Courtesy of Tanya Kaushal, YahooFinance

Weed legalization has become increasingly common in the U.S., despite the fact that marijuana is still illegal on a federal level.

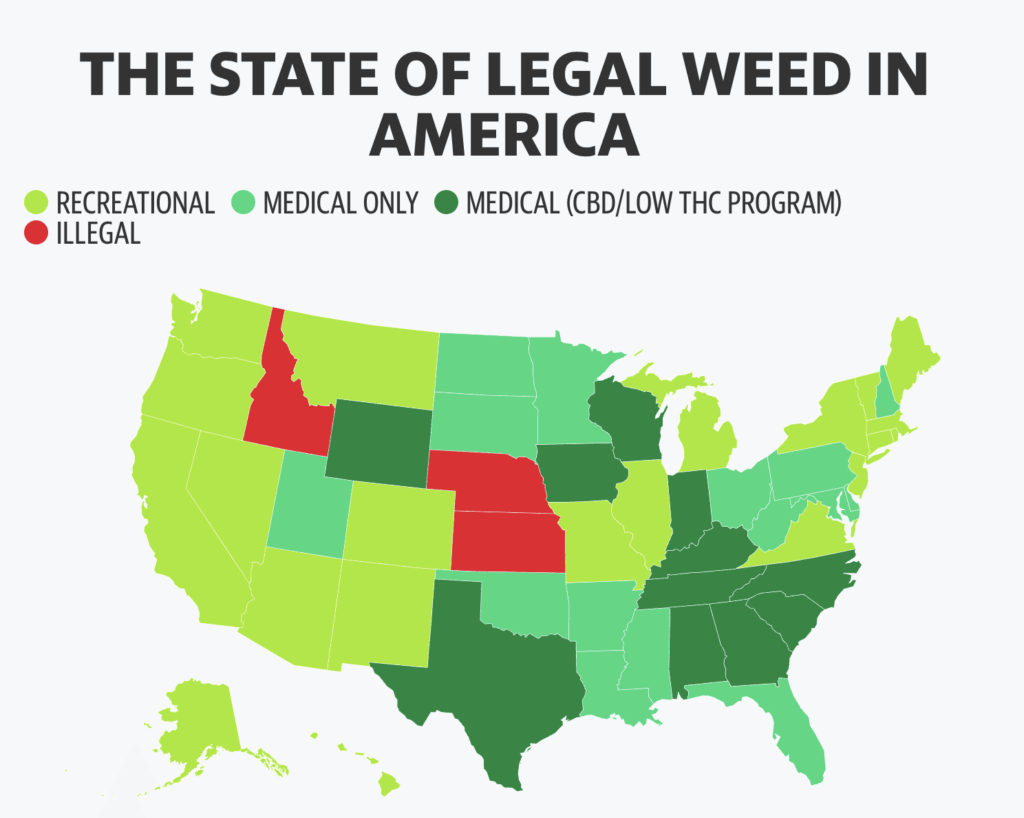

As of April 20, 20 states and the District of Columbia have legalized weed for recreational use while 27 states allow it for varying medicinal purposes. Three states — Idaho, Kansas, and Nebraska — prohibit it entirely.

SOURCE: NATIONAL COUNCIL OF STATE LEGISLATURES

Among the states that have legalized weed to any degree, “none of these states have ever repealed or even rolled back their laws, and public support for these policies has never been higher,” Paul Armentano, deputy director of Norml, a non-profit lobby for cannabis legalization, told Yahoo Finance. “That is because these policies are largely working as politicians and voters intended, and they are preferable to prohibition.”

A strong majority of Americans support the legalization of cannabis. An October 2022 survey from Pew Research found that 59% of adults support legalizing marijuana for both medical and recreational use while 30% support it solely for medical use.

There is clear bipartisan support for legalization: A January 2023 poll conducted by the Coalition for Cannabis Policy, Education and Regulation found that 68% of likely Republican voters support federal cannabis reform.

