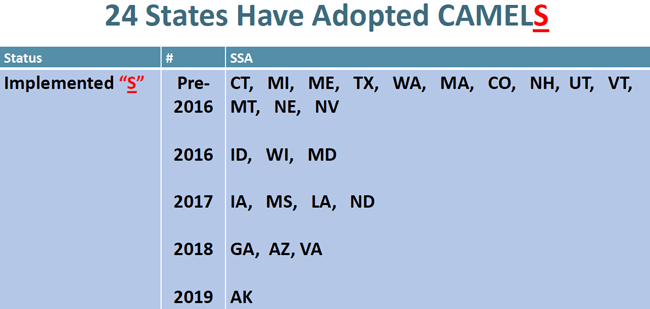

(Jan. 15, 2021) Adding an “S” for “market sensitivity” to the examination rating system for NCUA was proposed unanimously by the agency Board Thursday, an addition long supported by NASCUS for the federal regulator – especially since 24 states have already incorporated the component into their own exams.

The proposal would also redefine the “L” (Liquidity Risk) component in the existing rating system – and change the name to “CAMELS” (from the existing “CAMEL”).

Nearly five years ago, NASCUS wrote to NCUA urging the change and adding the “S” component. “NASCUS and state supervisory agencies encourage NCUA to consider earlier adoption of ‘CAMELS,’” NASCUS’ Lucy Ito wrote in the June 2016 letter to the board. “We again note that the separation of the ‘S’ component does not require a credit union to develop additional management system enhancements where market risk is already appropriately identified, measured, monitored and managed as part of the ‘L’ component.”

She also noted that in states that have adopted CAMELS (now totaling 24 – up from 16 when she wrote the letter), that regulators and credit unions have reported positive outcomes with nearly no additional regulatory burden. She stated that, in practice, state supervisors have continued to use the same examination procedures for assessing liquidity and interest rate risks. However, she wrote, by rating the “L” and “S” components separately—rather than in a combined component—state regulators have been able to provide better information to credit unions to clearly delineate analysis between liquidity risk and interest-rate risks.

Both Board Chairman Rodney Hood and Member Todd Harper mentioned NASCUS’ position on the S component, or the June 2016 letter, in their remarks – and stressed the importance of reaching out to the state system to discuss the proposal.

NCUA said that the proposal issued Thursday (for a 60-day comment period) would likely take effect in the first quarter of 2022 if adopted.

The agency asserted the proposal would provide greater clarity and transparency regarding credit unions’ sensitivity to market risk and liquidity risk exposures once adopted. “The proposed addition would make the NCUA’s rating system more consistent with the other financial institution regulators’ ratings system both at the federal and state levels,” the agency said.

The agency indicated that separating the “S” and “L” component ratings will allow NCUA to enhance:

- Monitoring of sensitivity to market risk and liquidity risk in the credit union system;

- Communication of specific concerns to individual credit unions; and

- Allocation of resources.

“In general, the NCUA Board expects that adopting a sixth CAMELS rating component will not have any adverse effect on a credit union’s CAMEL composite rating,” the agency wrote in its proposal. “The proposed separation of sensitivity to market risk and liquidity risk into individual CAMELS rating components will reduce potential rating inconsistencies.”

LINK:

Notice of Proposed Rulemaking, Parts 700, 701, 703, 704 and 713, CAMELS Rating System

(Jan. 15, 2021) In other action at its Thursday meeting, the NCUA Board:

- Adopted a final rule clarifying that corporate credit unions may purchase subordinated debt instruments issued by natural person credit unions (allowed under a final rule issued by NCUA late last year). The final rule also specifies the capital treatment of these instruments for corporate credit unions that purchase them. NASCUS and the state system strongly supported the subordinated debt rule, which allows well-capitalized, federally insured credit unions to count subordinated debt as capital for risk-based net worth purposes. The agency said it delayed finalizing the corporate rule, proposed in February 2020, until the subordinated debt rule itself was approved last month.

