(Nov. 12, 2021) A summary of NCUA’s new rule on federal credit union service organizations (CUSOs) – adopted Oct. 21 by the NCUA Board on a 2-1 vote – has been published by NASCUS; it is available to members only.

The final rule gives CUSOs owned by FCUs the power to originate any type of loan an FCU may originate – and give the NCUA Board more flexibility in approving permissible CUSO activities and services. It becomes effective Nov. 26. Board Chairman Todd Harper voted against finalizing the rule.

By allowing FCU-owned CUSOs to originate any type of loan an FCU can, the list of permissible loans by FCU CUSOs is expanded from only business loans, consumer mortgage loans, student loans, and credit cards. The list of new loans includes automobile and small-dollar (payday) loans – the two types NCUA has said would likely draw the newest involvement by CUSOs.

In its comment filed on the proposal last spring, NASCUS noted as a key concern with the proposal that possible, additional reporting requirements for state credit unions could be a result of a finalized rule. NASCUS noted that the proposal could influence state credit unions considering collaborating with FCU investors in the formation and ownership of a CUSO – a condition that prompted the association to comment.

In some states, NASCUS pointed out, CUSOs owned by state credit unions already hold expanded lending power. The association noted, however, that the NCUA proposal could end up requiring additional reporting requirements that don’t today exist for SCUs. “NASCUS opposes extension of any additional reporting requirements to SCU CUSOs resulting from an expansion of FCU powers,” the association wrote.

Following the rule’s adoption last month, NASCUS President and CEO Lucy Ito said the association views the final rule as a “natural evolution” in a robust dual charter system. However, she noted the additional reporting requirements and added that the state system will review the final rule closely and work with NCUA to resolve any unintended, negative impacts on state credit union CUSOs.

LINK:

NASCUS Final Rule Summary: FCU CUSOs (Parts 712) (members only)

(Nov. 12, 2021) Any issuances of secondary capital not completed by Jan. 1 will be subject to the requirements of the new subordinated debt rule, which becomes effective on that date, according to a letter published late last week by NCUA.

NASCUS has published a summary of the letter, which like all summaries from NASCUS, is available to members only.

The NCUA letter to credit unions ((LTCU 21-CU-13) states there is one potential exception: low-income designated credit unions are allowed to issue secondary capital approved in 2021, irrespective of the date of issuance, under a proposed rule issued by the agency in September. A final version of the rule, the letter stated, will be considered by the NCUA Board by Jan. 1.

The subordinated debt rule was approved by the NCUA Board nearly a year ago (in December 2020), with an effective date of the beginning of the new year. That rule allows well-capitalized, low-income designated, federally insured credit unions to count subordinated debt as capital for risk-based net worth purposes.

The proposal issued in September would amend that rule, slightly, by accommodating low-income credit union (LICU) access to federal investment programs, most notably the Treasury Department’s Emergency Capital Investment Program (ECIP). That program directs Treasury to make investments in “eligible institutions” to financially support small businesses and consumers in low-income and underserved communities. Those institutions include federally insured credit unions that are minority depository institutions (MDIs) or community development financial institutions (CDFIs) that are in sound financial condition. The investments are made in the form of subordinated debt.

Funding of secondary capital approved under the current rule would be permitted under the proposal beyond 2021, without the need to reapply under the subordinated debt rule – thus giving those credit unions a measure of regulatory relief.

“Given the current 45-day review period for secondary capital plans, any low-income credit union still planning to submit a secondary capital plan should do so as soon as possible,” the NCUA letter states. “Further, if a low-income designated credit union plans to submit a secondary capital plan this year, it should consider using the application requirements in section 702.408 of the final subordinated debt rule when drafting its plan and submitting an application.

“This can help avoid having to resubmit documentation as long as the application meets the requirements of the final rule,” NCUA wrote.

