By Michael K. Mahoney, Ogletree, Deakins, Nash, Smoak & Stewart, P.C.; National Law Review

Click here to read the entire article.

On May 19, 2026, President Donald Trump issued Executive Order No. 14406 (“Restoring Integrity to America’s Financial System”), which is likely to impact access to financial services for employees who are not U.S. citizens.

Quick Hits

- On May 19, 2026, President Trump issued an executive order calling for stricter due diligence requirements when financial institutions vet customer applications.

- The executive order requires banks and financial services companies to treat customers’ immigration status as a factor in evaluating potential financial risk.

- The executive order’s stated purpose is to “safeguard [the] financial system from illicit use[s],” such as unwithheld payroll taxes, money laundering, terrorism financing, and labor trafficking.

The executive order directs the secretary of the treasury and federal regulators to propose changes to Bank Secrecy Act regulations to strengthen due diligence requirements for financial institutions. A White House fact sheet explains, “Gaps in customer identification practices have allowed terrorists, drug traffickers, money launderers, and other criminal networks to exploit U.S. financial institutions to move illicit funds and evade law enforcement.”

The executive order describes red flags associated with suspicious financial activity, including:

- “evidentiary patterns of payroll tax evasion by employers or labor brokers,” including failures to withhold or remit federal taxes for non–work-authorized individuals;

- the use of unregistered third-party payment processors or digital platforms to “facilitate ‘off-the-books’ wage payments intended to bypass Bank Secrecy Act reporting thresholds or tax obligations”;

- the use of certain “foreign-identity documents, nominee accounts, shell companies, or complex ‘funnel’ structures designed to obfuscate the identity of the ultimate beneficial owners or conceal the true nature of payroll disbursements”;

- “patterns of repetitive, sub-threshold cash withdrawals or deposits that correlate with payroll cycles conducted outside of regulated payroll processing systems”;

- “financial activity indicative of labor trafficking or forced labor … where proceeds are commingled with legitimate business revenue or transferred to foreign jurisdictions; and

- “the use of an individual taxpayer identification number (ITIN) to obtain credit products or open depository accounts where the applicant lacks verified lawful immigration status.”

The executive order clarifies that an ITIN “facilitates tax compliance,” but its use in lieu of a Social Security number or valid work-authorized visa “may be identified as a risk factor requiring enhanced due diligence to ensure the account is not being utilized to facilitate the unlawful employment of unauthorized aliens.”

The executive order could make it more difficult for employees who are not U.S. citizens to open bank accounts, obtain credit, and access other financial services. It calls on federal regulators to issue guidance for banks and other financial institutions on managing the credit risks associated with extending loans and providing financial services to individuals without work authorization. It also directs the Consumer Financial Protection Bureau to consider changing regulations to clarify that potential deportation and loss of wages are factors that could affect a borrower’s ability to repay a loan.

Click here to continue reading.

By Josh Taylor, CSO Magazine

Click here to read the entire article.

The rise of autonomous AI in warfare has shifted cyber conflict from speed to scale, requiring a new doctrine focused on probabilistic, adaptive defense.

For most of my career running security operations, the shape of cyber conflict has been defined by who could move faster than the other side. Faster at identifying a vulnerability, faster at patching, faster at detecting, faster at responding. The last few months have made me reevaluate that framing. Speed still matters. It just no longer carries the picture on its own. Scale and autonomy have moved alongside it, and the relative emphasis I place on the three is something I expect to keep adjusting. When I read recent coverage of the US government’s deepening use of advanced AI for cyber operations, Anthropic’s Claude Mythos Preview disclosure and the wave of defensive AI being built in response, I recognized the pattern. It fits the pattern of doctrine forming.

Doctrine rarely arrives through formal announcements in this field. It emerges through repeated behavior, through choices made under operational pressure, through what capable actors do when no one is telling them to stop. That is where I believe we are now.

From tools to operational capability

I remember when cyber operations lived inside scripts. They moved into frameworks, then into automated pipelines, then into what we somewhat optimistically called orchestration. Each step compressed time and lowered required expertise. Frontier AI is starting to look to me less like the next step in that sequence and more like a different thing.