- Released (for a 30-day comment period, on a 2-1 vote with Harper dissenting) a proposed rule that would add to the agency’s list of permissible CUSO services the origination of any type of loan that a federal credit union (FCU) may originate. This expands the list of permissible loans by CUSOs from only business loans, consumer mortgage loans, student loans, and credit cards to any type of loan an FCU may originate, including, for example, automobile and small-dollar (payday) loans – the two types NCUA said would likely draw the newest involvement by CUSOs.

- Issued (for a 30-day comment period, on a 2-1 vote again with Harper voting no) a proposal raising the threshold for a credit union to be considered “complex” under risk-based capital rules from $50 million to $500 million and a risk-based net worth requirement that exceeds 6%. The change, if adopted, would be effective until the current risk-based capital (RBC) rule goes into effect, currently set for Jan. 1, 2022. “The COVID-19 pandemic has created a vital need for financial institutions, including credit unions, to provide access to responsible credit and other member services to support consumers,” which the agency inferred would be facilitated by the proposal.

- Heard a report on its 2021 Annual Performance Plan, which essentially outlines the general direction of the agency for the coming year through its strategic goals of: Ensuring a safe and sound credit union system; providing a regulatory framework that is transparent, efficient and improves consumer access; and “maximizing organizational performance to enable mission success.”

LINKS:

Final Rule, Part 704, Corporate Credit Unions

Proposed Rule, Part 702, Risk-Based Net Worth, Complex Threshold

Proposed Rule, Part 712, Credit Union Service Organizations

NCUA’s 2021 Annual Performance Plan

(Jan. 15, 2021) Lucy Ito praised the NCUA Board for moving forward on expansion of the rating system to include the “S” component. “We’re almost at the finish line – but we are willing and able to keep working with the agency to complete the process, and see this change made in time to be effective in 2022,” she said. “The state system is driving toward this goal out of a desire to have consistent standards set across the credit union system, and to reduce risk. For some time, state examiners have observed that the extended low-yield environment may encourage greater risk taking by financial institutions. We urge the agency to finalize this proposal as soon as possible following the comment period and as soon as practicable following necessary technical re-programming.”

(Jan. 15, 2021) NASCUS President and CEO Lucy Ito urged careful review of the proposal by the entire credit union system – and noted that federal law requires the agency to consult with the state system. “The FCU Act requires NCUA to consult and cooperate with state supervisors on prompt corrective action and capital adequacy issues, and we expect the agency to meet its lawful obligation,” she said. “Both approaches outlined by NCUA represent significant changes to how federally insured credit unions will meet capitalization requirements. The approaches include trade-offs that credit unions must weigh thoroughly, but also offer the potential for significant flexibility. NASCUS urges all of its members, both regulators and credit unions, to study this proposal carefully and offer input to us as we prepare our own feedback to the agency on the proposal.”

(Jan. 15, 2021) Applications for appointments to membership on one of four advisory committees that offer input from various sections of the financial industry, and for research projects by the agency, to the CFPB are now being taken, the bureau said this week. New members, selected through the application process, are expected to be announced in late summer, according CFPB.

Applications for membership in the bureau’s Credit Union Advisory Council (CUAC), Consumer Advisory Board (CAB), Community Bank Advisory Council (CBAC), and Academic Research Council (ARC). According to the bureau, membership in the committees includes representatives of consumers, diverse communities, the financial services industry, academics, and economists.

Qualification for membership goes beyond experts in the industry to those who have been affected by events or decisions of the industry, according to the notice. It states that membership is also open to “representatives of communities that have been significantly impacted by higher-priced mortgage loans, and seek representation of the interests of covered persons and consumers, without regard to party affiliation.”

Appointments to the committees are generally for two years.

The eight-person CUAC now includes executives of two NASCUS member credit unions (Brian Holst of Elevations Credit Union and Jeremiah Kossen of Town & Country Credit Union) and executives from three additional state-chartered credit unions (Racardo McLaughlin of TwinStar Credit Union, Monica Davis of Union Square Credit Union), Doe Gregerson of Landmark Credit Union).