LINKS:

NCUA LTCU 21-CU-13: Subordinated Debt Final Rule Effective January 1, 2022

(Nov. 12, 2021) NCUA late last week placed the tiny Pomona Postal FCU of Pomona, Calif., into conservatorship, saying the credit union’s most recent call report shows it had 717 members and $4.2 million in assets. The 57-year-old credit union had about a 51% loan-to-share ratio, according to NCUA data … Bob Gallman, president and CEO of the Louisiana Credit Union League since 2017, has announced his retirement, effective next March; he has notched more than 45 years in the credit union system … Guidance for dealing with climate change risk management “supervisory expectations” will be released this year, the acting comptroller of the currency said this week. “We expect to issue framework guidance by the end of this year, to be followed next year with detailed guidance for each risk area,” Acting Comptroller Michael J. Hsu said. “The detailed guidance will build on a range-of-practices review that will launch this week, industry and climate groups’ input, and lessons from other jurisdictions” … Providing “relevant and timely information” specifically for examiners and financial institution practitioners is the aim of a revamped notification system announced this week by the FFIEC (which, since April, has been chaired by NCUA Chairman Todd Harper). According to the Exam Council, its “FFIEC Announcements” email notifications will be distributed to the council’s email subscribers notifying them of updates to its website and “Infobases.” Each issuance, the council said, will be designated with the word “Announcement” in the header, followed by a sequential numbering order of a four-digit year and a two-digit issuance number. See the link for more or to sign up.

LINKS:

NCUA Places Pomona Postal Federal Credit Union Into Conservatorship

Acting Comptroller Discusses Climate Change Risk

FFIEC Implements New “Announcements” Communication Tool

(Nov. 12, 2021) Growing use of anonymity-enhanced cryptocurrencies (AECs) used in ransomware schemes and the ways that perpetrators launder ransomware proceeds are detailed in an updated advisory issued this week by Treasury’s financial crimes enforcement unit.

The updated “Advisory on Ransomware and the Use of the Financial System to Facilitate Ransom Payments” from the Financial Crimes Enforcement Network (FinCEN) reflects information from the agency’s Oct. 15 Financial Trend Analysis Report. The advisory, part of Treasury’s effort to combat ransomware, addresses the role of financial intermediaries in ransomware schemes, trends and typologies of ransomware and associated payments, recent examples of ransomware attacks, and financial “red flag” indicators of such activity.

Noted “trends and typologies,” according to the advisory, include: extortion schemes, the proliferating use of anonymity-enhanced cryptocurrencies (AECs); use of unregistered convertible virtual currency (CVC) “mixing” services (mixing is a mechanism used to launder ransomware proceeds, FinCEN notes); cashing out through foreign CVC exchanges; collaboration and partnerships among ransomware criminals; and more.

A description of 12 financial red-flag indicators of ransomware-related illicit activity is included to assist financial institutions in detecting, preventing, and reporting suspicious transactions associated with ransomware attacks. “As no single financial red flag indicator is indicative of illicit or suspicious activity, financial institutions should consider the relevant facts and circumstances of each transaction, in keeping with their risk-based approach to compliance,” FinCEN said. (See the complete report, linked below, for all 12 red flags.)

LINK:

FinCEN advisory on Ransomware and the Use of the Financial System to Facilitate Ransom Payments

(Nov. 12, 2021) A final rule on field of membership (FOM) shared facility requirements will be at least one of the items on the Nov. 18 NCUA Board meeting agenda, released this week.

The board will also receive three board briefings from staff – including one on the agency’s modernized examination tools – and consider the agency’s 2022-26 strategic plan

The board meeting is scheduled to begin at 10 a.m. Thursday at NCUA headquarters in Alexandria, Va.; it will be live-streamed via the Internet.

The final rule, as proposed nearly a year ago (in December 2020), would “modernize” requirements related to service facilities for multiple-common-bond federal credit unions (FCUs).

The proposal – which modifies Part 701, Appendix B, of NCUA regulations — would, the agency said, include any shared branch, shared ATM, or shared electronic facility in the definition of “service facility” for a multiple-common-bond FCU that participates in a shared branching network.“

According to NCUA, the FCU need not be an owner of the shared branch network for the shared branch or shared ATM to be a service facility. “These changes would apply to the definition of service facility both for additions of select groups to MCB FCUs and for expansions into underserved areas.”

The proposal was issued for comment on a 2-1 vote, with now-Board Chairman Todd Harper dissenting. Harper said he questioned the proposal’s ability, without changes, to increase service to underserved areas.

The shared service proposal is one of two outstanding proposals the board agreed in September to consider in upcoming meetings in November and December. Next month, the board will consider a proposal on mortgage servicing rights, which Harper also opposed.

The future of unanimous approval for both the FOM and mortgage servicing proposals may be a bit brighter, however: Harper said at last month’s NCUA Board meeting that he hoped to be able to support both in the upcoming votes.