What seems to separate frontier AI from the automation we have lived with, in what I have seen so far, is less about efficiency and more about independence. A model that can conduct reconnaissance across an unbounded attack surface, identify vulnerabilities without predefined signatures, assist in exploit chaining and adapt based on feedback feels less like enhancing an analyst’s workflow and more like operating with reduced human constraint. That shifts the economics of offense in ways that break assumptions most security programs still quietly rely on.

Click here to continue reading.

Published in PYMNTS

Click here to read the entire article.

Subprime consumers are navigating the credit markets through a mix of installments, informal borrowing and carefully managed payment behavior that traditional scoring models do not always capture.

PYMNTS Intelligence data on the behavioral profiles of subprime consumers argues that the subprime population represents a durable and identifiable segment of roughly 44 million U.S. adults, rather than a temporary byproduct of economic pressure. The report found that 17% of U.S. consumers identify as subprime, a share that has remained within a relatively narrow range for 47 consecutive monthly survey waves dating back to March 2022.

The stability of that segment matters for lenders, merchants and installment providers because the data suggests these consumers continue to seek credit access, even as many traditional products fail to align with their financial realities. The report notes that 35% of subprime consumers hold no credit or store card at all, compared to just 4% of super-prime consumers.

The report repeatedly points to one structural characteristic separating subprime consumers from the broader population: chronic pressure around bill payment. Fifty-five percent of subprime consumers reported living paycheck to paycheck with difficulty paying bills, more than double the rate for the overall population.

Traditional underwriting models remain heavily anchored to credit bureau data, revolving utilization and repayment history. Yet the PYMNTS Intelligence findings suggest that cash-flow behavior, spending priorities and payment sequencing may provide additional insight into repayment capacity and consumer stability.

The report highlights several behavioral indicators that may prove increasingly useful in underwriting targeted credit products for subprime consumers. One of the clearest involves the handling of periodic cash-flow events such as tax refunds. Among subprime consumers who received refunds, 67% described the money as either critical or very important to maintaining financial stability. Thirty-six percent directed the largest share of those funds toward everyday expenses or bills.

Click here to continue reading.

By John Beauchamp, CUAnswers/CUSO Magazine

Click here to read the entire article.

Your team has been talking to a vendor who has a solution that is going to make your life amazing. The vendor even said integration with your core is FREE. All you must do is pay the recurring fees going forward and be willing to be their beta test…and of course, provide them your data to develop with. What a bargain.

Not so fast.

While this solution might be a bargain for your organization, without the proper due diligence, this seemingly wonderful integration could be a formula for disaster. Too often, organizations see only the promises of a cool, new solution without understanding the risks and implications of turning over member data. Risks include the possibility of violating privacy laws if information is turned over without members’ consent. You can also be on the hook for data breaches, whether by the vendor or a downstream organization that receives access to the data.

Top questions to ask before signing on the dotted line

Consider the following before quickly agreeing to send your data to a third-party vendor:

What/how much data is your vendor requesting?

Is the vendor only asking for the data required to accomplish the task you are engaging them for, or is the vendor broadly requesting data that is unnecessary for your purposes? You may be exposing your organization to a massive data breach by sending data unneeded to reach your goals. In addition, your vendor may want volumes of data for such purposes as training their Artificial Intelligence (AI) models, at your risk.

Are you compliant with privacy laws?

Many states require consent from a person before their information can be sent to a third party. While there are federal carve-outs in state privacy laws for data sent to third parties to provide members with a financial product or service, many states grant their residents much broader protection regarding notification and the right to opt out. Do not assume an all-encompassing right to send data without first ensuring that your members do not have notification, consent, and opt-out rights regarding the data you are sending.

Have you reviewed the vendor’s data security policy?

Anytime you send member data to a third party, you are required to ensure that the third party is adequately safeguarding the data. Depending on the data sent, ensure the vendor can demonstrate safety and data protection, including physical safeguards, employee training, and compensating controls for you to follow.

Click here to continue reading.

By Kurt Woock, NerdWallet

Click here to read the entire article.