LINK:

Applications open for advisory committee appointments

Bios, additional information of current CUAC members

(Jan. 15, 2021) Florida (and NASCUS) welcome a new state-chartered credit union this week: Radiant CU of Gainesville (formerly SunState FCU). The 64-year-old credit union holds $570 million in assets and counts about 40,000 members … Melissa M. Lowden will be NCUA’s next deputy chief financial officer, effective Jan. 17, the agency said this week. In a release, the agency said Lowden – who joined NCUA in 2015 – will oversee accounting and financial reporting, enterprise risk management, strategic and performance planning, budgeting, procurement, facilities and logistical support, the administration of credit union operating fees, and the National Credit Union Share Insurance Fund’s (NCUSIF) capitalization deposits and investments … Brian Brooks, the acting comptroller of the currency, on Thursday resigned from the agency; Blake Paulson, formerly senior deputy comptroller and chief operating officer at the Office of the Comptroller of the Currency (OCC) was named his successor in accordance with federal statute.

LINK:

Lowden Named Deputy Chief Financial Officer

(Jan. 15, 2021) A final rule extending to Dec. 31, 2021 a temporary final rule on loan participations is the subject of the latest summary to be developed by NASCUS and posted on the association’s website.

The summary is available to members only.

At its Dec. 17 meeting, the NCUA Board approved (unanimously), an extension for a temporary final rule that increases the maximum aggregate amount of loan participations that a federally insured credit union (FICU) may purchase from a single originating lender without seeking a waiver from NCUA to the greater of $5 million or 200% of the FICU’s net worth (up from the greater of $5 million or 100% of the FICU’s net worth).

The rule had been slated to expire Dec. 31, 2020. The temporary rule, adopted by the NCUA Board as a relief measure for credit unions in the midst of the coronavirus crisis last spring, originally took effect April 21.

LINK:

Summary: Final rule, Temporary Regulatory Relief in Response to COVID-19 — Extension (members only)

(Jan. 15, 2021) Improving coordination between NCUA and CFPB over the consumer protection supervision of credit unions with more than $10 billion in assets is the stated purpose of a “memorandum of understanding” announced by the two agencies Thursday.

In a joint release, the two agencies said that under the agreement they will “pursue opportunities to proactively and efficiently share supervisory information, including drafts of Covered Reports of Examination and final Reports of Examination for credit unions” with more than $10 billion dollars in assets. The agencies said they would use “secure, two-way electronic means” to accomplish that and that they will “jointly collaborate in semi-annual strategy planning sessions to identify and address areas of alignment and coordination in examinations for covered institutions.”

CFPB and NCUA also asserted that the agreement would “better facilitate coordinated examinations” to increase efficiency, and that the two agencies would share information on training activities and content, as well as on supervisory activities and potential enforcement actions.

(Jan. 15, 2021) Mark your calendars for four upcoming events from NASCUS in the months ahead – including the week after next.

- Jan. 25: NASCUS sponsors a webinar (for members only) outlining the Solar Winds/Orion security breach (by Russian actors), and its impact on the state system (both regulators and credit unions). The 90-minute session will take an in-depth look at the security breach, which was originally estimated to have affected about 18,0000 customers of the Solar Winds firm, and its Orion product – including a number of big federal agencies (such as the Treasury Department). There is no cost for the event, but it is open to members only.

- March 16: The Wisconsin Department of Financial Institutions, the Wisconsin Credit Union League and NASCUS team up to provide this annual session that looks at national and state issues (including the impact of COVID-19), duties, liabilities and protections of credit union directors, and succession and strategic planning. This is a virtual session that runs from 9 a.m. to noon (central time).

- March 17-18: NASCUS National Meeting (for state regulators only). This virtual meeting looks at the latest issues facing supervision and regulation of the state system, while also offering state regulators a forum where they can share ideas, discuss common issues, and uncover trends. The event this year will be virtual; registration is open only to state regulators.

- Summer: NASCUS Cybersecurity Conference with CUNA is scheduled to be held (with the precise date/time to be announced at a later time). The event has become the premier cybersecurity event within the credit union system, looking at the latest developments, trends and techniques for ensuring security of credit union systems. Like many other events in 2021, the cybersecurity conference will be held virtually.

For more information on any of these events, see the link below.

LINK:

NASCUS 2021 ‘Upcoming Events’

(Jan. 15, 2021) The state system has a new, direct contact on the NCUA Board: Vice Chairman Kyle Hauptman, who was named board liaison to NASCUS and another credit union group this week by Chairman Rodney Hood.

