(June 11, 2021) Changes made during its reorganization have led to a loss of fair lending expertise at the CFPB, and other actions taken by the agency could lead to reduced transparency and difficulty in assessing progress toward fair lending goals, according to a report issued by the Government Accountability Office (GAO) this week.

GAO said that a reorganization by the bureau in 2018 shuffled its fair lending activities, resulting in expertise being reallocated throughout the agency. The congressional watchdog stated that, when the agency conducted the reorganization three years ago, it moved its fair lending office from the supervision, enforcement and fair lending division to the office of former Director Kathleen Kraninger reallocating some of the fair lending office’s responsibilities along the way.

More specifically, GAO said those key changes in the 2018 reshuffling were:

- Responsibility was moved from specialist attorneys in the fair lending office to generalist attorneys in its enforcement office.

- Subject matter expertise and exam support was shifted from dedicated fair lending office supervision staff to a new team in the office of supervision policy.

- Responsibility for selecting institutions for fair lending exams and identifying enforcement priorities was reassigned from the fair lending office to supervision offices and the office of enforcement at the bureau.

“As CFPB planned and implemented the reorganization, it did not substantially incorporate key practices for agency reform efforts GAO identified in prior work—such as using employee input for planning or monitoring implementation progress and outcomes,” the congressional watchdog stated.

The GAO also said that it identified “challenges related to the reorganization” that included loss of fair lending expertise and specialized data analysts. The agency indicated those losses may have “contributed to a decline in enforcement activity in 2018.”

In any event, the report stated, the bureau has not assessed how well the reorganization met its own goals or how it affected fair lending supervision and enforcement efforts.

LINK:

Fair Lending: CFPB Needs to Assess the Impact of Recent Changes to Its Fair Lending Activities

(June 11, 2021) Marijuana and hemp are the subjects of a three-day virtual conference, sponsored by NASCUS, which wraps up today after delving into a wide variety of subjects about offering financial services in the fast-developing industry.

More than two dozen speakers are featured at the event (including NCUA Board Member Rodney Hood), which kicked off Wednesday, and looked at recent regulatory updates, how business is evolving in the space, details of cannabis and hemp banking programs at credit unions, and business payments.

The event was led by Deirdra O’Gorman, founding and principal of DX Consulting, a Bank Secrecy Act/anti-money laundering (BSA/AML) consulting firm for cannabis banking.

Specific sessions looked at cash logistics and onsite compliance in cannabis business solutions, building sustainable cannabis business in a regulated environment, lending, NCUA guidance (with Tim Segerson, deputy director of the agency’s office of examination and insurance), hemp rules from the U.S. Department of Agriculture, and a regulator’s perspective on exam programs (featuring NASCUS Vice Chairman Janet Powell, chief of regulation and supervision – credit unions, Oregon Department of Consumer and Business Services).

Videos of key sessions from the event are posted on the NASCUS website, available to registered attendees of the program.

LINK:

NASCUS Marijuana & Hemp eSchool

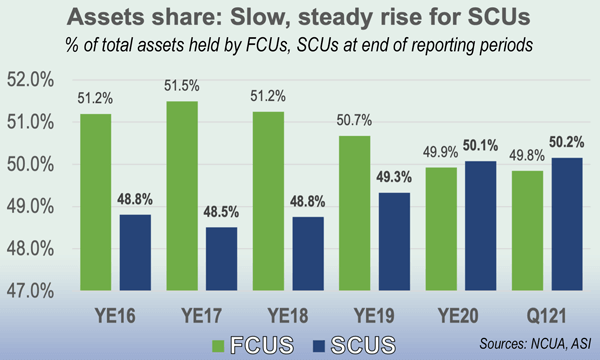

(June 11, 2021) Credit union assets mushroomed to a total of just under $2 trillion in the first quarter of the year – and state-chartered credit unions kept pace with the growth, maintaining a slight edge over federals in the share of total assets held as of March 31, according to numbers released by NCUA, and compiled by NASCUS, late last week.

(June 11, 2021) Credit union assets mushroomed to a total of just under $2 trillion in the first quarter of the year – and state-chartered credit unions kept pace with the growth, maintaining a slight edge over federals in the share of total assets held as of March 31, according to numbers released by NCUA, and compiled by NASCUS, late last week.

According to first-quarter credit union statistics culled from first quarter call reports, the nation’s 2,007 state credit unions (federally and privately insured) held 50.2% of total assets, with the 3,167 federals holding the balance. Growth of assets in the first quarter slightly favored state credit unions, which advanced their holdings by 5.85%; FCUs grew by 5.52%. Membership at the state credit unions advanced by just over 500,000 (0.83%); FCUs saw memberships grow by 900,000 (1.39%). Total membership for credit unions was 125.8 million (FCUs have the edge here, with 51.7% of all members).