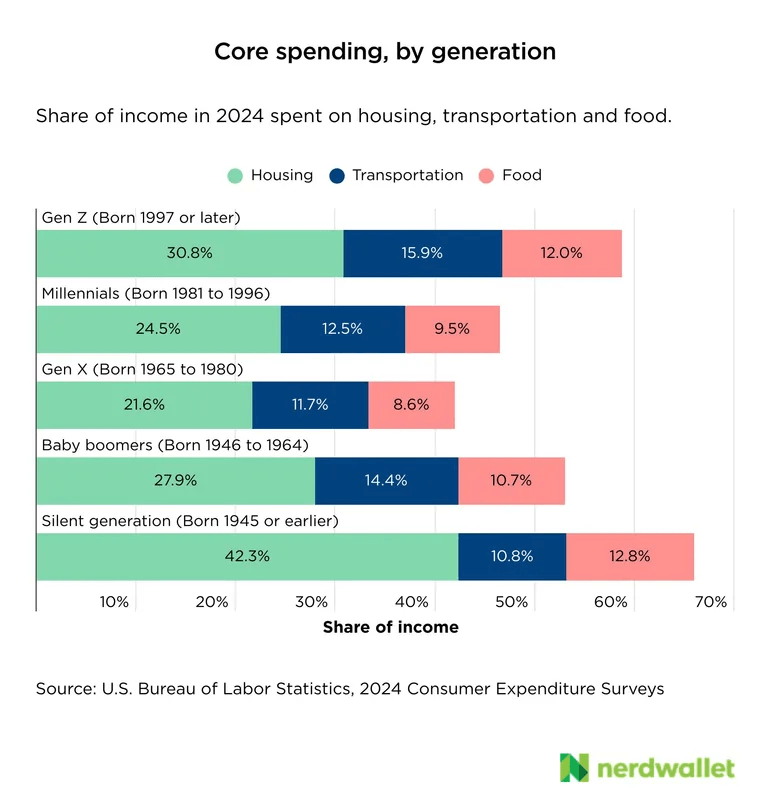

Changing priorities and shifting income cause spending habits to morph as people age.

American households spent an average of $539 on bakery products and $131 on postage and stationery in 2024. Those are a few of the quirkier spending habits tracked and categorized in the Consumer Expenditure Surveys, a nationwide survey of more than 30,000 people. The federal government has conducted detailed expenditure surveys since 1888.

The Bureau of Labor Statistics releases this data, which includes spending details on hundreds of items for different generations, in one-year batches. While it may seem outdated by the time it’s released — particularly last year, when the 2024 data release was delayed until December due to the federal government shutdown — the tradeoff is specificity: We can put the spending patterns of specific groups of Americans under a magnifying glass.

Overall spending trends, by generation

The average dollar amount spent isn’t the best way to understand this data. Varying incomes can distort the meaning behind raw dollar amounts. For example, a younger household may spend a smaller dollar amount at restaurants than an older household, but if the younger household has a lower income, they may still be devoting a larger percentage of their income to eating out.

Instead, comparing the share of spending to the average income for each demographic reveals how much income each expense category eats up. Income reported in this survey is pre-tax.

Housing, transportation and food make up the core of American budgets. These three expenses used, on average, 48% of a household’s income in 2024. (The BLS measures spending by household, or what they call a “consumer unit.” That term includes families and other groups who pool their income and expenditure decisions. Roommates, on the other hand, are distinct consumer units.)

Click here to continue reading.

By Jim Tyson, CFO Dive

Click here to read the entire article.

Before the war with Iran, 8% of adults said their family sometimes or often lacked enough food, the Federal Reserve said, citing survey results.

Dive Brief:

- Roughly three out of four U.S. adults (73%) said they are “doing okay financially” or “living comfortably” even as their view of the economy has dimmed, with 42% of survey respondents voicing concern about finding or keeping a job, the Federal Reserve said.

- More than 90% of adults identified inflation as a concern, the central bank said in a report on an annual survey, noting that price pressures persisted as their most common financial worry.

- “Fifty-eight percent [of households] said that changes in the prices they paid compared with the prior year had eroded their financial standing,” the Fed said, with 14% saying inflation had made their situation much worse.

