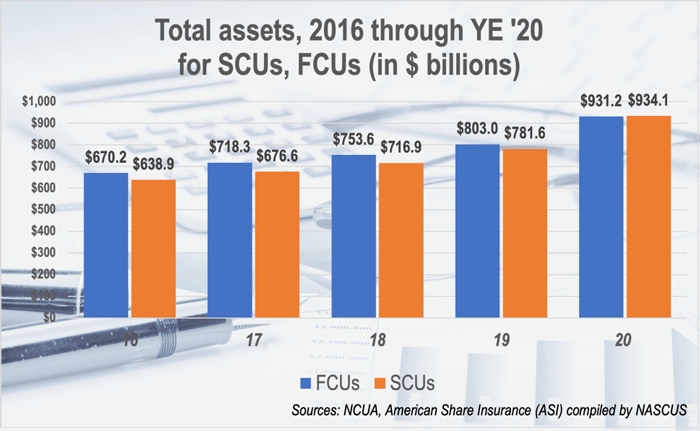

(March 5, 2021) After inching closer and closer for years, the total amount of assets held in state-chartered credit unions has exceeded that of federally chartered credit unions, with state charters now holding slightly more than 50%, according to numbers released by NCUA and compiled by NASCUS this week.

The numbers, gleaned from year-end call reports for both federal- and state-chartered credit unions (including federally and privately insured institutions), show state-chartered credit unions with $934.1 billion in assets, compared to $931.2 billion for federals. Overall assets held by credit unions are now approaching $2 trillion ($1.84 trillion). (State chartered statistics are from NCUA call reports for federally insured, state-chartered credit unions, and from American Share Insurance (ASI) Inc. for privately insured credit unions.)

“Credit union members, in response to the financial impact of the coronavirus crisis, clearly decided to hold onto or build their savings over the last year, when the pandemic’s impact became fully apparent,” said NASCUS President and CEO Lucy Ito. “Clearly, those members determined that state-chartered credit unions were a safe and sound place to maintain their savings – including their stimulus payments — reflecting the confidence in state credit unions built through responsible leadership by credit union boards and management and the careful supervision of state regulators.”

Assets at state charters grew by 19.5% over the last year, compared to 15.9% for FCUs. State system credit union memberships advanced by 3.8% (to 58.6 million); FCUs saw their memberships rise by 2.8% (to 63.1 million), for a grand total of 121.7 million memberships.

The number of credit unions continued a long slope downward, with 2,020 state charters (down 44 from year-end 2019), and 3,185 FCUs (down 98 from the end of last year). There were 5,205 credit unions at the end of 2020.

In other statistics, NCUA reported for federally insured credit unions:

- Insured shares and deposits rose $242 billion, or 19.8%, in 2020 from the previous year – a big driver of the increased assets at credit unions.

- Total loans outstanding were up $55 billion, or 4.9%, from the previous year (to $1.16 trillion); the loan-to-share ratio dropped to 73.2% at the end of 2020, down from 84% at the end of 2019 (before the pandemic’s impact was apparent).

- Net income was down $2.1 billion during 2020 compared to 2019, to $12 billion. NCUA said the decline was due primarily to a jump in provisioning for loan and lease losses or credit loss expenses.

- The return on average assets (ROAA) was 70 basis points (bps) at the end of 2020 – down from 93 bp at year-end 2019. However, NCUA pointed out that the median return on average assets across all federally insured credit unions at the end of 2020 was 40bp, down 20bp from the end of the previous year.

- The return on average assets for federally insured credit unions was 70 basis points in the fourth quarter of 2020, down from 93 basis points in the fourth quarter of 2019. The median return on average assets across all federally insured credit unions was 40 basis points, down 20 basis points from the fourth quarter of 2019.

LINK:

NCUA Releases Q4 2020 Credit Union System Performance Data

(March 5, 2021) NASCUS has published its summary of NCUA’s regulatory review roster for 2021, which lists the one-third of the agency rules that it is reviewing – part of the three-year review plan by the agency. This summary is also available to members only.

Under the review plan, the agency’s Office of General Counsel maintains a rolling review schedule of one-third of NCUA rules each year, and seeks public comment on those.

Among the rules being reviewed this round: Security program, report of suspected crimes, suspicious transactions, catastrophic acts and Bank Secrecy Act compliance (Part 748 of the agency’s rules); Golden parachute and indemnification payments (Part 750); Registration of residential mortgage loan originators (Part 761); Rules of NCUA Board procedure, promulgation of NCUA rules and regulations, public observation of NCUA Board meetings (Part 791); and Post-employment restrictions for certain NCUA examiners (Part 796).