“It is time for lawmakers, and federal lawmakers in particular, to set aside their ‘canna-bigotry’ and comport the law in a manner that is consistent the available science, majority public opinion, and the plant’s rapidly changing cultural status,” Armentano said.

Armentano added that it is important for cannabis policy to “legalize, regulate, and educate,” which helps reduce the risks associated with cannabis abuse and an unregulated market.

Register today: 2023 Cannabis Banking Symposium

Register today: 2023 Cannabis Banking Symposium

Join us June 27-28, 2023, for our signature cannabis banking event. Network with state and federal regulators, credit union leaders, cannabis experts, and industry stakeholders in a two-day, collaborative deep-dive into the cannabis banking landscape environment.

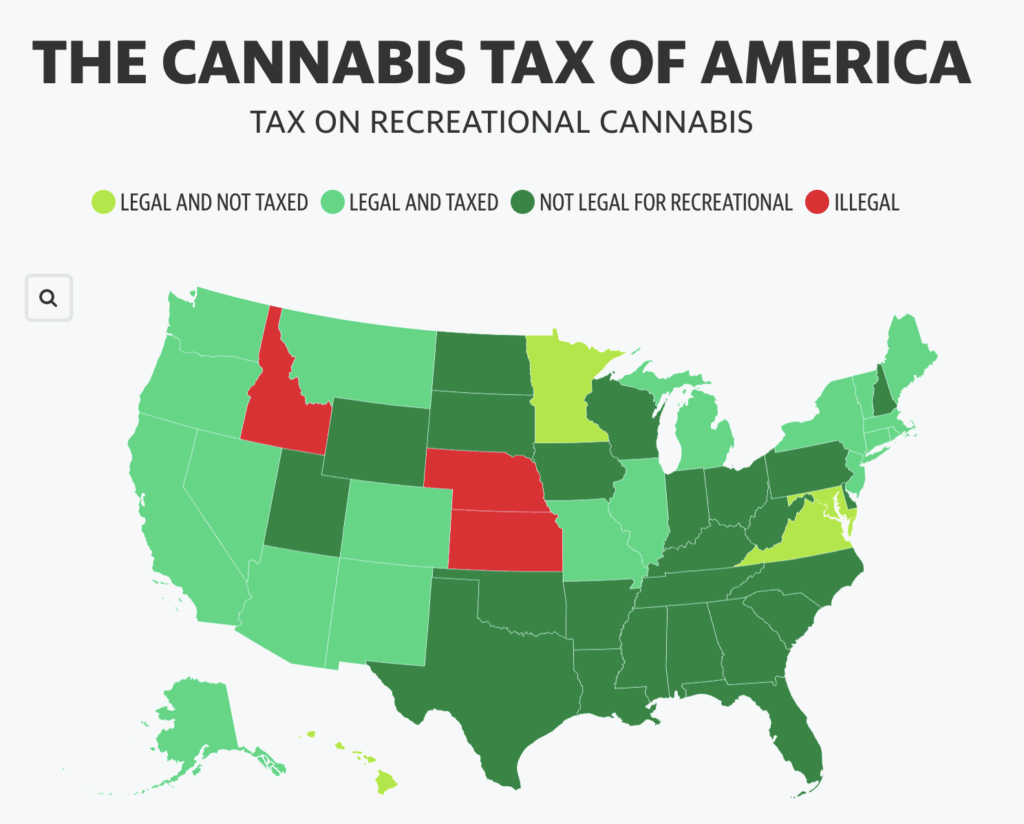

SOURCE: URBAN INSTITUTE • Hawaii, Maryland, and Virginia recently legalized recreational cannabis but taxation hasn’t begun yet.

The cannabis tax

National and global cannabis demand is increasing. It is projected that the U.S. cannabis market could see sales reaching $57 billion to $72 billion by 2030, according to a report from New Frontier Data.

States that have legalized marijuana have used the opportunity to generate revenue.

So far, 19 states levy a “cannabis tax” for the sale of recreational weed. Between July 2021 and June 2022, 11 states collected up to $774 million in state cannabis taxes, the highest being Washington and Colorado on a per capita basis.