Dive Insight:

The economic outlook has dimmed since the Fed gathered results for the survey in October, with the Iran war increasing price pressures and prompting downgrades of forecasts for growth.

“The Middle East war is expected to exert a modest but meaningful drag on near-term growth through renewed supply chain disruptions, higher shipping costs and increased uncertainty around energy and trade flows,” LPL Financial Chief Economist Jeffrey Roach said Monday.

The war will likely slow growth by 0.2 percentage point in the second quarter and by 0.3 percentage point in Q3, he said in a note. Economists see 35% odds of a recession in the next 12 months, an increase from 32% in February and March, according to a Wolters Kluwer survey.

Inflation is casting a shadow on the outlook. A war-induced surge in energy prices last month pushed up the rate of price gains to a three-year high, with the consumer price index climbing 3.8% on an annual basis. The cost of energy jumped 17.9% during the past year, spurred by a 28.4% increase in the price of gasoline and 54.3% gain in the price of fuel oil, the Bureau of Labor Statistics said Tuesday.

Price pressures, and declining affordability, have eroded consumer sentiments to record lows in recent months. In turn, retail sales growth slowed to 0.5% last month from 1.6% in March as a war-induced surge in price pressures exceeded wage gains and put the price of some goods out of reach for low-income consumers. On an annual basis, sales increased 4.9%, the Census Bureau said Thursday.

Before the Iran war, 8% of adults said their family sometimes or often lacked enough food and 16% failed to pay all their bills the prior month, the Fed said, citing survey results. Although most households said they are financially stable, some “demographic groups — including low-income, young, and Black adults — saw meaningful declines” in their financial well-being from 2024 to 2025, the central bank said.

Click here to continue reading.

By Michael Wayland, CNBC

Click here to read the entire article.

Key Points

- The head of Capital One Auto, one of the nation’s largest auto finance lenders, told CNBC he isn’t overly concerned about rising consumer automotive debt and inflated used car prices leading to so-called “forever loans.”

- While median monthly car payments have jumped from $390 to $525 since 2019, data provided by Capital One Auto suggests vehicle costs have been stable compared with income.

- The lender found 80% of car purchasers who finance a vehicle are below the generally recognized payment to income threshold of 15%, even though they’re taking out longer loans to get to that goal.

The head of one of the nation’s largest auto finance lenders isn’t overly concerned about rising consumer automotive debt and inflated used car prices leading to longer loans on vehicle purchases.

His main reasoning? The percentage of income consumers are spending on their vehicles has remained relatively flat compared with 2019, before the coronavirus pandemic led to inflated pricing as demand surged but inventories stayed low.

“If I just told you, ‘Car prices going up, interest rates going up, insurance prices going up,’ you would say, ‘You know what, consumers must be paying more as a ratio to the income,’” Capital One

Auto President Sanjiv Yajnik told CNBC. “However, if you look at every quintile of salary and earnings of people, the payment-to-income ratio has remained fairly flat.”

While Capital One reports median monthly car ownership payments have jumped from $390 to $525 since 2019, data provided exclusively to CNBC from its automotive unit suggest that vehicle costs have stayed relatively stable compared with income. That’s because, overall, the payment-to-income ratio has remained flat at approximately 10% since 2019, according to the automotive arm of the American bank.

Capital One Auto found 80% of car purchasers who finance a vehicle are below the generally recognized payment to income threshold of 15%.

“The consumer is being cautious. They’re being responsible. This is a much healthier way to do things than the alternative, because it’s not a discretionary spend,” said Yajnik, referring to consumers prioritizing vehicle payments for transportation, including work.

To get to that goal, however, more consumers are taking on longer loans to keep payments affordable.

Click here to continue reading.

By Lori Sommerfield, Chris Willis, Taylor Gess & Lane Page; Consumer Financial Services Law Monitor, Troutman Pepper Locke

Click here to read the entire article.

On May 5, Craig Trainor, Assistant Secretary for the Office of Fair Housing and Equal Opportunity (FHEO) at the U.S. Department of Housing and Urban Development (HUD), used the American Bankers Association’s Risk and Compliance Conference to send a clear message about how the Trump administration plans to enforce the Fair Housing Act (FHA) going forward, including with respect to how it will treat special purpose credit programs (SPCPs).