LINK:

NASCUS Summary: NCUA 2021 regulatory review

(March 5, 2021) A “regulatory alert” outlining Home Mortgage Disclosure Act (HMDA) data collection is outlined by NASCUS in one of the latest summaries to be posted by the association.

The summary is available to members only.

Last month, the agency issued its Regulatory Alert 21-RA-04, which lists the requirements for collecting HMDA data associated with mortgage loan applications processed during 2021. The alert also lists (as further noted in the summary) the HMDA data partial exemptions for certain transactions.

(March 5, 2021) The mandatory compliance date of the general qualified mortgage (QM) final rule would be delayed 15 months (from July 1 to Oct. 1, 2022) under a proposal issued this week by CFPB.

In a release, the agency said it has issued a notice of proposed rulemaking (NPRM) to delay the rule, which was only finalized in December under former Director Kathleen Kraninger.

Under the previous rule, the requirement for general QM loans was that the borrower’s debt-to-income ratio (DTI) not exceed 43% with a new requirement of a limit based on the loan’s pricing. Under the new rule adopted in December, which was slated to take effect July 1 but is proposed to be delayed to next year, a price-based approach was installed for limiting lending in replacement of the specific 43% DTI limit after determining that a loan’s price is a strong indicator of a consumer’s ability to repay.

CFBP Acting Director Dave Uejio, in a release, stated that extending the compliance date will ensure that homeowners struggling with the financial impacts of the COVID-19 pandemic have the options they need.

“At a time when so many consumers are struggling and at risk of losing ground, particularly Black and Hispanic consumers, we need to do all we can to help people stay in their homes and to ensure the availability of responsible, affordable mortgages,” Uejio said. “In proposing to extend the date by which lenders must comply with the CFPB’s new General QM definition, we are working to provide needed options for both homeowners and lenders during a time of uncertainty and hardship.”

The agency also said extending the mandatory compliance date of the general QM final rule would allow lenders more time to offer QM loans based on the homeowners’ debt-to-income (DTI) ratio, and not solely based on a pricing cut-off.

“Extending the compliance date of the General QM final rule would also give lenders more time to use the GSE Patch, which provides QM status to loans that are eligible for sale to Fannie Mae or Freddie Mac,” CFPB said.

CFPB noted that if the proposal is finalized, a number of things would remain in place. That is: the old, DTI-based general QM definition; the new, price-based General QM definition; and the GSE Patch (unless the GSEs exit conservatorship prior to Oct. 1, 2022) would all remain available as long as the lender received the consumer’s application prior to Oct. 1, 2022.

Comments on the proposal are due April 5.

LINK:

CFPB Proposes Delay of Mandatory Compliance Date for General Qualified Mortgage Final Rule

(March 5, 2021) Watching closely to determine what additional support may be needed for smaller credit unions and minority depository institutions in the months to come as they face the continuing coronavirus crisis will be a priority for NCUA, NCUA Board Member Rodney Hood said this week.

At the same time, he and board Vice Chairman Kyle Hauptman agreed that the agency needs to loosen up chartering requirements so that more federal credit unions can be created.

In recorded remarks to the Credit Union National Association (CUNA) Governmental Affairs Conference, NCUA Board Member (and former Chairman) Rodney Hood said many financial institutions were left more vulnerable than they would otherwise have been due to the financial impact of the pandemic. “So closures of financial institutions, with the attendant systemic risks, are always a possibility,” he said.

Hood said, should closures occur, regulators need to be “prepared to respond appropriately to ensure the safety and soundness of the larger system,” and that it would always be his preference to save institutions rather than merging them.

In other comments, Hood said that moving forward with a new rule to expand lending authorities for credit union service organizations (CUSOs), which is now out for comment, is a priority for him. “This rule also would allow credit unions to invest in non-credit union owned fintech companies, something that I think is critical in today’s marketplace,” he said.

The NCUA board member also voiced support for “significantly” streamlining and simplifying the process of chartering new credit unions. NCUA Board Vice Chairman Kyle Hauptman, during his recorded comments at the conference, echoed Hood’s call.