“The main lesson we’ve learned so far from state cannabis taxes is that tax design matters,” Adam Hoffer, director of excise tax policy at the Tax Foundation, told Yahoo Finance. “The revenue potential from cannabis taxes is significant. A simple, low-rate, and low-cost tax system has the potential to raise significant amounts of revenue, while simultaneously decreasing social harms from cannabis by bringing illicit market transactions into a legal market framework.”

Hoffer explained that many states have opted for an “ad valorem tax” or a “sales tax based on the transaction price.” This tax relies on the value of the product and typically changes every year, most commonly used for properties. It fluctuates based on market prices.

With a larger cannabis supply chain, if the price falls, tax collection will fall too. Hoffer explained that taxes “based on product weight and potency would have far less volatility.”

There are currently five states — Alaska, Colorado, Maine, Nevada, and New Jersey — that use a weight-based cannabis tax. Aside from New Jersey, which taxes the different parts of the cannabis plant based on potency, the other four states tax the grower directly, according to the Urban Institute.

Still, federal cannabis policy views the drug as illicit, and therefore, the varying taxation in states has resulted in losses for cannabis businesses. Last year, the largest publicly-traded cannabis companies in total lost $550 million.

Today, the Consumer Financial Protection Bureau (CFPB) joined four other federal financial regulatory agencies, along with state bank and state credit union regulators, in issuing a statement that the use of United States Dollar LIBOR (USD LIBOR) panels will end on June 30, 2023.

CFPB issued an Advisory Opinion related to time-barred debts.

The Advisory Opinion affirms that the FDCPA and the Debt Collection Rule prohibit FDCPA-covered debt collectors from suing or threatening to sue to collect a time-barred debt. The Advisory Opinion also affirms that this prohibition may apply to debt collectors that bring state-court mortgage foreclosure actions to collect on time-barred mortgage debt.

You can access the Advisory Opinion here: www.consumerfinance.gov/compliance/advisory-opinion-program/.

CFPB Issues Guidance to Protect Homeowners from Illegal Collection Tactics on Zombie Mortgages

Today, the Consumer Financial Protection Bureau (CFPB) issued guidance on debt collectors, covered by the Fair Debt Collection Practices Act, threatening to foreclose on homes with mortgages past the statute of limitations.

Related Reading: Prepared Remarks of Director Rohit Chopra on Zombie Mortgage Debt

Director Chopra hosted a discussion with local community organizations, advocates, leaders, and members of the public about “zombie” second mortgages and other debt collection issues.

Director Chopra provided remarks on an interagency press conference to announce the Joint Statement on Enforcement Efforts Against Discrimination and Bias in Automated Systems.

Four federal agencies jointly pledged today to uphold America’s commitment to the core principles of fairness, equality, and justice as emerging automated systems, including those sometimes marketed as “artificial intelligence” or “AI,” have become increasingly common in our daily lives.

The FDIC is issuing supervisory guidance to its supervised institutions to ensure that supervised institutions are aware of the consumer compliance risks associated with assessing overdraft fees on a transaction that was authorized against a positive balance but settled against a negative balance (APSN).

The FDIC is issuing supervisory guidance to its supervised institutions to ensure that supervised institutions are aware of the consumer compliance risks associated with assessing overdraft fees on a transaction that was authorized against a positive balance but settled against a negative balance (APSN).

Statement of Applicability: The contents of, and material referenced in, this FIL apply to all FDIC-supervised financial institutions.

Highlights:

- The guidance expands on an FDIC 2019 Supervisory Highlights article titled “Overdraft Programs: Debit Card Holds and Transaction Processing” by discussing the FDIC’s concerns with both the available and ledger balance methods used by institutions when assessing overdraft fees.

- FDIC supervised institutions should be aware of heightened risks of violations of Section 1036(a)(1)(B) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and Section 5 of the Federal Trade Commission (FTC) Act when assessing overdraft-related fees on APSN transactions.

- Unanticipated and unavoidable overdraft fees can cause substantial injury to consumers. Due to the complicated nature of overdraft processing systems and payment system complexities outside the consumer’s control, consumers may be unable to avoid injury.