Regarding the modernized exam tools: the agency is rolling out new implements for evaluating credit unions. Those include the agency’s Modern Examination & Risk Identification Tool, (MERIT), as well as associated programs: the Data Exchange Application (DEXA), NCUA Connect, and the Admin Portal.

The other two briefing will be a quarterly report on the National Credit Union Share Insurance Fund (NCUSIF) and an update on the agency’s response to the COVID-19 pandemic.

LINK:

Agenda, NCUA Board Nov. 18 meeting

Two big opportunities are and will be available to you for learning more about NASCUS and the value it offers to the state system:

- A recording is now available of a demonstration webinar of CU Campus 365, held this week. CU Campus 365 is an online compliance training and professional skills learning platform for credit unions. Powered by BAI, the nation’s leader in training and research for financial institutions, CU Campus 365 provides access to more than 500 credit union compliance training courses and more than 150 professional-skills courses. The 30-minute webinar includes a high-level overview of how credit union supervisors and practitioners can leverage CU Campus 365. The webinar also describes CU Campus 365’s library of documents about various relevant policies that training managers need to meet examiner and management requirements. To find out more, see the link below.

- Hold Dec. 9, 2 p.m. ET, on your calendar for the next NASCUS 101, a free, short webinar where you can learn from the NASCUS team how to make the most of a NASCUS membership. Among the topics addressed: What NASCUS is, how NASCUS contributes to the entire credit union industry, how to engage in the regulatory and legislative processes, collaboration with peers, committee and working group involvement, customized communications and more. The webinar is open to all members and prospective members. To register, see the link below.

LINKS:

CU Campus 365 Information form

Register here for NASCUS 101, Dec. 9, 2 p.m. ET.

(Nov. 12, 2021) A bipartisan group of 24 governors and other top officials called on the Congress this week to include the SAFE Banking Act – legislation supported by the state system to provide clarity to financial institutions seeking to serve legitimate cannabis businesses – as an amendment to the military funding bill now pending in Congress.

The governors, territorial leaders and the mayor of the District of Columbia – 20 Democrats and four Republicans – said the SAFE Banking Act has “more bipartisan support than ever before.”

The legislation has passed the House but has not been taken up in the Senate. It would provide a safe harbor for credit unions and banks serving cannabis businesses in states where it is legal. More than 35 states have legalized cannabis for medical or adult use. However, federal law prohibits credit unions and banks from safely banking cannabis businesses, including those that provide them with goods and services.

The state and territorial leaders argued that the bill should be added to the National Defense Authorization Act (NDAA), must-pass legislation by year’s end to essentially keep the military funded. The House has added the provision to its version of the NDAA; the Senate has not yet acted. The state leaders wrote that the issue was one of public safety.

“Medical and recreational cannabis sales in the U.S. were estimated to total $17.5 billion last year, but because of antiquated federal banking regulations, almost all cannabis transactions are cash-based,” the leaders wrote. “Not only are cash-only businesses targets for crime, cannabis businesses are further disadvantaged compared to other legal businesses by being unable to open bank accounts or obtain loans at reasonable rates. The cannabis industry is legal in some form in the majority of U.S. states and it is too large of a market to be prohibited from banking opportunities.”

LINK:

(Nov. 12, 2021) There will soon be two open seats on the Federal Reserve Board – and maybe three as early as January – because of the announced resignation of the former vice chair for supervision on the board, in what could be some big changes ahead for the central bank’s leadership.

Randal K. Quarles – the first and so far only vice chair of the Federal Reserve Board for supervision – announced his retirement from the agency board Monday, effective in late December. In a letter to President Joe Biden (D), Quarles said after four years as a member of the central bank’s board, and end of his term last month as vice chair of supervision, it was time for him to leave.

“It has been a great privilege to work with my colleagues on the Board, throughout the Federal Reserve System, and among the global central banking and regulatory committee,” Quarles wrote.

Quarles’ resignation will leave two open seats on the Fed Board; no successor has yet been named to him as top supervisor for the agency and the White House has made no nominations to fill the soon-to-be two open board seats.

There could be a third opening on the board within two months: the term of Fed Vice Chair Richard Clarida expires in January (and, likewise, the White House has been mum on a replacement).

And, there remains the question of who will lead the central bank board for the lion’s share of 2022 and beyond: the term of Jerome H. (“Jay”) Powell as chair of the board expires in February. He may continue to serve on the board after that, since his term as a governor runs until January 2028.