Trainor stated that the FHEO is “returning to the beating heart” of FHA enforcement by prioritizing cases with “strong evidence of disparate treatment,” and that it “will no longer chase phantom discrimination based upon statistical disparities without evidence of intentional unlawful treatment.” In other words, HUD is signaling a focus on intentional discrimination claims, and a corresponding retreat from large‑scale disparate impact cases built primarily on statistical disparities.

At the same time, Trainor underscored that the FHEO is closely scrutinizing SPCPs. He specifically referenced a program offered by the Washington State Housing Finance Commission that was “created to address disparities resulting from past discrimination against racial groups.” As summarized below, earlier this year the FHEO launched an investigation into that program. Trainor warned that SPCPs “that do not comply with the statutory text of the [FHA] continue to be subject to enforcement,” and he cautioned that lenders “found engaging in illegal discrimination will be held accountable.”

Trainor also encouraged institutions that may have offered programs with race‑based eligibility criteria to take “immediate remedial actions” and indicated that “meaningful” remedial efforts will be viewed favorably in deciding whether and how to pursue enforcement.

Click here to continue reading.

By Walter Donway, The Daily Economy

Click here to read the entire article.

Organizations often mistake measurable activity for meaningful achievement. AI productivity metrics confuse computation costs with added value.

A recent Wall Street Journal report on a workplace trend called “tokenmaxxing” offers a revealing glimpse into some of the confusion attending America’s AI boom.

Some companies, the Journal reports, are experimenting with measuring an employee’s engagement with AI by tracking “tokens”—the units into which the system converts text typed into prompts. Now, in some workplaces, it seems token consumption has become a badge of an AI user’s engagement, experimentation, or productivity.

This is a striking moment. During what often feels like a national celebration—or national heart attack—over the transformative productive potential of artificial intelligence, we are publicly debating if an employee’s value might be measured by the volume of text sent to and from a chatbot.

The controversy deserves more attention than its odd jargon suggests. It exposes a central uncertainty in the AI revolution: what, exactly, does productive use of AI mean?

Reporting in Built-In, Ellen Glover reports that tokenmaxxing “is taking much of the tech industry by storm… individuals are ranked on leaderboards based on how much they use AI, with generous perks and incentives encouraging them to push these tools to their limits… The assumption is that the more you use AI, the more productive you must be. Those who lean in the hardest will come out on top.”

She adds that some employees take advantage of the fact that now “systems use AI agents to work autonomously for hours on end, reviewing and editing large codebases and writing entire programs while their human users are out living their lives.”

Tokens are real enough. Large language models do not “read” language as humans do. They convert words, punctuation, fragments of words, and other text elements into tokens—standardized units processed mathematically. The more tokens used, generally, the more computing resources consumed. AI providers often charge by token volume. Tokens therefore matter to engineers, accountants, and software managers.

When tokens migrate from a technical unit used in billing into a measure of employee performance, however, we risk confusing the cost of computation with the creation of value.

Click here to continue reading.

Glen speaks with Andrew Warren about the Financial Health Network’s new report which makes the case for modernizing the definition of underbanked consumers. Also- X Money makes its long-promised debut, and the OCC potentially rides to the rescue of interchange (and workable payment processes).

Links related to this episode:

- The Financial Health Network’s latest 26-page “brief”: Unbanked, Underbanked, or Something Else Entirely?

- The Financial Health Network’s EMERGE conference, May 19-21 in Atlanta: https://finhealthnetwork.org/event/emerge-financial-health-2026/ (USE CODE “JOINME-GLEN” FOR A DISCOUNTED RATE)

- Ron Shevlin’s take on the prospects for X Money- https://www.forbes.com/sites/ronshevlin/2026/04/17/musks-x-money-how-it-could-win-and-why-it-wont/

- Payments Dive on the OCC’s move to short-circuit Illinois’ Interchange Fee Prohibition Act: https://www.paymentsdive.com/news/occ-plans-to-preempt-illinois-interchange-law/817618/

- Our recent conversation with Ncontracts’ Stephanie Lyon about the shifting regulatory environment, including interchange battles: https://www.big-fintech.com/the-states-of-financial-regulation/

If CU Unplugged’s style of hands-on problem solving sounds like your cup of collaborative tea, check out our Innovation Club. This group of forward thinkers meets virtually each month, and our twice-annual in-person session is coming up in May. Reach out about a guest pass: https://www.big-fintech.com/innovation-club/

By PMNTS.com

Click here to read the entire article.