“There has got to be an easier path for de novo credit unions,” Hauptman said. “I’m from Maine, and I was pleased to hear about a new credit union chartered in my home state just last year— until I learned it took nine years to accomplish. Nine. Things may move a bit slowly in Maine, sure, but not that slowly. Self-reliant, accountable people who want to work cooperatively with others to charter a new credit union that they will own, deserve a clear path to make that a reality.”

Hauptman said he intends to talk to persons who have recently started a credit union and those who want to start one. He said his goal is to work with NCUA staff on a new, easier path for creating new credit unions.

LINK:

NCUA Board Member Rodney E. Hood Remarks before CUNA’s 2021 Governmental Affairs Conference

NCUA Vice Chairman Kyle S. Hauptman Remarks before CUNA’s 2021 Governmental Affairs Conference

(March 5, 2021) Staying focused on capital and liquidity, consumer financial protection, and diversity, equity and economic inclusion will achieve a vibrant economic outcome from the impact of the coronavirus crisis for everyone, including credit unions, the NCUA Board chairman said in a speech this week.

In recorded video remarks to the Credit Union Natl. Assn.’s (CUNA) annual Governmental Affairs Conference (GAC) this week, Chairman Todd Harper urged credit unions to pay careful attention to capital, asset quality, earnings and liquidity as they and their members emerge from the crisis. He urged credit unions to mitigate problems when they develop. And, as the pandemic evolves, he said his agency will continue to adjust its supervision and examination program to mitigate potential risks to the National Credit Union Share Insurance Fund (NCUSIF). He made no mention about a premium to be paid to the fund.

Harper also advocated for creation of a dedicated program to supervise for compliance with consumer financial protection and fair lending laws. He indicated that the agency, in 2020 exams, had found “notable shortfalls” in credit union compliance with the Fair Credit Reporting Act (FCRA), the Electronic Funds Transfer Act (EFTA) and the Truth in Lending Act (TILA).

He said creation of a dedicated consumer protection unit at the agency would “better protect consumers’ interests, ensure that the credit union system lives up to its commitment to serve members, and provide a comparable level of consumer protection oversight as federal bank regulators.”

However, he also said the agency would continue to focus on compliance with forbearance provisions of the 2020 Coronavirus Aid, Relief, and Economic Security (CARES) Act to help consumers facing difficulties spawned by the pandemic. “Whether it means reworking an existing loan due to financial stress, or delaying payments, the NCUA will not criticize a credit union’s efforts to provide prudent relief for members when such measures are conducted in a reasonable manner with proper controls and management oversight,” he said.

He told the group that – given the cooperative philosophy of credit unions – that each credit union “has a moral obligation to step up and help minority-owned businesses and communities recover and start anew in the months ahead.” He challenged the viewers to deliver more financial products and services “free of discrimination or unfair practices to people of color and within communities of color,” adding that such efforts will be “vital to ensuring a more equitable economic recovery.”

LINK:

NCUA Chairman Todd M. Harper Remarks before CUNA’s 2021 Governmental Affairs Conference

(March 5, 2021) NCUA’s Rodney Hood was named the agency’s representative on the board of NeighborWorks America, a public-private organization that promotes affordable housing and community development, NCUA Chairman Todd Harper said this week. The group’s board consists of representatives of financial regulatory agencies and the U.S. Department of Housing and Urban Development (HUD) and includes (in addition to Hood): Martin Gruenberg, member of the FDIC Board, serving as NeighborWorks’ board chair; Michelle W. Bowman, member of the Federal Reserve Board of Governors, serving as vice chair; Grovetta Gardineer, senior deputy comptroller for bank supervision policy at the (OCC) … Federal civilian agencies were advised this week to install a patch for Microsoft Exchange for on-premises products – or disconnect those products until they do update with the patch. The “emergency directive” issued by the federal Cybersecurity and Infrastructure Security Agency (CISA) said the directive was issued in response to observed active exploitation of these products using previously unknown vulnerabilities. The directive also requires agencies to collect forensic images (if they are currently able to do so), and requires agencies to search for known indicators of compromise after patching; if indicators are found, they agencies are advised, they should contact CISA to begin incident response activities … The State of Washington, Dept. of Financial Institutions, is inviting applications for the position of program manager, chief of specialty examinations; see the NASCUS “state job opportunities” page (link below) for more details … NASCUS now has its own Facebook page, an effort undertaken by NASCUS Senior Director of Communications and Marketing Amanda Tuckey to expand the association’s reach. “We’re welcoming everyone to follow our page for daily NASCUS/industry news,” Tuckey said.