As in past quarters, most of the growth in assets was centered on the largest of credit unions: those with at least $1 billion (395 credit unions). Those CUs held more than $1.4 trillion in assets and 72% of all assets in credit unions. Membership grew by 10% and net worth increased by 13.7%, according to NCUA. (The 293 credit unions with more than $500 million but under $1 billion in assets held about 10% of total assets and also saw increases in their lending, memberships and net worth).

Those results are in stark contrast with smaller credit unions (those under $500 million in assets): according to NCUA, loans, membership and net worth among those credit unions – which make up 92% of all credit unions, but hold only about 17% of all assets — declined in the first quarter, following a trend of the last several years.

NASCUS President and CEO Lucy Ito affirmed that the inflow of savings from stimulus payments and other sources was a key factor in driving up assets at credit unions that saw growth. But she also praised the management of state credit unions for ensuring their members have a haven for their savings, and that the members understand the safety and value a credit union offers.

“The numbers make it clear that credit union members recognize that their state-chartered institutions are strong, safe and resilient institutions that watch out for their members’ interests,” she said.

But she also acknowledged the struggle that smaller credit unions face in today’s environment. “State supervisory authorities are committed to doing whatever they can, in concert with safety and soundness, to give smaller credit unions their best chance to thrive,” Ito said. “Small credit unions play a key role in the lives of their members, and the state system wants that role to continue.”

Other first quarter results for federally insured credit unions (state and federal) reported by NCUA showed:

- The return on average assets for federally insured credit unions was 104 basis points in the first quarter of 2021, up from 52 basis points in the first quarter of 2020.

- Net income totaled $19.7 billion at an annual rate, up $11.3 billion (134.9%) from the same period a year ago.

- The net interest margin was $48.7 billion, 2.57% of average assets.

- Delinquency and net charge-off rates were both down, compared to a year ago: the former was 46 basis points (down 17 points from last year); the latter (as the net charge-off ratio) was 35 bp (down from 58 bp in the first quarter of 2020).

LINK:

Rising Net Income, Elevated Insured Share Growth Reported in First Quarter of 2021

(June 11, 2021) Actions taken by the federal credit union regulator in April – extending temporary provisions giving credit unions some regulatory relief from savings surges during the coronavirus crisis – were reinforced by the agency late last week in a letter to federally insured credit unions.

NASCUS has prepared a summary of the letter, which is available now (members only).

In its Letter to Credit Unions (21-CU-04), the NCUA Board reminded credit unions that the actions it took in April — reducing the earnings retention requirement for credit unions classified as adequately capitalized, and permitting an undercapitalized credit union to submit a streamlined net worth restoration plan if it becomes undercapitalized predominantly because of share growth during the coronavirus crisis – are in effect until the end of March 2022.

The action taken in April was essentially an extension of a decision made in June 2020, which the agency said was taken in “anticipation that some federally insured credit unions may experience a temporary reduction in earnings and regulatory capital ratios due to their COVID-19 response efforts.” Those temporary modifications expired Dec. 31, 2020.

However, NCUA decided earlier this year to reintroduce the temporary changes, due to the continued impact of the COVID-19 pandemic, the agency said.

LINKS:

NCUA Letter to Credit Unions 21-CU-04, Renewal of Prompt Corrective Action Relief

NASCUS SUMMARY: LTCU 21-CU-04, renewal of PCA relief (members only)

(June 11, 2021) NASCUS posted two other summaries this week, on NCUA-issued “regulatory alerts” over the last two weeks on the CFPB’s Regulation B (Equal Credit Opportunity Act, ECOA), and the bureau’s delay of the compliance date with the new “qualified mortgage” (QM) rule.

Both summaries are available to members only.

The ECOA alert advises credit unions that they should ensure policies, procedures, and training materials promote compliance with federal equal credit opportunity laws, and Regulation B administered by the CFPB, in line with a 2020 U.S. Supreme Court ruling. The alert (21-RA-07) notes that a March 16 interpretive ruling published by CFPB clarified the prohibition against sex discrimination in the ECOA.

The alert also notes that the rule is consistent with the 2020 high court ruling in Bostock v. Clayton County, Ga. That ruling held that the prohibition against sex discrimination in Title VII of the Civil Rights Act of 1964 encompasses sexual orientation discrimination and gender identity discrimination.

The second alert focuses on action taken by CFPB in late April, which moved compliance with the QM rule to Oct. 1, 2022 from July 1 of this year. The bureau said in April that the delay was made to “help ensure access to responsible, affordable mortgage credit, and preserve flexibility for consumers affected by the COVID-19 pandemic and its economic effects.”