In a release, the agency said Hauptman’s responsibilities as liaison to the state system (and to the Defense Credit Union Council, a Washington-based group representing defense-based credit unions) would include meeting with both groups and reporting on priorities and recommendations to the NCUA Board. Hood noted that the Federal Credit Union Act empowers him, as NCUA Chairman, to determine each board member’s area of responsibility.

Hauptman said, in the release, that he is looking forward to working with NASCUS “as it will provide me with a broader understanding of the credit union landscape.”

NASCUS’ Lucy Ito, in a press statement of her own, congratulated Hauptman and added that the state system is fully ready and willing to interact with him to achieve his stated goal of developing a broader understanding of credit unions, particularly the role of the dual chartering system. “NASCUS shares the belief that a strong, equal partnership between NCUA and the state credit union system will help ensure a vibrant and mutually reinforcing dual charter system – which we also believe makes for a stronger, more resilient and long-lasting credit union system overall,” she said.

LINKS:

Hauptman Named NCUA Liaison to DCUC and NASCUS

(Jan. 15, 2021) Two approaches for simplifying risk-based capital (RBC) requirements for federally insured credit unions (FICUs) were proposed by the NCUA Board Thursday, one replacing the current rule with a risk-based leverage ratio (RBLR) rule requirement, and the second retaining the RBC rule but allowing credit unions to “opt-in” to the RBLR.

The proposal (an advance notice of proposed rulemaking (ANPR)) was issued for a 60-day comment period on a 2-1 vote, with Board Member Todd Harper objecting.

The final vote on the proposal came after a more than one-hour delay in which the sound (and written transcript) from the Internet-streamed, virtual meeting was unavailable. That meant, for the most part, discussion among the board members about the proposal was not public. The sound (and transcript) was audible (and visible) again just in time for the recorded vote of 2-1.

In issuing the ANPR, NCUA noted that the existing RBC rule, which was adopted more than five years ago, has been delayed to the first of next year. That delay time, the agency said, has provided it with more time to evaluate FICUs that are classified as “complex” (those with total assets greater than $500 million, a new threshold also set at the meeting Thursday).

NCUA said the RBLR contained in the proposal is intended to simplify the regulatory risk-based capital requirements, while ensuring the overall capital framework. “The RBLR approach would utilize certain risk characteristics to determine the required capital level,” the agency said. This approach differs from the 2015 final rule, the agency said, where all assets and certain off- balance sheet activities were categorized into risk groups and then risk-weighted to produce a risk- based ratio.

The first approach the board is considering, according to the agency, would replace the current risk-based capital rule with the RBLR requirement. The agency said that approach uses relevant risk attribute thresholds to determine which complex credit unions would be required to hold additional capital (or buffers).

The second approach would keep the 2015 RBC rule, but would allow eligible complex FICUs to opt-in to a “complex credit union leverage ratio” (CCULR) framework to meet all regulatory capital requirements. That approach would be modeled on the “Community Bank Leverage Ratio” (CBLR) framework, which is available to certain banks under certain conditions, and went into effect early last year (after adoption in 2019). NCUA Board Chairman Rodney Hood has, in the past, signaled his interest in the agency adopting a similar approach for credit unions. Under the CBLR, a community banking organization may qualify if it has a tier 1 leverage ratio of greater than 9%, less than $10 billion in total consolidated assets, and limited amounts of off-balance-sheet exposures and trading assets and liabilities.

The board also indicated that only one or the other of the approaches would be adopted, calling them mutually exclusive and that the CCULR would not be available under the RBLR.

NCUA also said it is considering the net worth ratio as the RBLR measurement. It would be supplemented, the agency said, with mandatory capital buffers when certain risk factors are triggered. That approach, NCUA said, would require an extra cushion of capital buffers over and above the 7% net worth ratio standard for classification as well capitalized “when certain characteristics inherent in a FICU’s balance sheet exceed specified thresholds.”

The risk factors under consideration, according to NCUA, would be based on the 2015 final rule, which it said used higher risk weightings.

LINK:

Advance Notice of Proposed Rulemaking, Part 702, Simplification of Risk Based Capital Requirements