LINKS:

Chairman Harper Appoints Hood to NeighborWorks America Board of Directors

CISA issues emergency directive requiring federal agencies to patch critical vulnerability

NASCUS state job opportunities (WA program manager, chief of specialty exams)

NASCUS Facebook page (https://www.facebook.com/NASCUS)

(March 5, 2021) Kudos to NASCUS Credit Union Advisory Council Member Brian Wolfburg, CEO of VyStar CU in Jacksonville, Fla., for introducing William “Bill” J. Bynum, CEO of Hope Credit Union and former Herb Wegner Award Winner from 2016, in a recorded message this week. The Wegner award, sponsored by the National Credit Union Foundation, is typically awarded to individuals whose words and deeds revolutionize the ways credit unions serve their communities. This year, in a bow to social distancing during the pandemic, the NCUF honored past winners, rather than in-person celebrations. VyStar sponsored Bynum’s presentation.

(March 5, 2021) Kudos to NASCUS Credit Union Advisory Council Member Brian Wolfburg, CEO of VyStar CU in Jacksonville, Fla., for introducing William “Bill” J. Bynum, CEO of Hope Credit Union and former Herb Wegner Award Winner from 2016, in a recorded message this week. The Wegner award, sponsored by the National Credit Union Foundation, is typically awarded to individuals whose words and deeds revolutionize the ways credit unions serve their communities. This year, in a bow to social distancing during the pandemic, the NCUF honored past winners, rather than in-person celebrations. VyStar sponsored Bynum’s presentation.

(March 5, 2021) The day before CFPB Director Nominee Rohit Chopra’s appearance before a Senate committee considering his nomination, the bureau released a report from the current acting director saying the agency is working to mitigate home foreclosures prompted by the economic fallout of the coronavirus crisis.

Acting Director Uejio, in a report posted on the bureau’s website, said up to 10% of U.S. households are now at risk of eviction and foreclosures, largely as a result of the economic impact of the coronavirus crisis. Uejio also noted that the bureau is working with other agencies to mitigate a potential flood of home foreclosures and evictions in the coming months.

“The good news is that actions taken by both the public and private sector have, so far, prevented many families from losing their homes during the height of the public health crisis,” Uejio wrote in a blog post. “However, as legal protections expire in the months ahead, over 11 million families – nearly 10% of U.S. households – are at risk of eviction and foreclosure. He added that “put simply: we have very little time to prevent millions of families from losing their homes.”

The report notes that, in 2020, those who have fallen behind at least three months on their mortgage increased 250% to more 2 million households. The report asserts that delinquencies are “now at a level not seen since the height of the Great Recession in 2010.”

Collectively, the report states, these households are estimated to owe almost $90 billion in deferred principal, interest, taxes and insurance payments. Meanwhile, the report continues, there are more than 8 million rental households behind in their rent, which the report termed “a rental crisis.”

LINKS:

Housing insecurity and the COVID-19 pandemic

(March 5, 2021) Saying he looks forward to approaching with an open mind the mission of the CFPB, director nominee Rohit Chopra told a Senate panel this week that fair and effective oversight of the mortgage market can promote a “resilient and competitive financial sector” while also addressing racial inequities.

Testifying before the Senate Banking Committee during a hearing on his nomination, Chopra said during the last economic crisis of 10 years ago, “we saw how unlawful and avoidable foreclosures proved to be catastrophic in cities, small towns, and rural areas alike, contributing to deeper social divisions and inequities.”

He said the country again faces “an important test to ensure that troubles in the housing market do not sabotage the recovery of our local economies.”

During questions and answers, Chopra said he also has an open mind about changes to qualified mortgage (QM) rules. He said he would look to what the statute says and what Congress’ goals are as the bureau reviews the rules. (See additional story, below.)

Last week, Acting Director Dave Uejio released a statement that the agency is considering revising or outright revoking the “seasoned QM” rule (which applies to portfolio loans meeting certain performance requirements over a 36-month seasoning period, including having no more than two delinquencies of 30 or more days and no delinquencies of 60 or more days). The bureau also said it “expects to shortly issue” a proposal that would delay the July 1 mandatory compliance date for the general QM rule.

Chopra, during his appearance before the panel, said the bureau won’t dictate financial policy. When it comes to QM, he said, “it is important that we balance the consumer protections that Congress has put into place with access, including for rural and other areas.”

LINK:

Rohit Chopra, opening statement before Senate Banking committee (March 2, 2021)