Subprime consumers are often viewed through a narrow credit-risk lens. PYMNTS Intelligence’s “Who Is the Subprime Consumer? A Behavioral Profile” shows a different picture: a large, steady and measurable part of the U.S. consumer economy that is changing how it uses credit, installment products and one-time cash events to manage daily financial pressure.

The report finds that 17% of U.S. consumers, or roughly 44 million adults, fall into the subprime credit range. That share has held within a narrow band across 47 monthly survey waves from March 2022 through January 2026. In other words, this is a durable segment with distinct behaviors, needs and product opportunities.

The data also shows that subprime consumers aren’t just heavy credit card revolvers. In fact, the share of subprime consumers who always or usually revolve their balances has fallen from about 50% in mid-2023 to 38% in January 2026. At the same time, 35% of subprime consumers have no credit or store cards at all, creating a gap for issuers, merchants and installment providers that can serve this group with products built around cash flow rather than traditional prime-card assumptions.

That shift is especially visible in BNPL and healthcare. Subprime consumers use BNPL at higher rates than the overall population, but they concentrate this usage among specific providers. Younger subprime consumers also report delaying care, skipping prescriptions and borrowing from family or friends to manage healthcare costs. Tax refunds and one-time government payments play a similar role: Subprime consumers often use these to cover bills, repay debt or stabilize household finances.

For banks, card issuers, merchants, BNPL providers and healthcare finance firms, the message is clear. Subprime consumers are not outside the credit economy. They are navigating it differently, and the companies that understand those behaviors may put themselves in a better position to build lasting relationships with this 44 million-consumer market.

In “Who Is the Subprime Consumer? A Behavioral Profile,” learn how:

- Subprime consumers are moving across credit products. Always-or-usually revolving has declined, while BNPL and installment products are taking on a larger role in how these consumers manage purchases.

- Healthcare costs are creating new financing needs. Young subprime consumers are delaying care, negotiating bills and using installment options at rates that point to unmet demand at the provider office, pharmacy and telehealth checkout.

- Cash flow timing can shape product strategy. These consumers often use refunds and one-time payments to cover bills or repay debt, giving issuers and lenders clearer moments to reach them with relevant offers.

Click here to continue reading.

By Celonis, published in Banking Dive

Click here to read the entire article.

The notion that the best way for banks to modernize their core systems is to rip them out and replace them with new ones is not only outdated—it’s also inefficient.

Consider a study by IBM that found 94% of banking overhauls exceed their deadlines, resulting in delays that negatively affect the project’s ROI.

Fortunately, the rise of AI means that there are other paths to transformation. In this new era, leading financial institutions are focusing less on decommissioning outdated software and more on how new technology can help them extract data and create value from existing systems. It’s a savvy move that enables organizations to leverage what they have, while still modernizing for the future.

“We’ve been so focused on moving from legacy systems to newer systems, when the real opportunity is in how we use the data and improve the process,” says Jaymini Hirani, Financial Services Lead at Celonis.

Data is everywhere, but where’s the intelligence?

Modern banks rely on hundreds of systems and applications. For example, a single payment may come in contact with 200 different systems as it traverses from initiation and authorization to clearing and settlement.

Some of those systems represent the latest technology. But others are likely legacy software, core banking systems, or even Excel spreadsheets managed by specific employees. As a result, the related data is siloed within systems and applications, making it difficult to access.

In this environment, interactions and handoffs between teams become increasingly complex, and the risk of errors increases, resulting in delays and manual workarounds. The fragmented nature of the data also limits transparency, which can impede productivity and, more importantly, lead to regulatory concerns.