Quarles’ four-year term as vice chair for supervision ended last month. He now serves as chairman of the international Financial Stability Board (FSB), which works to coordinate financial stability regulatory programs across the globe. However, the term for that office ends at year’s end.

A former banker, Wall Street lawyer and Treasury Department official, the 64-year-old Quarles was nominated to the position by President Donald Trump (R) in September, 2017; he joined the board in October. His current term was to run until 2032.

LINK:

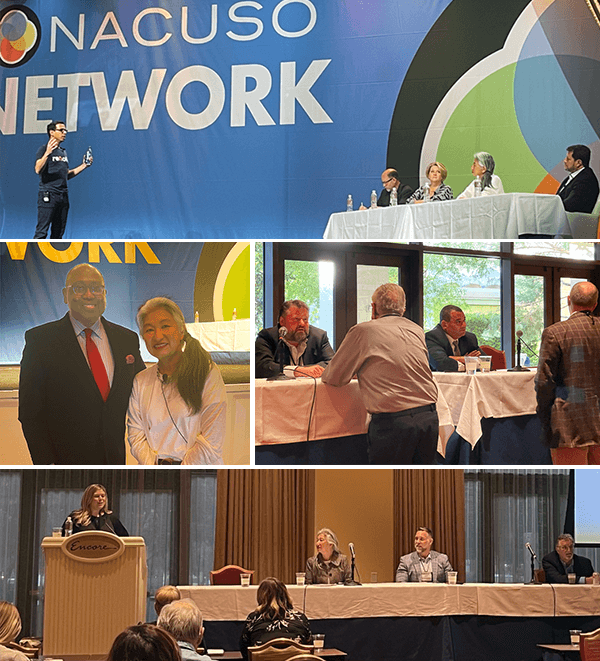

(Clockwise from top) NASCUS’s Lucy Ito (second from right) joins other judges in the “Next Big Idea” competition in listening to a presenter’s big idea. Other judges are (from left) Bill Beardsley, president of Michigan Business Connection; Becky Reed, CEO, Lone Star Credit Union; Steve Salzer, SVP enterprise risk office and general counsel at PSCU … NASCUS’s John Kolhoff (left) and Brian Knight answer questions from session participants following their presentation … Liz Winninger, President & CEO of Xtend, moderates a panel discussing “Think tanks: Why credit unions need more of them” with Ito; Chris Harper, senior director of membership at Filene; and Vic Pantea of Variable Ventures. NCUA Board Member Rodney Hood and NASCUS’s Ito take time out at the conference.

(Nov. 12, 2021) NASCUS was a prominent participant in national conference for CUSOs held this week in Las Vegas, Nev., taking roles in conferences, breakout sessions and the annual “next big idea” competition for innovative ideas that benefit service organization offerings to credit unions.

The 2021 NACUSO Network Conference, held throughout the week, looked at a variety of subjects of interest to the state credit union system. Among the NASCUS’s participation was:

- A session on credit union share insurance and how CUSOs can create more options for credit unions featured NASCUS Regulator Board Secretary/Treasurer John Kolhoff (commissioner of the Texas Credit Union Department) and association Executive Vice President and General Counsel Brian Knight. Among other things, Knight and Kolhoff discussed the importance of the strength of the dual chartering system. Knight made note of the Dual Charter Resource Initiative (DCRI), a partnership between NASCUS and credit union system organizations designed to update existing resources, and produce new ones, that support strengthening of the state charter. The pair also discussed how NASCUS is working with NACUSO and CU*Answers in support of the “CUSO Challenge,” a five-part program aimed at supporting CUSOs. Among other things, the initiative is working to facilitate de novo credit unions, enhance CUSO effectiveness in regulatory and legislative representation, study alternatives to deposit insurance, develop a scholarship fund, and gather ideas for CUSO development.

- NASCUS President and CEO Lucy Ito served as one of the judges to select the winner for the 2021 “Next Big Idea” competition, sponsored annually by NACUSO to identify innovative idea for credit union service organizations. The winner selected by the audience and the panel was RenoFi, a firm that offers home renovation loans that provide financing for up to 90% of the after-renovation value of the property. Noting that RenoFi will present its innovation at the NASCUS 2022 State System Summit (S3) next summer, Ito congratulated the winner. “Consumers have many loan options from their credit unions for other life events, but this innovation fills a long-time need. Thanks also to NACUSO for bringing this innovation – and those of the other four finalists – to the state system’s attention.”

LINKS: