increasing inventories … we do expect the consumer and ultimately businesses to weaken, which is part of what the Fed is trying to engineer but hopefully in a constructive way,” he added.

Recent Fed reports and surveys reported households on average in a strong financial position, with working families doing well, and unemployment at levels more akin to the boom years of the 1950s and 1960s. Wages for many lower-skilled occupations are rising, and bank accounts, on average, are still flush with cash from coronavirus support programs.

But confidence has waned, and in a recent Reuters/Ipsos poll the economy topped respondents’ list of concerns.

“I don’t think our crystal ball relative to the macro later this year, 2023, 2024 is necessarily any better than others. Clearly, we’re going to see with the Fed actions different impacts in different businesses,” GE CEO Larry Culp, told the conference. Still, not everyone in corporate America is seeing slowdown.

“Of the vast majority of the markets we serve are still quite strong,” Caterpillar Inc CEO Jim Umplebly said.

“And our challenge at the moment, quite frankly, is supply chain, our ability to supply enough equipment to meet all the demand that’s out there,” he added.

(Nov. 19, 2021) Monetary policy, inflation, and cyberattacks could heighten risk to the financial system, according to the annual report issued this week by the Treasury office tasked with conducting financial research.

The report also raised concerns about risks related to low bank profitability, commercial real estate performance and hedge fund strategies.

According to the Office of Financial Research (OFR) annual report to Congress, the economy has rebounded and volatility caused by the pandemic has subsided. However, the other challenges to the financial system mean the overall risks to the financial system remain in the medium range.

According to the OFR press release, the report, highlights three key research findings related to financial system vulnerabilities:

- Macroeconomic uncertainty remains about the continuing impact of the coronavirus and the “pattern of inflation.”

- Cyber risk has grown from mounting economic costs inflicted by cyberattacks and the increasing expense required to guard against them.

- The potential risk from climate change – which has introduced vulnerabilities – is still difficult to identify, assess and forecast for the financial system.

About “sector-specific” risk, the report notes that risks tied to low rates on banks’ profits should be closely monitored. “Higher interest rates on longer-term investments, such as 10-year Treasuries, did not increase net interest margins,” OFR said. “While further research is necessary, possible explanations include lower loan demand and less willingness on the part of banks to lend at longer maturities or take on more deposits.”

LINK:

(April 30, 2021) A two-page fact sheet that lays out what’s behind the demise of the London Interbank Offer Rate (LIBOR), a widely used rate used for such lending products as adjustable rate mortgages, has been published by the New York Fed’s Alternative Rate Reference Committee (ARRC). The fact sheet explains (among other things) LIBOR, the problems it poses, why it is being replaced at the start of next year, and the Fed’s favored replacement for the rate, the Secured Overnight Financing Rate (SOFR). A “part II” of the sheet, available separately (and linked to the first fact sheet) outlines how SOFR will work … Readings on inflation are likely to rise more in the coming weeks before moderating,Federal Reserve Chair Jerome H. (“Jay”) Powell said this week, adding that, ultimately, there will only be a “transitory” effect on inflation. Powell said the rise in inflation indicators will be partially due to supply bottlenecks from a rebound in spending as the economy continues to reopen. Those indicators likely will also be driven by emerging reports of a strengthening economy: Real GDP increased at a seasonally adjusted annual rate of 6.4% during the first quarter of 2021, the federal Bureau of Economic Analysis said this week. In the fourth quarter of last year, real GDP increased 4.3%.

LINK:

Background on USD LIBOR