The final rule making the change was titled “April 2021 Amendments to the ATR/QM Rule” (ATR stands for “ability to repay”).

In its alert, NCUA notes the two categories that the compliance date delay affects: General QMs and temporary GSE QMs (referring to QMs issued by government-sponsored enterprises Fannie Mae and Freddie Mac).

LINKS:

NASCUS Summary: 21-RA-07 Equal Credit Opportunity Act (Regulation B) (members only)

(June 11, 2021) Congratulations to Virginia’s Robert “Bob” Hughes retired as deputy director of the State Corporation Commission Bureau of Financial Institutions on May 28 after 41 years of service … Retiring NASCUS leader Lucy Ito is profiled in the American Banker (a trade publication) this week, focusing on NASCUS’ efforts to bring transparency and equity to the overhead transfer rate – which the article notes was a singular accomplishment during her nearly seven-year turn at the helm of the association. (To see the full text of the article, see the link below – subscription required) … Requiring financial institutions to report information on account flows for tax reporting purposes “would be a complex undertaking” with significant compliance burdens that may outweigh whatever benefits result, according to a letter sent from financial institution trade groups (including those representing credit unions) to a House subcommittee this week. The letter essentially cautions lawmakers about taking the step, which was proposed last week by President Joe Biden (D) in his 2022 budget. Under the proposal, all deposit, loan and investment accounts at financial institutions (including credit unions) for persons and businesses would be subject to a $600 “de minimus” gross inflow reporting threshold. The provision is designed to increase taxpayer compliance with income reporting … There is just a bit more than two weeks left for low-income designated credit unions to seek Community Development Revolving Loan Fund (CDRLF) grants, including minority depository (MDI) mentoring grants, NCUA said the week. The deadline is June 26 to apply for the approximately $1.5 million in CDRLF grants to the most-qualified applicants, subject to the availability of funds, the agency said. There are three categories of grants: underserved outreach (maximum award of $50,000); MDI mentoring (maximum award of $25,000); and digital services and cybersecurity (maximum award of $7,000).

LINKS:

American Banker — Lucy Ito’s legacy: Lowering a vexing regulatory cost for credit unions (subscription required)

(June 11, 2021) With the signing by the governor of legislation giving the Texas Credit Union Department 12 more years to serve the state’s credit unions and members, the agency’s future for the next dozen years is set.

The state legislature adopted the legislation late last month; Gov. Greg Abbott (R) signed it late last week. The law becomes effective Sept. 1.

In Texas, state agencies are subject to periodic review by the “Sunset Commission,” which in the case of the TCUD is every 12 years. The commission then makes a recommendation to the legislature for continuation of the agency.

In December, the commission found that the state has a “continuing need” for the state credit union department, and that it should be sustained for another 12 years. The commission’s report also said the state “benefits from having a strong credit union industry” and the current organizational structure of the department “is the most efficient and effective approach to regulation at this time.”

In addition to extending the operations of the department, the legislation (among other things) also: requires the department to track more comprehensive complaint and enforcement data to support analysis and guide regulatory activities; and mandates development of a process by the department for notifying and issuing guidance for credit unions about federal statutory or regulatory changes that take effect immediately and conflict with state law.

The TCUD (headed by Commissioner John J. Kolhoff) was created in 1969 and has been an independent agency since. In 2009, the agency earned “self-directed semi-independent (SDSI)” status, authorizing it to set its own fees, budgets, and performance measures independent of the legislative appropriations process. Over the past four decades, the commission has considered nine times folding the TCUD into the state’s Finance Commission (which oversees three agencies supervising banks, savings banks and other types of financial institutions and occupations). Each time, the Sunset Commission has recommended maintaining a separate credit union regulator with its own credit union commission.

“My thanks to the Sunset Advisory Commission, the incredible efforts of our staff, the leadership of the Credit Union Commission and the industry for making this possible; we are stronger together,” said Commissioner Kolhoff. “Thanks also to NASCUS for its support, especially bringing together state and federal agencies to ensure our programs remain efficient, effective, and continue to evolve.”

NASCUS CEO Lucy Ito thanked the state legislature for its decision, and congratulated Commissioner Kolhoff. “The TCUD, and Texas credit unions — through advocacy by the Cornerstone Credit Union League — did a phenomenal job in preparing for and navigating the sunset review process,” Ito said. “We are fortunate to have a system where regulators, credit unions, and leagues can work together to provide an environment with business practices that put members first.”

LINK:

Texas Extends Credit Union Department Operations Until 2033