- Institutions are encouraged to review their practices regarding the charging of overdraft fees on APSN transactions to ensure customers are not charged overdraft fees for transactions consumers may not anticipate or avoid.

- Institutions should ensure overdraft programs provided by third parties are compliant with all applicable laws and regulations.

Related Resources:

- FIL-81-2010: Overdraft Payment Supervisory Guidance

- FIL-40-2022: Supervisory Guidance on Multiple Re-Presentment NSF Fees

Equifax, Experian and TransUnion have removed medical collections debt with an initial reported balance of under $500 from U.S. consumer credit reports, the three credit reporting agencies said Tuesday (April 11) in a joint press release.

“We understand that medical debt is generally not taken on voluntarily and we are committed to continuously evolving credit reporting to support greater and responsible access to credit and mainstream financial services,” Equifax CEO Mark W. Begor, Experian CEO Brian Cassin and TransUnion CEO Chris Cartwright said in the release. “We believe that the removal of medical collection debt with an initial reported balance of under $500 from U.S. consumer credit reports will have a positive impact on people’s personal and financial well-being.”

This is the latest change made as part of a commitment announced by the three credit reporting agencies in March 2022.

In two changes that took effect July 1, 2022, paid medical debt is no longer included on consumer credit reports, and consumers are given a year — rather than the previous limit of six months — to address unpaid medical debt before it appears on their report.

With the most recent change — which the agencies had said would take effect in the first half of this year — nearly 70% of the total medical collection debt tradelines reported to the agencies have been removed from consumer files, according to the Tuesday press release.

The effort by the credit reporting firms to change how they report outstanding medical liabilities was undertaken in March 2022 in part to satisfy the Consumer Financial Protection Bureau (CFPB).

CFPB Director Rohit Chopra said earlier in March 2022 that he would hold credit reporting agencies accountable for dragging their feet on acting against companies that report inaccurate medical debt.

The CFPB reported in February that medical collection tradelines are still a majority of all collections on consumers’ credit reports — at 57%. And that’s even with the fact that, as the CFPB said, debt collectors “are moving away” from reporting (or furnishing) medical bills to credit reporting companies.

Courtesy of PYMNTS.com

Courtesy of Anna Hrushka, Banking Dive

Atlanta-based Greenlight is making its kid-focused banking services available to traditional financial institutions, the fintech announced on Wednesday.

The new partnership program, called Greenlight for Banks, allows banks and credit unions to offer the fintech’s suite of banking and education products to their customers through a co-branded landing page and app.

Over half a dozen firms, including Morgan Stanley, WaFd Bank and Community Financial Credit Union have partnered with Greenlight to offer the fintech’s services to their customers, Matt Wolf, Greenlight’s senior vice president of business development said.

Greenlight is actively involved in discussions with over 100 financial institutions, he added.

“In those conversations with financial institutions, we found that many don’t have the expertise or resources to create a compelling digital banking experience for the next generation,” Wolf said. “We’ve designed something that really helps financial institutions, seamlessly integrate family banking into their own ecosystems.”

Greenlight, which was co-founded by Tim Sheehan and Johnson Cook, launched a debit card for kids in 2017.

The fintech has since expanded its offerings to include savings and investing for children, while allowing parents to automate allowances and supervise their dependents’ money management.

In January, Greenlight launched a financial literacy game called Level Up, which banks and credit unions will also be able to make available to their own customers through Greenlight for Banks.

Lenders who partner with Greenlight have the option to hold the deposits gathered by the fintech, or allow them to be held by Greenlight’s partner bank, Community Federal Savings Bank, which issues the Greenlight debit card.

While banks are eager to launch products that reach the next generation of customers, bank accounts geared toward children typically don’t have high balances, meaning, they won’t be large deposit generators for banks, Wolf said.

“A couple transactions a month is probably not going to really rise to the top of their technology roadmap and prioritization,” Wolf said.

But offering services targeted toward kids and their parents allows a bank or credit union to create deep and potentially long-lasting relationships, Wolf added.